Interest rate cut expectations pushed markets to new highs | Luminor

Interest rate cut expectations pushed markets to new highs

Anton Skvortsov

Investment and Risk Analysis Team Leader

- Global equity markets recouped May’s losses and reached all-time highs

- The first half of this year marked the best start to the year for global financial markets since 2015

- Global economic activity continues to slow as manufacturing sector shows signs of contraction

- Investors are expecting fairly aggressive monetary policy easing from both Fed and ECB

- Q2 earnings reporting season should provide hints of future earnings growth

Best first half of the year since 2015

Despite the ongoing global economic slowdown, June turned out to be a positive month for financial markets, as world equities managed to recover most of May’s losses. US equities were once again leading the climb, rising by almost 7% for the month and reaching an all-time high. Equity price gains continued in July, pushing the All Country World Index to record levels.

Equity Market Performance

| 1m | YTD 2019 | Distance from all-time high | |

|---|---|---|---|

| Developed Markets ex US (EUR) | 3,5% | 12,2% | 7,9% |

| All Country World Index (EUR) | 4,1% | 15,3% | 1,9% |

| Europe (EUR) | 4,3% | 13,6% | 7,8% |

| Emerging Markets (EUR) | 3,4% | 9,6% | 8,0% |

| S&P 500 (USD) | 6,9% | 17,3% | 0,1% |

*based on monthly data

Source: MSCI, finance.yahoo.com

Emerging market equity price gains were more modest, and as a result, year-to-date returns are lagging behind developed market equities. Developed market equities have outperformed emerging market equities almost twofold since the beginning of the year—developed equities are up by 16.1% year-to-date compared with a 9.6% gain for emerging market equities.

