Do higher rates mean the beginning of the end? | Luminor

Do higher rates mean the beginning of the end?

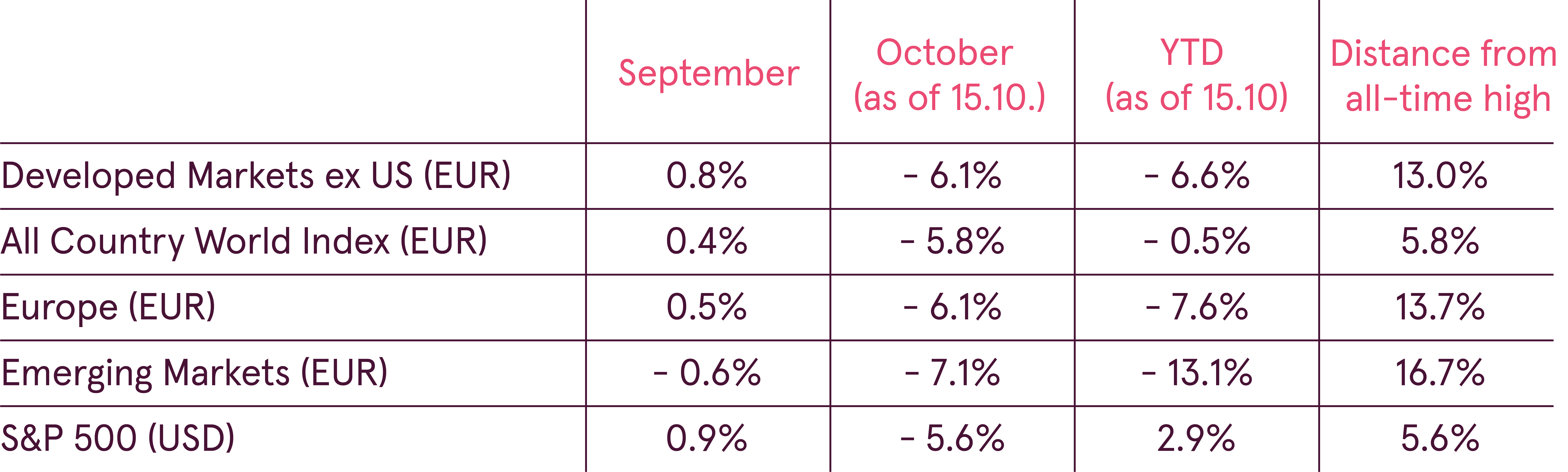

- After new all-time highs reached in September two weeks of the new month erased YTD gains for the global equities

- Fears of faster and more significant interest rate increases hamper investor sentiment

- US yields spiked in October as 10-year Treasury rate reached a seven-year high of 3.26%

- Global equities have an earnings yield of 5.4%, which is significantly higher than 10-year bond rates in US and Eurozone of 3.15% and 1.20% respectively

