Is the selling finally over? | Luminor

Is the selling finally over?

- Global equities remained volatile in November but managed to post a small gain for the month

- Emerging market equities came in unexpectedly strong in November, handsomely outperforming all other regions

- Global yields have come down lately and the US 10-year treasury yield is well below 3% again

- The market is currently pricing in two more rate hikes in the US over the year

- Supply-driven decline in commodity prices should not be seen as an indicator of an approaching recession

- Emerging market equities may be showing signs of ending the trend of underperformance

Although November ended with a gain, global equities were very volatile during the month

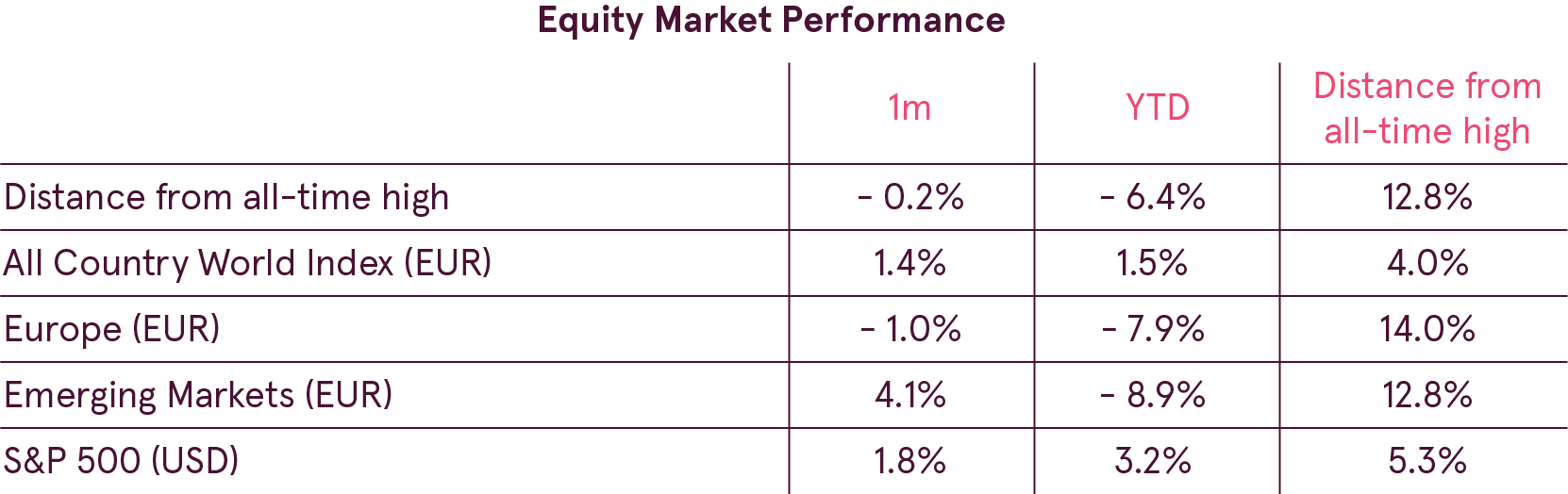

If we only look at the monthly return statistics for global equities, it may seem like the markets were fairly calm in November, especially compared to the previous month. Global equities, represented by the All Country World index (ACWI), have managed to show a gain of 1.4%. However, the fight between investors who were willing to buy the dip and those who used rallies as opportunities to sell resulted in wide intra-month price fluctuations. Consequently, the trading range for the month reached close to 5% for ACWI. Actually, with one month still left till the end of the year it is already possible to say that the current year was the most challenging for global investors since 2011.

Snapping the half-year-long trend of underperformance, emerging market equities excelled in November, surging over 4%. Nevertheless, emerging market equities are still lagging in all other major markets year-to-date with an almost 9% loss. European stocks closely follow with a close to 8% decline this year.