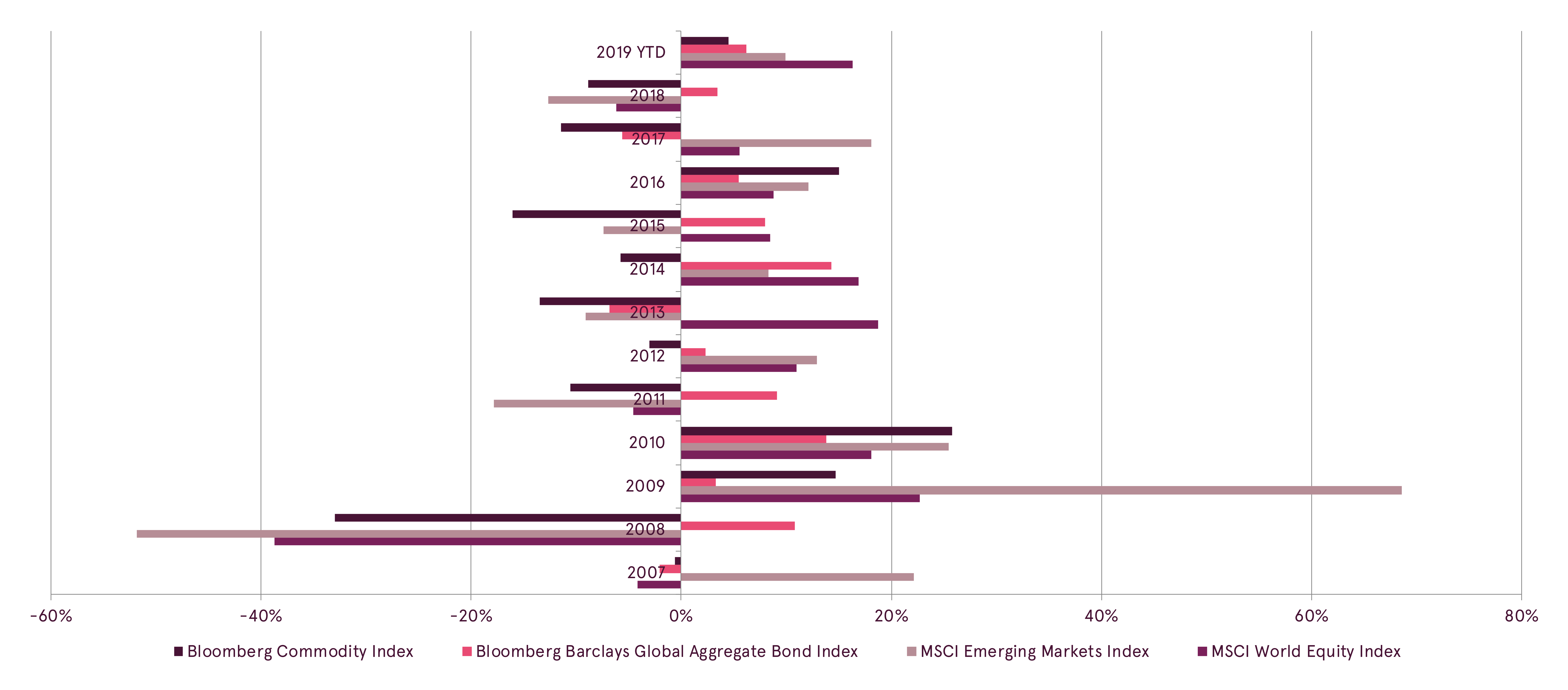

In a complete turn of fate compared with last year, when no major asset class produced any decent returns, the first half of this year marked the best start to the year since 2015. This year the prices of bonds, stocks and commodities are all rising, with the smallest gain being 4.5% (commodities).

Calendar Year Returns of Various Asset Classes

Source: Bloomberg

Slower global economic growth is driving down inflation expectations

With no improvement in the current economic indicators, investors continued to pin high hopes on the central banks to provide monetary stimulus to support global financial markets. As a result, the usually considered bad news, with worse than expected economic indicators, was actually considered good and pushed global equities higher, as investors believed such news improved the chances of rate cuts.