- Political and geopolitical development add additional uncertainty

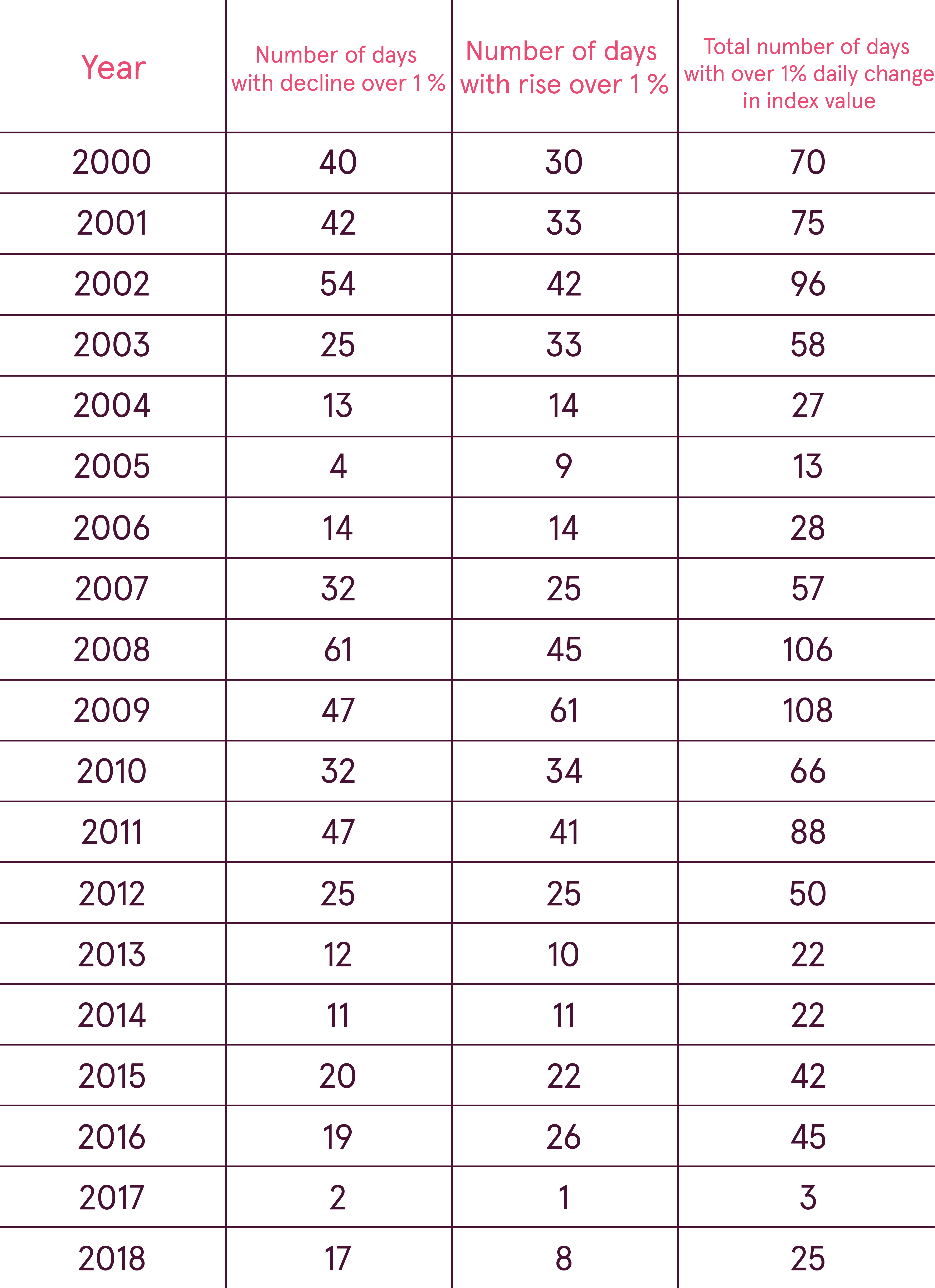

- Since the year 2000 All Country World Index had on average 52 days per year with over 1% daily changes in the value of the index

After new all-time highs reached in September two weeks of the new month erased YTD gains for the global equities.

Global financial markets continued on the positive note in the month of September with both the US S&P 500 and the All Country World equity index (ACWI) reaching new highs. However the second week of October brought the volatility back and erased over 5% of the global equity market capitalization. As of the 15th of October, the month-to-date drop for the ACWI stood at 5.8%. Still the index was basically flat for the year and less than 6% from its all-time record level.

The US equity market continued to outperform all the other major markets. Even after the 5.6% decline in October, the S&P 500 index was still showing an almost 3% gain for the year.

No changes were also in the lagging regions, as emerging market equities continued to underperform. Emerging market equities slipped over 7% in two weeks of October and are already over 16% below their all-time high.

With nine and a half years into the current bull market, and this one being the longest in the US history, each significant move to the downside gets many investors questioning if this is the start of the new downtrend. Bull markets, however, never end of just age and require some specific catalyst.

Fears of faster and more significant interest rate increases hamper investor sentiment

A rise in the US bond yields looks to be the main factor that started the sell-off. A gradual increase in the US yields started already in the first part of September in the anticipation of the third rate hike this year by the Fed. After the Central Bank raised rates and indicated its plans for a fourth hike in December, 10-year Treasury yields rose above 3% for the first time since May.