North America is basically the only major region where the stock market is still showing a year-to-date gain this year thanks to the strength of US equities. And with North America representing more than half of the All Country World index value, global equities are also up 1.5% this year.

Global interest rates have been retreating quite significantly lately

Fears of interest rates increasing have kept everything connected to the Fed in the spotlight. Comments by Fed President Powell about the level of the neutral interest rate were one of the main factors triggering the global equity sell-off last month, as they implied a significant increase in interest rates ahead. At the end of November, however, Powell stated that interest rates “remain just below the broad range of estimates of the level that would be neutral for the economy.”

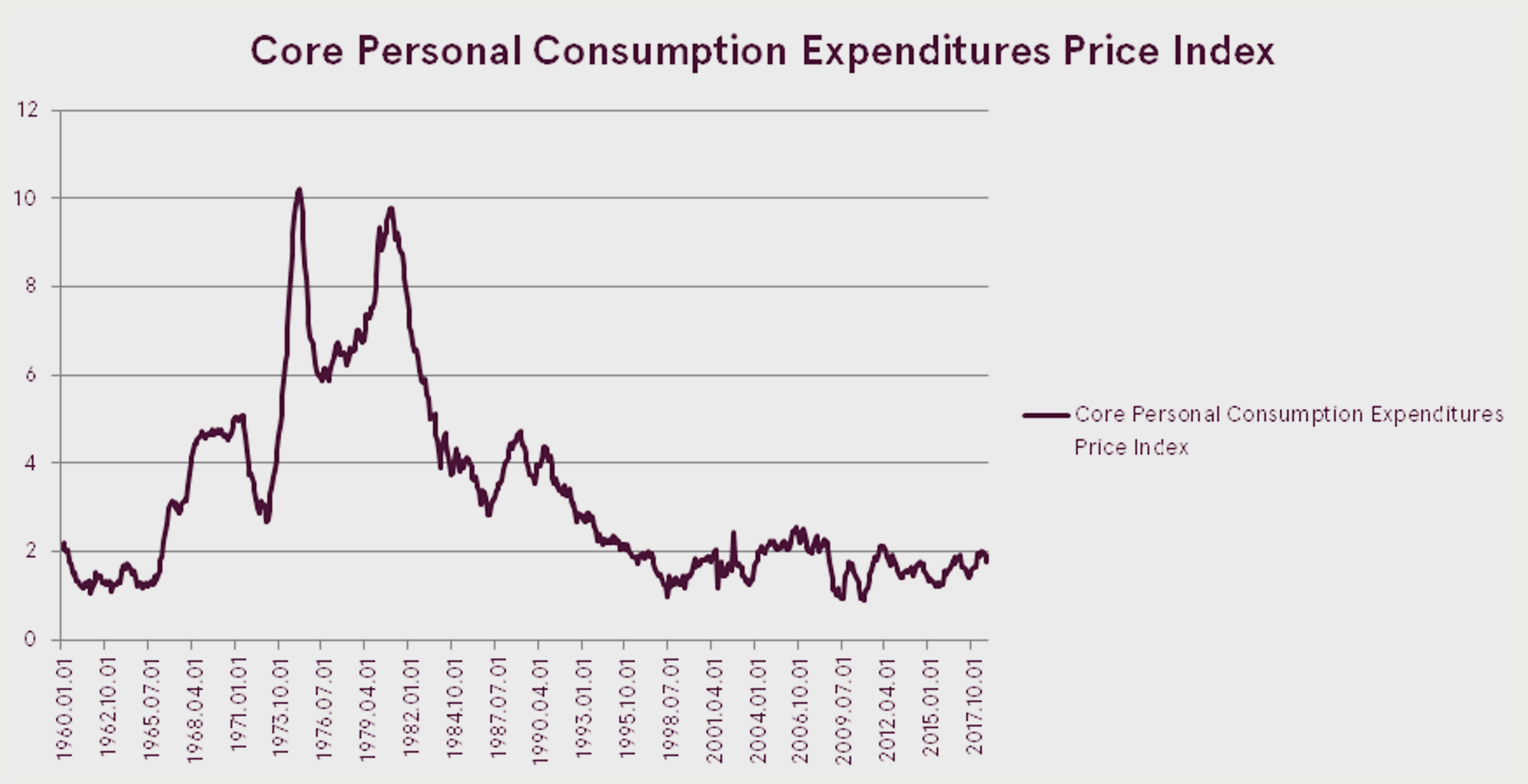

Such a message was taken by the market as a signal that the Fed is becoming more dovish, meaning fewer hikes ahead. Investors took the change in the Fed communication as a reaction to slightly softening economic indicators and easing inflation pressures. For example, US core PCE, which is the Fed’s favorite gauge of inflation, has been in decline for three months in a row with the last reading of 1.78%. At the same time, the statistics of new jobs created in November, although still indicative of a strong jobs market, came below consensus expectations.

Accordingly, bond yields came down considerably in response. The US 10-year Treasury yield plunged over 30 basis points from its high and is now again below 3%. The shorter term rates also declined, but by a smaller magnitude. As a result of the current reassessment, the market still expects the Fed to hike rates in December with a 75% probability (down from 80% one month ago).