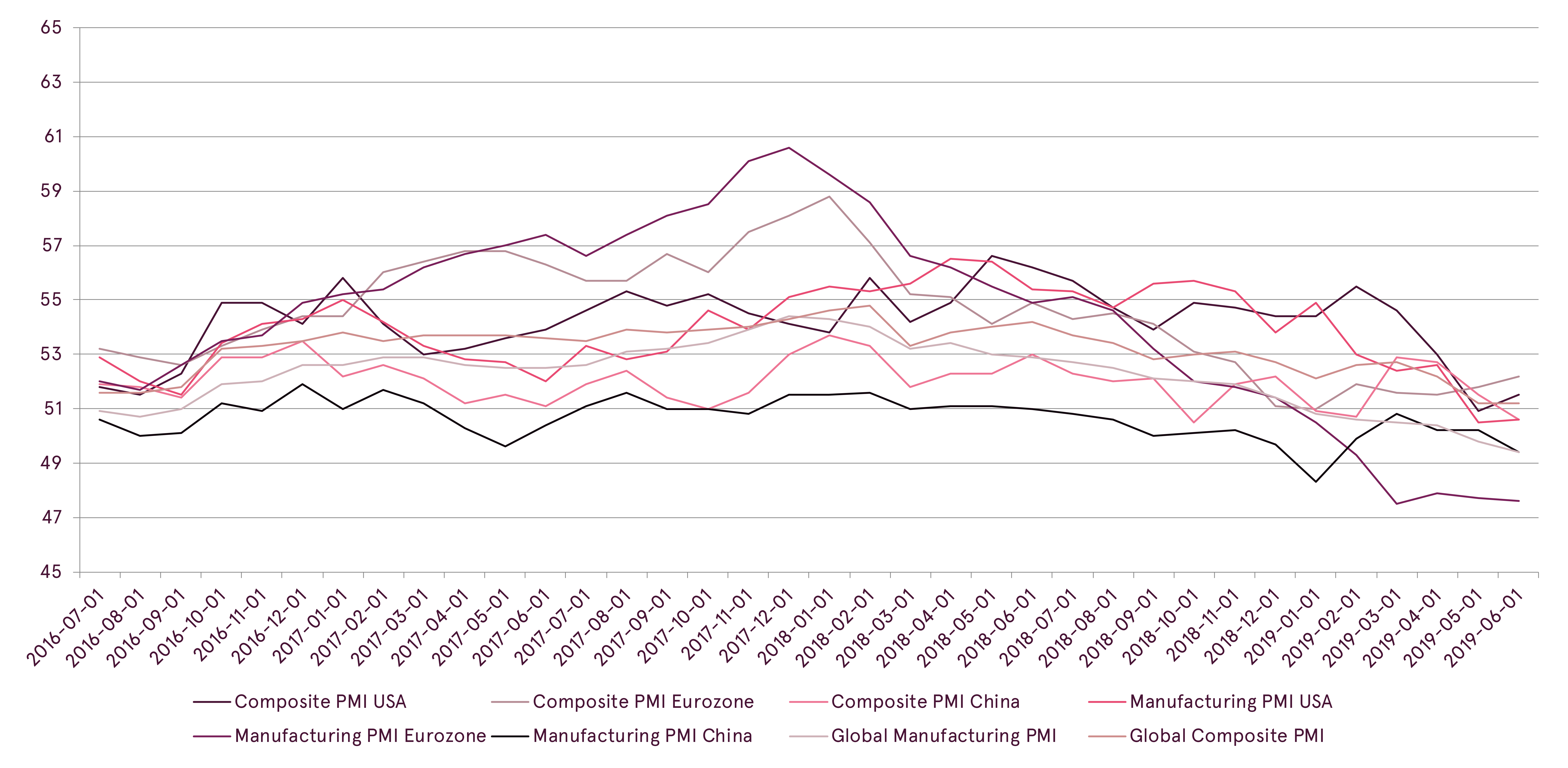

Global economic activity indeed continues to cool down, with most indicators pointing towards slower growth ahead. Recent Purchasing Managers’ Index (PMI) data shows that the world manufacturing sector is contracting, with only the US still sporting modest gains. Consequently, only the strong services sector is keeping the overall economic growth alive.