However, in the beginning of October US yields spiked even further with 10-year Treasury rate reaching a seven-year high of 3.26%. The yields rose despite lower inflation reading for September and slightly softer than expected US job market data. The cause for the rise was a comment made by the Fed president Powell that “we're a long way from neutral, probably”. This was interpreted by the market that the Fed still sees the current rates as very accommodative and expects significant rate increase in the future.

A spike in the interest rates is the main risk to the forward outlook

Interest rate level is a major factor determining the equity market outlook and is especially closely watched by investors now after a long period of 0 rates. Investors fear that the Fed may go too far and too fast with the rate hikes and thus hurt economic growth. Higher interest rates make it harder to get credit and reduce consumption, which hurts corporate revenues. At the same time higher borrowing costs decrease profit margins thus further impairing corporate earnings.

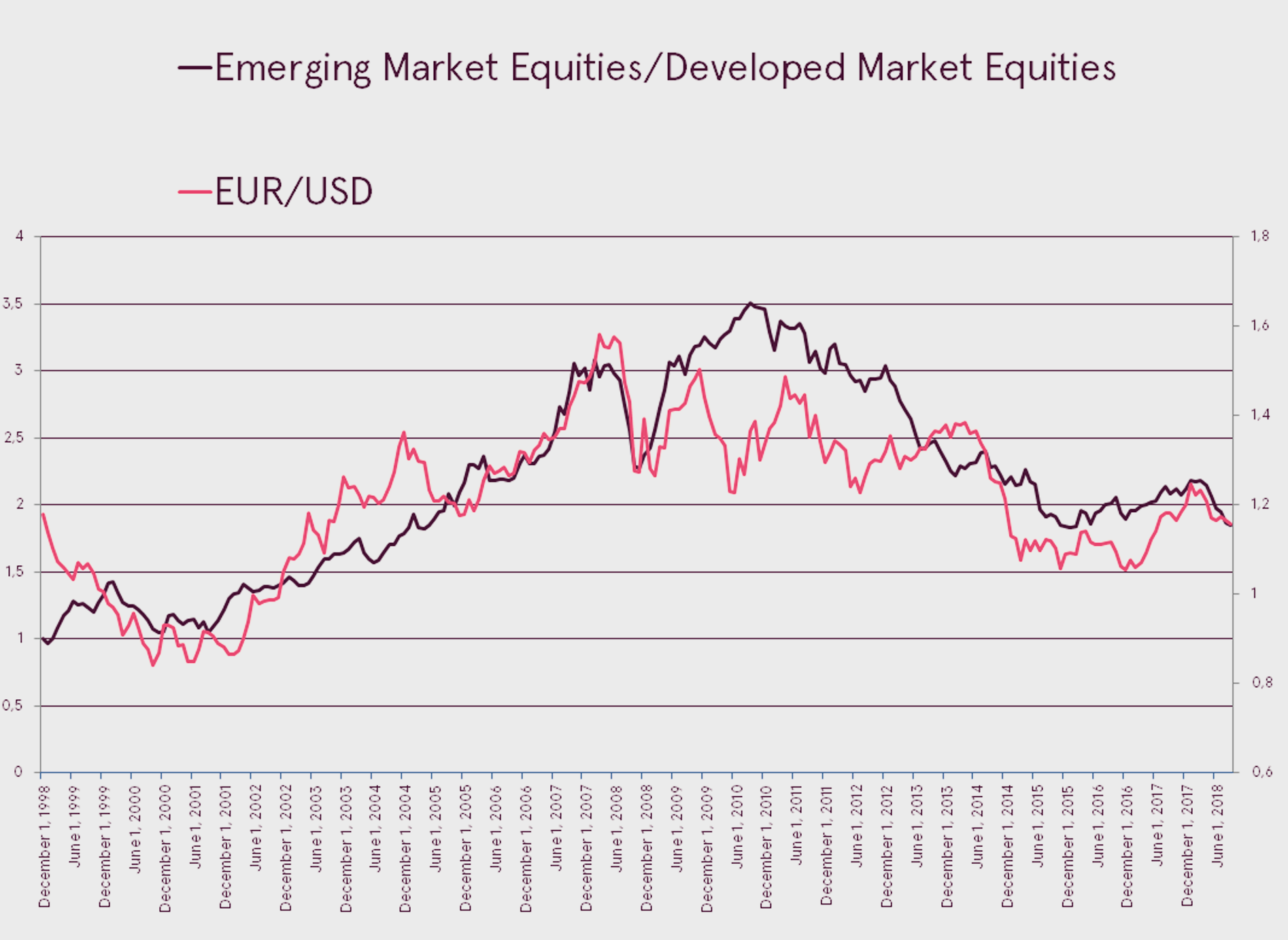

Higher US rates are especially bad for emerging market economies, as a big chunk of their debt is denominated in USD. Therefore a rise in US rates and resulting stronger dollar significantly tighten monetary conditions for those economies. Consequently, it gets harder for the emerging markets to get new funding while servicing of existing debt gets more expensive. Decrease in commodity prices, which is usually associated with stronger dollar comes as an additional burden. As a result, history has shown that emerging market equities have always underperformed the developed market stocks during the dollar uptrend.

Finally, a significant rise in bond yields raises their relative attractiveness compared to equities.

However, we are very far from that levels, as the global equities have an earnings yield of 5.4%, which is significantly higher than 10-year bond rates in US and Eurozone of 3.15% and 1.20% respectively. Consequently, equities still offer a healthy risk premium to investors.