A more significant adjustment of expectations happened over a longer timeframe. If a month ago the market assigned over 30% probability that the Fed would raise rates over 3% by the end of next year, now that probability is just about 5%. That implies that investors now price in two more rate hikes until next December.

What can be implied from the drop in oil prices?

In response to increasing supply, oil prices dropped by 1/3 since the start of October. An unexpectedly strong increase in US production and some concessions on Iranian sanctions resulted in oil supply exceeding demand and leading to a buildup of inventories.

Declining oil prices drove the whole commodity index lower. Decreasing commodity prices, however, should not be taken as a sign of an upcoming recession, as the lower prices are driven by higher supply, not lower demand. Moreover, as commodities are an input to production, lower prices should help ease inflation pressures. So, this should be good for financial markets going forward, as central banks will be able to keep interest rates lower for longer.

Furthermore, historically, global equities have usually followed declining commodity prices by a positive performance. Since the year 1988, the All Country World index has risen 8.3% on average in the year following a decline in the Bloomberg Commodity Index. That is 1.5% higher than the average increase in that period.

Are emerging market equities at the turning point?

Emerging market equities were surprisingly strong in November, although it is still premature to say if the trend of underperformance has finally ended. However, there are several factors that should provide support to emerging market equities.

Due to long period of underperformance, at the same time that earnings were growing, emerging market equities became quite cheap both in relative and absolute terms. The Current Cyclically Adjusted P/E (CAPE) for emerging market equities is just 12.5, compared to the historical average of 15.8. The valuation is also much lower than global stocks in general, which have a CAPE of 19.9 currently.