Purchasing Manager Indices (PMI) for Selected Countries

Source: Bloomberg

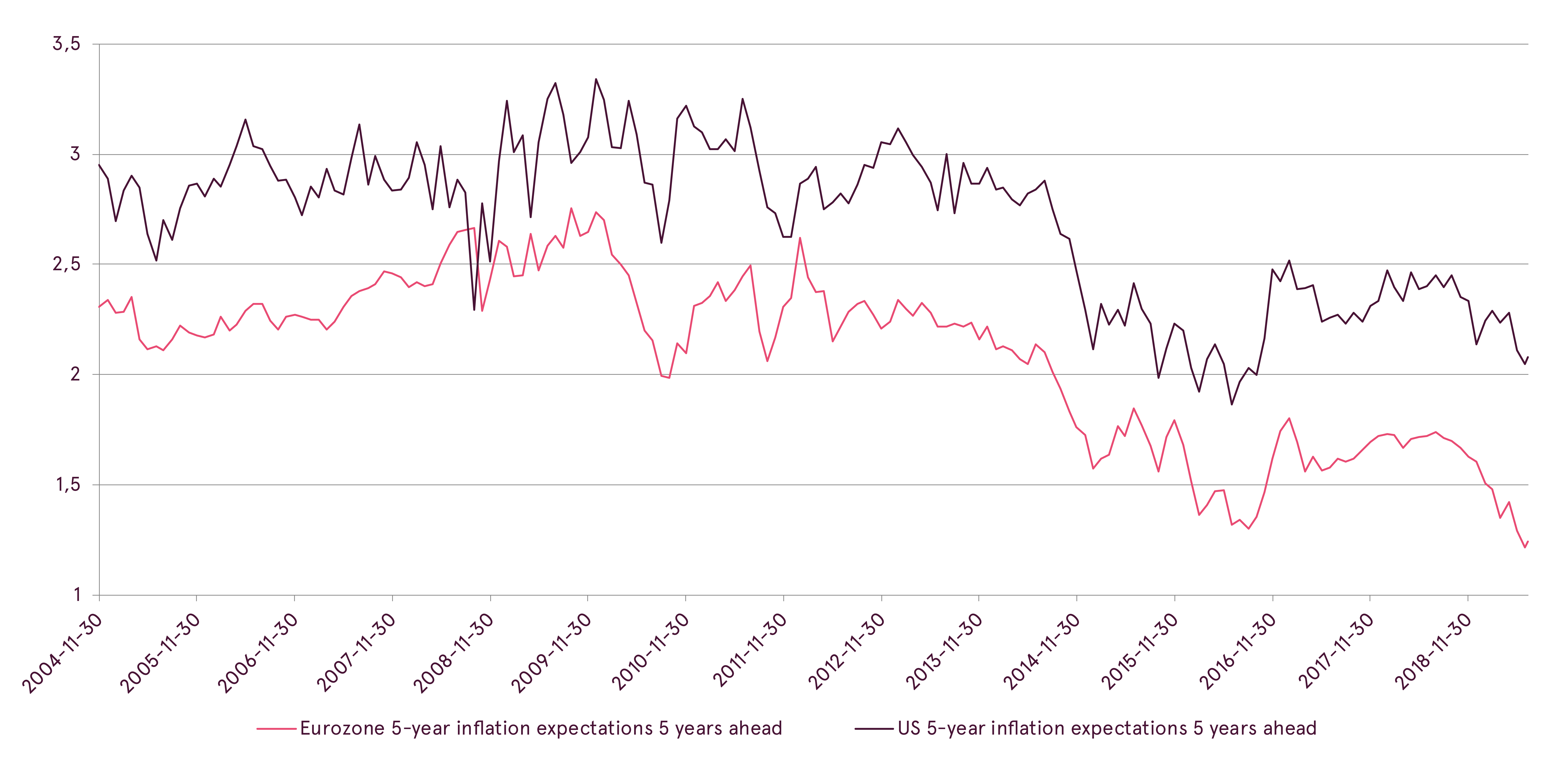

Slowing economic growth is keeping inflation pressures subdued. As a result, both current inflation readings and long-term expectations have been steadily decreasing and are staying well below the central bank target rates. Long-term inflation expectations in the US dropped to the lowest level since 2016, whilst in the Eurozone such inflation expectations plunged to lows not seen in 15 years. As one of the main central bank mandates is to keep inflation stable, such a drop in expectations led investors to believe that central banks will step in with monetary stimulus. In fact, the ECB and the Fed presidents both confirmed readiness to move forward with monetary easing.

Long Term Inflation Expectations

Source: Bloomberg

Markets are pricing in quite aggressive additional stimulus from the Fed and the ECB

Fed president Powell in his recent speeches acknowledged the risks to the economy due to the slump in the global manufacturing sector and increased trade tensions. Therefore, Powell indicated readiness to cut rates in July as a precautionary measure to support the economy. Consequently, investors consider the US’ July rate cut a done deal, with the only question being the magnitude of the rate cut—investors assign a close to 20% probability of a 50 basis point rate cut.

Overall, investors were fairly aggressive in their expectations of the pace of monetary policy easing. Currently, markets are pricing in around 0.8 percentage points of rate cuts during the next year. Consequently, the US 10-year treasury yield dropped back to 2%, as investors have piled in to fixed income assets.

Despite being at a negative interest rate already currently, the ECB also confirmed readiness to move forward with additional stimulus. ECB president Draghi pointed out that the central bank still has tools left to further ease monetary policy. As a result, investors are expecting a 20 basis point rate cut and a restart of the bond buying programme to be announced at the ECB meeting in September.

Such expectations pushed German 10-year bond yields to an all-time low of -0.4%. Moreover, the market is now expecting Eurozone rates to remain in negative territory until 2025.

Additionally, it was announced that Christine Lagarde, current Managing Director of the IMF, was chosen as the next ECB president starting from November 2019. The choice satisfied investors, as Lagarde is considered a supporter of Draghi’s monetary policy actions and appears to be open to unconventional monetary policy. Therefore, investors’ expectations of the ECB’s future policy actions remained unchanged.