Moreover, we believe that the Fed will not hike the rates too far and too fast, as they are still closely following current economic indicators. And with the latest slight deterioration in the leading economic indicators global growth is expected to moderate a bit in the near future. Therefore the Fed will not have the need to hurry with the rate hikes. As a result, although still a risk, the probability of rates overshooting and hurting the global economy is still fairly low.

Political and geopolitical development add additional uncertainty

Developments in the political and geopolitical area continue to keep many investors nervous. The main issue is a trade war between US and China, which is still far from being solved. As Trump tries hard to deliver on his promises to reduce the influence of China in the global economy and tackle the outflow of jobs from the US he continues to pressure China. If the tensions escalate significantly they may hurt the global economic growth.

Additionally, the budget crisis in Italy adds more political risks to the Eurozone, while the latest tensions between the US and Saudi Arabia increase geopolitical risks. As those political developments are practically impossible to predict, they create uncertainty, which hurts investor sentiment.

Current volatility levels are just returning to historical averages

Due to extremely benign period of steady growth in the year 2017 investors got used to low volatility environment with small price fluctuations. As a result, current environment seems like extremely volatile. In reality however, the volatility is just returning to historical average level.

If we look at the daily moves of the All Country World index, then since the year 2000 the index had on average 52 days per year with over 1% daily changes in the value of the index. In 2017 however, there were only 3 such days. Therefore the current year’s 25 such days seem like a lot.