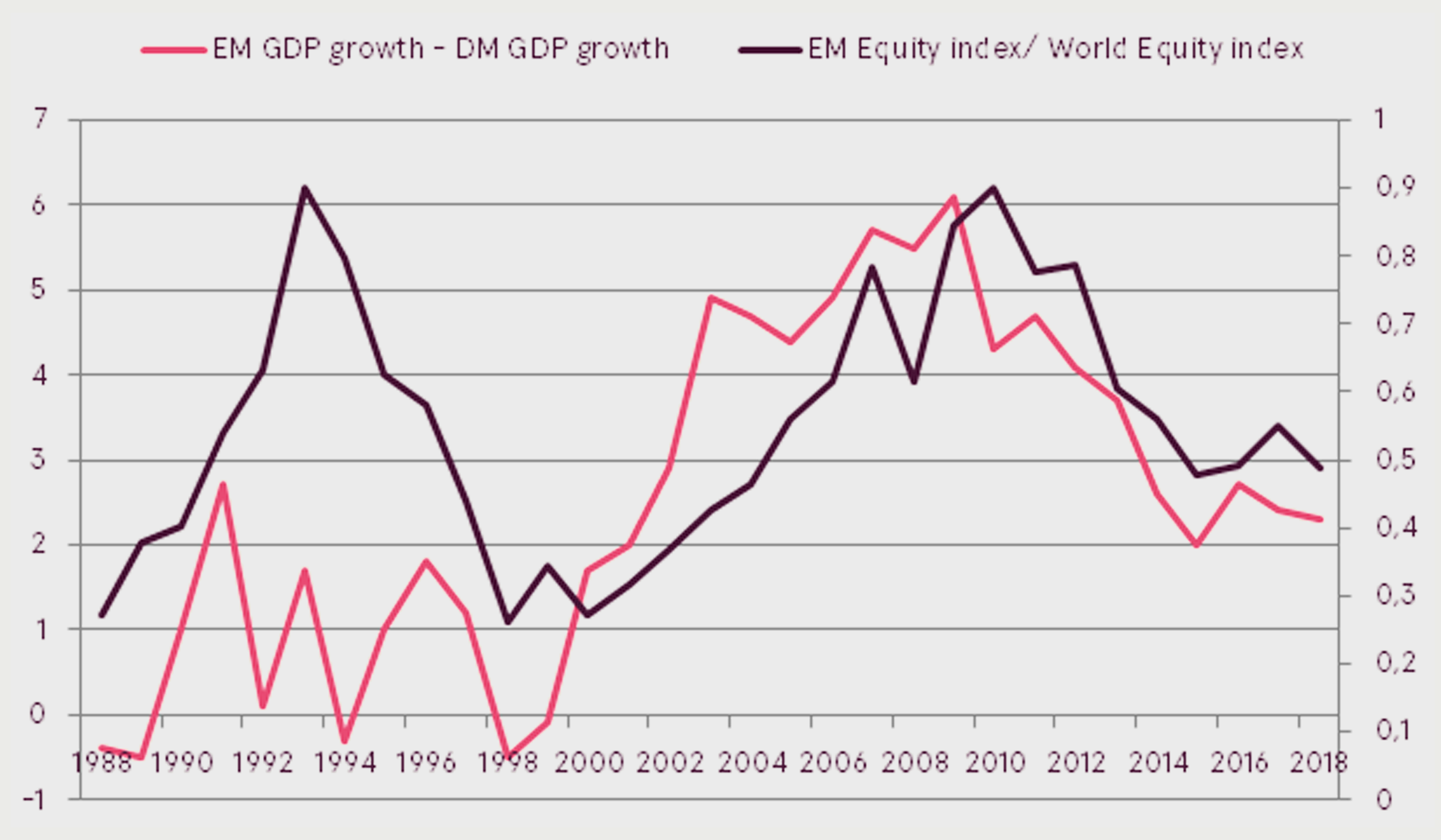

In addition, the economic conditions are beginning to favor emerging markets. The Citigroup Economic Surprise index, which measures how strong the actual economic indicators were compared to expectations, has been improving handsomely over the last quarter. At the same time, the same indicator deteriorated for developed economies. Consequently, as the economic growth in developed economies is slowing, emerging market economies are starting to improve. Such development should lead to the increasing economic growth outperformance of emerging countries.

Historically, the relative performance of emerging and developed market equities has quite significantly correlated with the economic growth differential. Therefore, improving economic growth in emerging market countries should help the region’s equity markets outperform developed market equities. An additional boost may be provided if the trade war issues are solved between the US and China. The 90-day truce, achieved after the G-20 meeting, was the first step in the right direction. And the very positive market reaction was a good indication of what could follow once the trade war ends.

Finally, about half of the emerging market equity underperformance during the last 6 months came from currency depreciation. Emerging market currencies have been pressured recently by the rising USD interest rates, which also made credit conditions tighter for emerging market economies, as a big chunk of their debt is in USD. However, a recent retreat in the US interest rates and inflation expectations may help emerging market currencies rebound, providing additional support to the regional equities.