Monetary policy easing should keep US dollar under pressure

Changes in the relative levels of interest rates play an important role in determining exchange rate movements. As the interest rate differential moves in favour of one country, its currency tends to appreciate as a result. Historically, the EUR/USD exchange rate has broadly followed the changes in the euro and dollar interest rate differential according to data compiled since 2005.

EUR/USD exchange rate vs Eurozone - US interest rate differential

Source: Bloomberg

Taking into account the fact that euro interest rates are now below 0, the ECB has much less room for further cuts compared to the Fed. Therefore, euro rates should become relatively more attractive supporting the EUR going forwards. This trend could help push the EUR/USD exchange rate higher by the end of the year.

Q2 earnings reporting season will be important in shaping investors’ expectations of future growth

July marks the start of the earnings reporting season for Q2 2019. Global earnings growth expectations keep being lowered, but a significant rebound in the growth rate is expected by the end of the year. As a result, guidance about the future expected performance would be closely studied during the current earnings reporting season.

According to the I/B/E/S Refinitiv data, Q2 2019 corporate profits in the US are expected to stay at the same level as one year ago. In Europe, analysts are expecting a modest earnings growth of 0.8% compared with Q2 2018.

Looking one year ahead, however, the earnings growth rate is expected to pick up significantly. Eurozone corporate profits are expected to grow by 7.4% during next year, whilst profit growth in the US during the same period is expected to reach 7.5%. Moreover, investors are pinning the highest of hopes on the growth of emerging market corporate earnings, expecting them to increase by 9.7% during the next year.