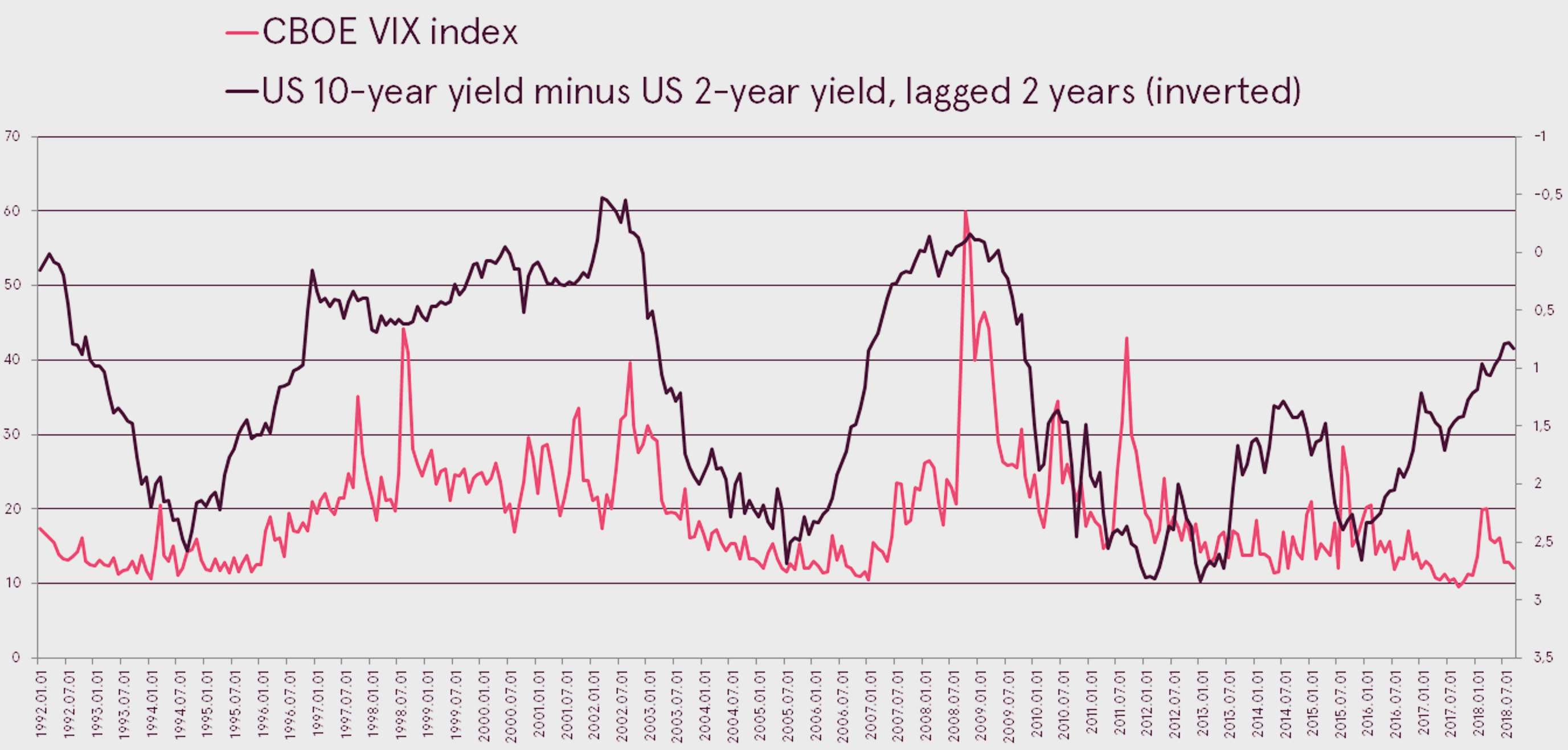

Investors shouldn’t be afraid of the higher volatility, as it is perfectly normal for the current stage of the bull market. Moreover, historically also the yield curve flattening that occurred recently has signaled the rise of the equity market volatility in the future, so investors should take this into account.

Notably, volatility offers great opportunities for the disciplined investors making regular contributions, providing possibilities to enter at attractive prices.

Outlook

Despite some slight moderation in the global economic growth, the overall environment is still supporting the continuation of the uptrend in equities. Moreover, starting earnings reporting season should be a good catalyst for improved investor sentiment, which got hurt by higher interest rates.

Still, investors should be aware of the expected higher volatility due to outstanding risks outlined above.

Subject to changes in circumstances, the opinions given in the Overview may differ from current ones, which is why Luminor bears no responsibility for the timeliness of the opinions presented in the Overview.

This Overview should not be deemed an investment consultation or an offer to invest in financial instruments, make financial transactions or act in any other way. The Overview may not be interpreted as Luminor’s confirmation or promise of occurrence of the events reported in the Overview. The data presented is not connected to any potential information receiver’s specific investment goal, financial situation nor any specific needs.

The historical yield of securities described in this Overview is for reference only. The historical yield may not be considered as a guarantee for future investment results, as the real yield may differ considerably from the one referred to herein.

Luminor shall not be held liable for any loss that the customer might incur due to relying on information contained herein. Before making any investment or credit decision it is recommended to use the help of a respected professional and evaluate the suitability of the investment product or service to the customer’s risk profile and goals.

The terms and conditions of financial instruments and investment fund prospectuses can be found on the Luminor homepage www.luminor.lv. This material may not be copied, distributed or published in any form without Luminor’s prior written consent.