Outlook

With the latest softening of global economic indicators, the question of whether we are heading for a global recession arose. Interestingly, the official definition of recession differs between the OECD and the one in use in the US made by National Bureau of Economic Research (NBER). The OECD defines recession as a slowdown of growth below the trend, while NBER requires GDP contraction. As a result, OECD has indicated that we’ve already experienced two recessions since 2009, in 2011 and 2015, while there were still none identified in the US.

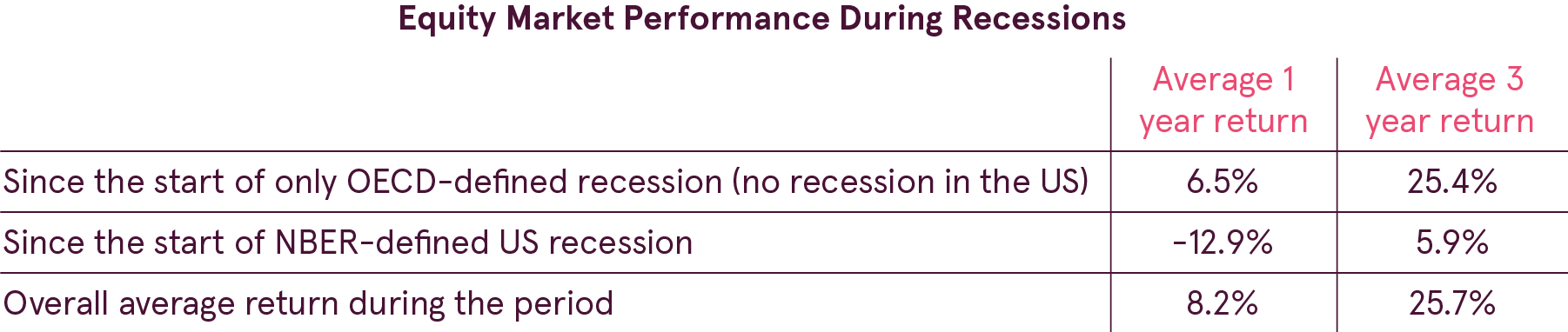

There has been a big difference in stock market performance historically when there was just an OECD-defined recession without one in the US compared to when there was also a NBER-defined recession in the US. In case of only an OECD-defined recession, when there was no recession in US, the World Equity Index has actually risen on average 6.5% in the year since the start of the recession. However, when there was also an NBER-defined recession in the US, world stocks dropped 12.9% over a year.