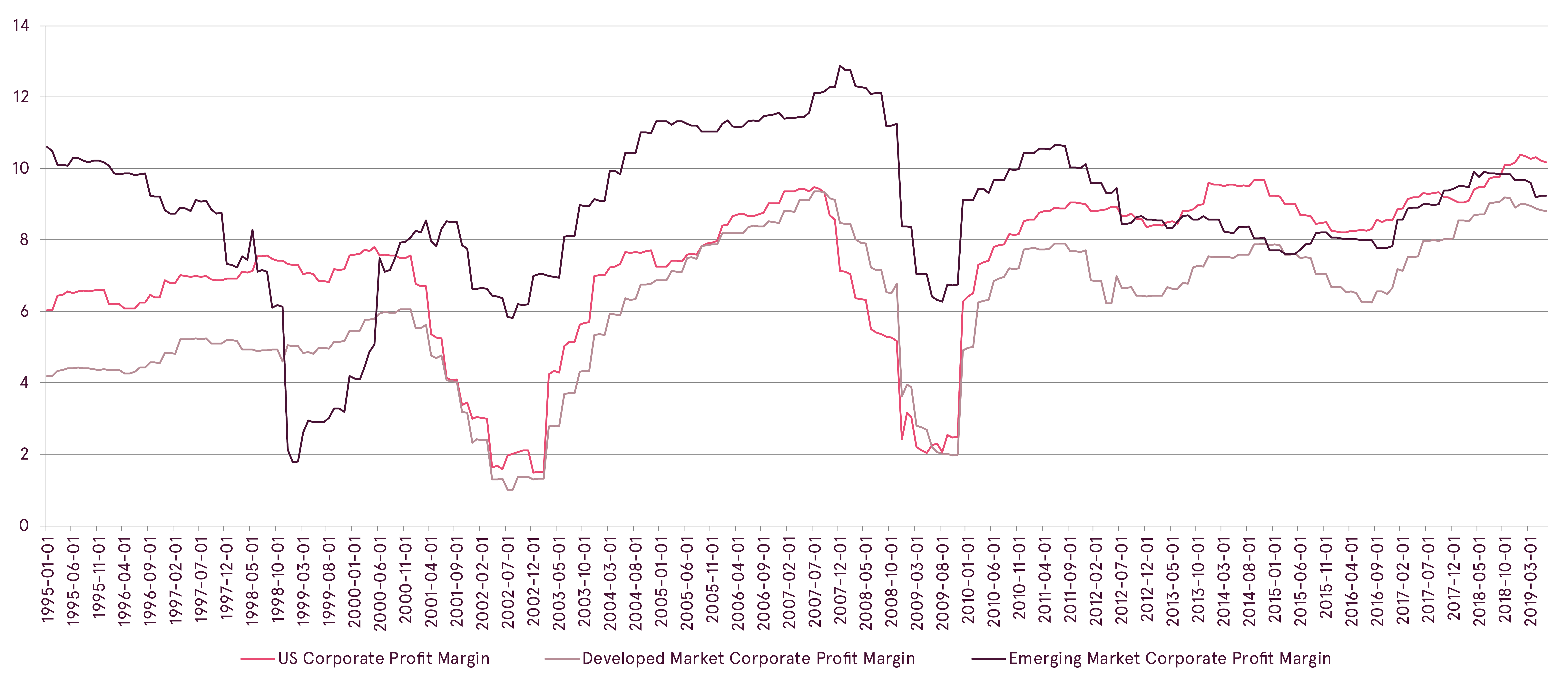

Corporate Profit Margins

Source: Bloomberg

Such strong growth expectations increase the risk of potential disappointment by the actual data. Profit margins of development market companies in general and in the US in particular are close to record levels, meaning that the profit growth should mostly happen through increased revenues. Therefore, such strong growth expectations are dependent on the rebound of global economic growth occurring by the end of this year. Only the emerging market corporate profit margins are still around 30% below the record levels reached in 2007 and thus have room for improvement.

Outlook

After the recent gains in equity markets, global stock valuations are surpassing long-term historical average levels. Although the overall world equity market valuation is far from extreme, some regions, such as the US, are getting on the expensive side. At the same time, emerging market equities are still relatively cheap. Nevertheless, such valuation levels require continued strong earnings growth to support the uptrend in equity prices.

As a result, the economic growth rebound in the second half of this year is extremely important for global equities, and the trade war truce achieved during the G20 meeting between the US and China provided much needed hope to investors. Although nothing specific was agreed during the meeting, the restart of negotiations led investors to believe that a trade deal will be reached by the end of this year, providing much needed support to the global economy.