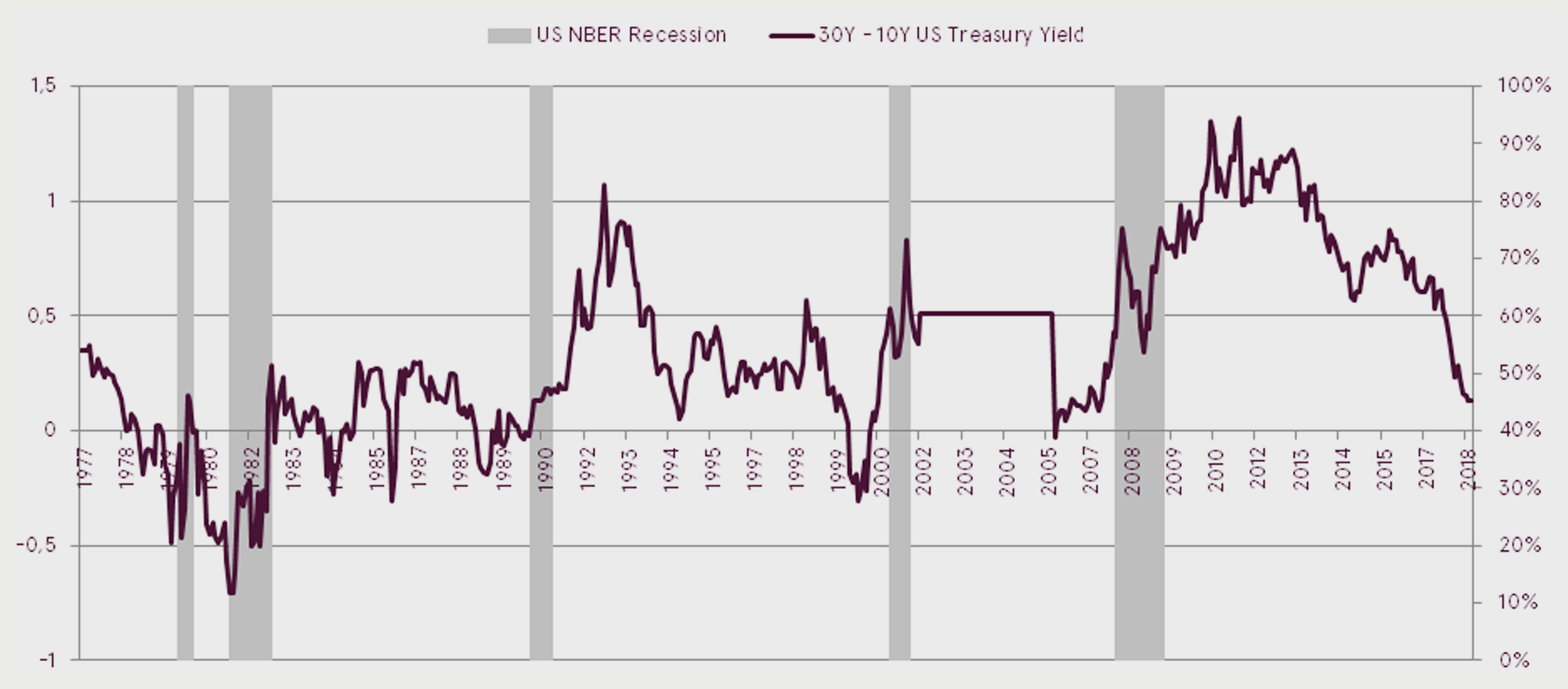

Looking at the current picture, we may indeed see a slowdown in global economic growth. However, there is still no sign of an upcoming US recession. The flattening US yield curve, which was seen as one of the signs of a potentially upcoming recession, has actually been steepening lately if we look at the longer end of the curve. The 30-year versus 10-year yield spread is currently standing at 0.29%, which is actually fairly close to its historical average of 0.35%.

Considering the above and that global equities are currently at the average historical valuation, the return from global equities in the longer term should also be close to the historical average. However, considering existing political and geopolitical risks, the path to that return may be quite volatile. As a result, investors should be prepared for a potentially rough ride ahead.

Subject to changes in circumstances, the opinions given in the Overview may differ from current ones, which is why Luminor bears no responsibility for the timeliness of the opinions presented in the Overview.

This Overview should not be deemed an investment consultation or an offer to invest in financial instruments, make financial transactions or act in any other way. The Overview may not be interpreted as Luminor’s confirmation or promise of occurrence of the events reported in the Overview. The data presented is not connected to any potential information receiver’s specific investment goal, financial situation nor any specific needs.

The historical yield of securities described in this Overview is for reference only. The historical yield may not be considered as a guarantee for future investment results, as the real yield may differ considerably from the one referred to herein.

Luminor shall not be held liable for any loss that the customer might incur due to relying on information contained herein. Before making any investment or credit decision it is recommended to use the help of a respected professional and evaluate the suitability of the investment product or service to the customer’s risk profile and goals.

The terms and conditions of financial instruments and investment fund prospectuses can be found on the Luminor homepage www.luminor.lv. This material may not be copied, distributed or published in any form without Luminor’s prior written consent.