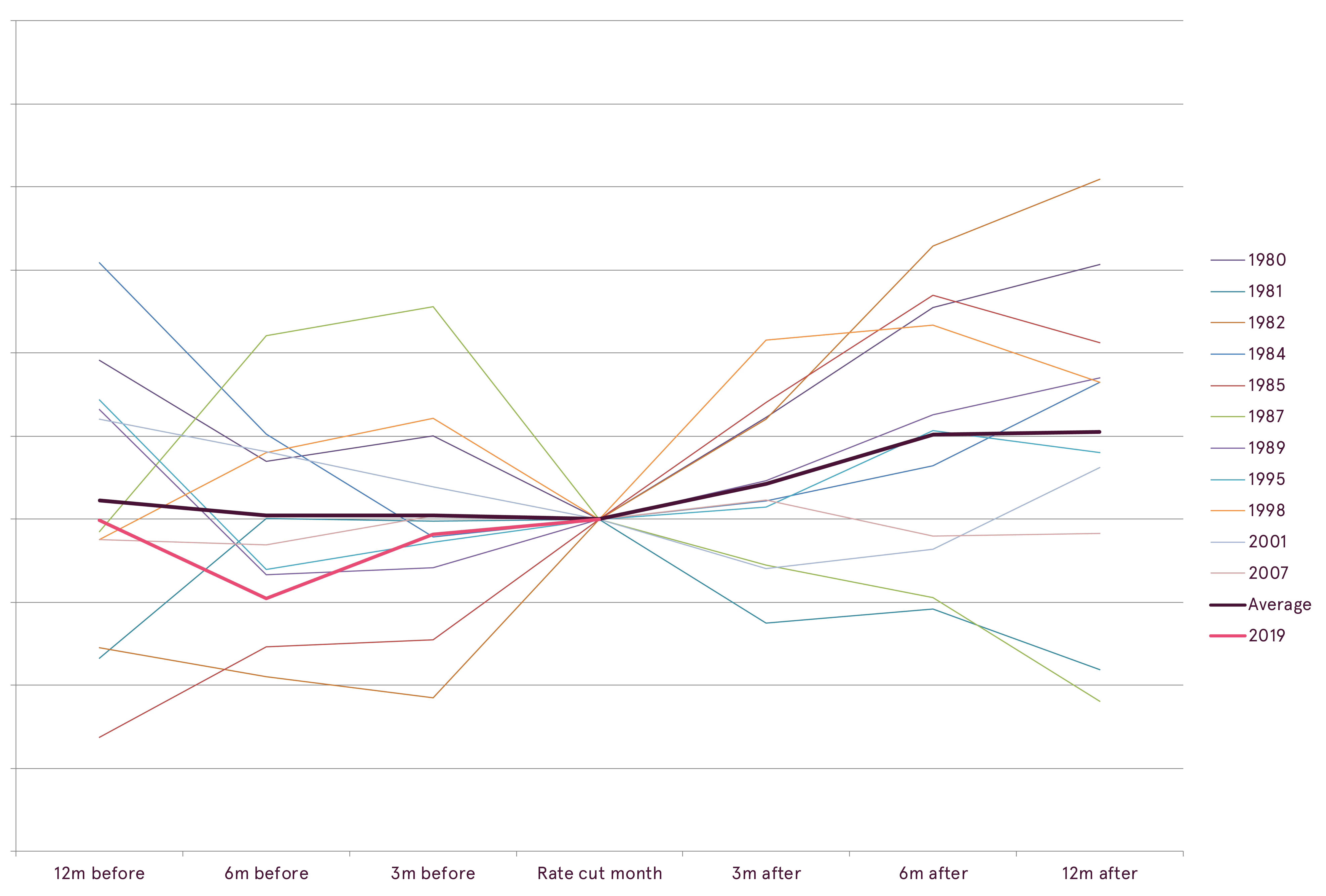

Additionally, lower interest rates should also support global equities. A decrease in interest rates helps improve the profit margin by keeping financing costs low. Moreover, equity valuation tends to rise when the Fed lowers interest rates. Historically, the P/E ratio of US stocks has increased by 10% on average a year after the first rate cut by the Fed (data since 1980). However, the average starting valuation at the time of the first rate cut was significantly lower than it is currently. Therefore, there is a substantial risk that history may not repeat this time.

Change in Price / Earnings (P/E) Ratio of S&P 500 around first Fed rate cut

Source: Bloomberg, Luminor calculations

Additionally in the fixed income space, the valuations are currently fairly stretched due to aggressive interest rate cut expectations. As a result, should inflation pressures increase amidst an improving economic outlook, the central banks could fail to deliver the expected pace of rate cuts. This could lead to the repricing of expectations in fixed income markets, pushing rates higher and bond prices lower.

Overall, the risks continue to be elevated in the short-term, which should result in higher asset price volatility. Once the short-term risks resolve, however, the uptrend in global equity prices has a good chance of continuing further.

Warnings

- This Marketing Communication is not considered investment research and has not been prepared in accordance with standards applicable to independent investment research.

- This Marketing Communication does not limit or prohibit the bank or any of its employees from dealing prior to its dissemination.

Origin of the Marketing Communication

This Marketing Communication originates from the Portfolio Management unit (hereinafter referred to as PMU) – a division of Luminor Bank AS (reg. No 11315936, with registered address at Liivalaia 45, 10145, Tallinn, Republic of Estonia, represented within the Republic of Latvia by Luminor Bank AS Latvian branch, reg. No 40203154352, address: Skanstes iela 12, LV-1013, Riga, hereinafter - Luminor). PMU is involved in the provision of discretionary portfolio management services to Luminor clients.

Supervisory authority

As a credit institution Luminor is subject to supervision by the Latvian Financial Supervisory Authority (Finanšu un kapitāla tirgus komisija). Additionally, Luminor is subject to supervision by the European Central Bank (ECB), which undertakes such supervision within the Single Supervisory Mechanism (SSM), which consists of the ECB and the national responsible authorities (Council Regulation (EU) No 1024/2013 - SSM Regulation). Unless set out herein explicitly otherwise, references to legal norms refer to norms enacted by the Republic of Latvia.

Content and source of the publication

This Marketing Communication has been prepared by PMU for information purposes. Luminor will not consider recipients of this Communication as its clients and accepts no liability for use by them of the contents, which may not be suitable for their personal use.

Opinions of PMU may deviate from recommendations or opinions presented by the Luminor Markets unit. The reason may typically be the result of differing investment horizons, using specific methodologies, taking into consideration personal circumstances, applying a specific risk assessment, portfolio considerations or other factors. Opinions, price targets and calculations are based on one or more methods of valuation, for instance cash flow analysis, use of multiples, behavioural technical analyses of underlying market movements in combination with considerations of the market situation, interest rate forecasts, currency forecasts and investment horizon.

Luminor uses public sources that it believes to be reliable. However, Luminor has not performed independent verification. Luminor makes no guarantee, representation or warranty as to their accuracy or completeness. All investments entail a risk and may result in both profits and losses.

This Marketing Communication constitutes neither a solicitation of an offer nor a prospectus in the sense of applicable laws. An investment decision in respect of a financial instrument, a financial product or an investment (all hereinafter “product”) must be made on the basis of an approved, published prospectus or the complete documentation for such a product in question, and not on the basis of this document. Neither this document nor any of its components shall form the basis for any kind of contract or commitment whatsoever. This document is not a substitute for the necessary advice on the purchase or sale of a financial instrument, a financial product.

No Advice

This Marketing Communication has been prepared by Luminor PMU as general information and shall not be construed as the sole basis for an investment decision. It is not intended as a personal recommendation of particular financial instruments or strategies. Luminor accepts no liability for the use of the Marketing Communication content by its recipients.

If this Marketing Communication contains recommendations, those recommendations shall not be considered as an objective or independent explanation of the matters discussed herein. This document does not constitute personal investment advice or take into account the individual financial circumstances or objectives of the persons who receive it. The securities or other financial instruments discussed herein may not be suitable for all investors. The investor bears all risk of loss in connection with an investment. Luminor recommends that investors independently evaluate each issuer, security or instrument discussed herein and consult any independent advisors if they believe it necessary.

The information contained in this document also does not constitute advice on the tax consequences of making any particular investment decision. The estimates of costs and charges related to specific investment products are not provided therein. Each investor shall make his/her own appraisal of the tax and other financial advantages and disadvantages of his/her investment.

Risk information

The risk of investing in certain financial instruments including those mentioned in this document, is generally high, as their market value is exposed to many different factors. The value of and income from any investment may fluctuate from day to day as a result of changes in relevant economic markets (including changes in market liquidity). The information herein is not intended to predict actual results, which may differ substantially from those reflected. Past performance is not necessarily indicative of future results. When investing in individual financial instruments the investor may lose all or part of their investments.

Important disclosures of risks regarding investment products and investment services are available here.

Conflicts of interest

To avoid occurrence of potential conflicts of interest as well as to manage personal account dealing and / or insider trading, the employees of Luminor are subject to internal rules on sound ethical conduct, management of inside information, handling of unpublished research material and personal account dealing. The internal rules have been prepared in accordance with applicable legislation and relevant industry standards. Luminor’s Remuneration Policy establishes no link between revenues from capital markets activity and remuneration of individual employees.

The availability of this Marketing Communication is not associated with the amount of executed transactions or volume thereof.

This material has been prepared following the Luminor Conflict of Interest Policy, which may be viewed here.

Distribution

This Marketing Communication may not be transmitted to, or distributed within, the United States of America or Canada or their respective territories or possessions, nor may it be distributed to any U.S. person or any person resident in Canada. The document may not be duplicated, reproduced and(or) distributed without Luminor’s prior written consent.