Financial markets update: February 2018

- Currency poses continued headwind for euro-based investors, as euro gained over 4.5% in January against the USD

- First month of the year made global equity investors happy with a 5.5% gain (All country world index)

- Historically, after a more than 4% gain in January, MSCI World index finished the year positively in all cases since 1969

- Positive fiscal and political developments in Brazil translated into close to 10% gain for Latin American equities

- Long streak of low volatility ended in the beginning of February with a long-awaited correction

- Q4 earnings reporting season started on a positive note in US and Emerging markets, while European earnings are lagging

- Equities are no longer cheap, but double-digit expected earnings growth implies potential upside for equities even without change in valuation

The year 2018 started on a positive note with a continuation of the major trends in financial markets that were in force last year – global equities reached new highs, bonds were under pressure from rising yields, while the euro surged higher against the dollar. The first trading days of February however, brought the long-awaited correction to global stocks. Although after a long period of calm such fluctuations may seem extraordinary, that is just a usual correction after extensive price appreciation and the long-term outlook remains positive.

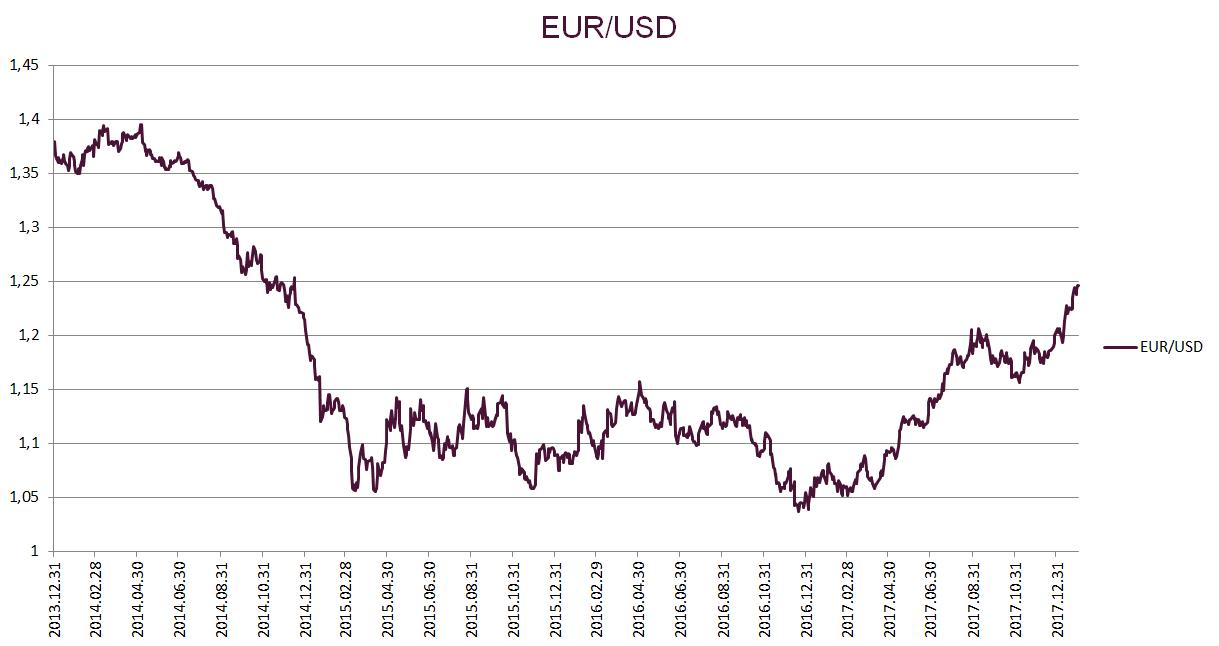

Euro-based investors continue to face headwinds from currency appreciation

After pausing somewhat in the fourth quarter of 2017, the euro appreciation trend returned with renewed strength in 2018. The euro managed to gain over 4.5% against the dollar due to continued strength in the Eurozone’s fundamental indicators. It is evident that the Eurozone may be enjoying the best growth in the decade, which is poised to continue as regional economic confidence remains close to 17-year highs. Such economic momentum ignites speculations of faster than expected policy tightening by the ECB, which helps propel the euro higher. Adding fuel to the fire, Austrian central bank head Nowotny suggested that conditions are in place for the ECB to end its bond buying program.

Nevertheless, general market expectation is still for the bond buying program to end in September 2018 and the first rate hike to occur by the middle of next year. Considering that inflation is stubbornly stuck significantly below the 2% target, such expectations seem reasonable. Therefore, although the long-term appreciation trend is still in force, in the short term the euro move looks stretched and EUR/USD pair may be due for a correction.

Positive January means positive year?

Global equities are off to a great start of the year with strong gains all over the world. The All Country World index gained 5.5% year-to-date in USD (1.6% in EUR). Many investors consider that a good sign for the rest of the year, saying that a positive January usually indicates gains for the full year. But is there any credibility to that theory?

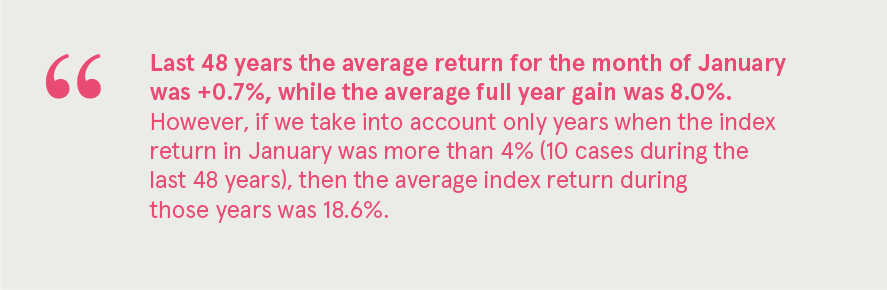

Looking at the MSCI World index, during the last 48 years the average return for the month of January was +0.7%, while the average full year gain was 8.0%. However, if we take into account only years when the index return in January was more than 4% (10 cases during the last 48 years), then the average index return during those years was 18.6%. Moreover, in all the 10 cases the index finished with a positive full year return. So historical data does confirm that a good January return tends to indicate a positive year. However, investors should be cautious relying on such data, as history may not repeat because there is no fundamental process guaranteeing that relation.

Latin American equities gain almost 10% as conditions in the region improve

Looking broadly, there was no major change in the equity market leadership, as emerging markets continued their outperformance – 3.8% vs 1.3% gains year-to-date (EUR based). Within emerging markets, however, Latin American equities came to the forefront with an almost 10% gain measured in EUR. The region benefited from improved investor sentiment towards Brazilian equities, as economic recovery continued widening, supported by lower interest rates and improving consumer and business confidence. Progress in the move to a better fiscal stability through pension system reforms provided further support. However, politics remains an important risk factor, considering that Brazilian president elections are scheduled for October 2018.

Robust earnings growth should become the backbone for future equity returns

January saw the start of the Q4 2017 corporate earnings reporting season that will continue in February and will be one of the main market-moving factors with focus being on forward earning guidance.

In the US, with slightly less than half of the companies having reported, the picture is very bright. 80% of companies reported better than expected earnings and 82% posted better revenue. At the current pace the earnings growth for 2017 in the US is expected to reach 12.7%. Supported by a boost from tax reform, US corporate earnings are expected to grow 17.5% in 2018.

European corporate earnings continue to be hampered by the euro strength. Of those companies that have so far reported earnings, only 44% beat expectations. The situation with revenues is more promising, as over 71% of companies reported better sales. Due to the low base effect however, the full year 2017 earnings growth is expected to reach a robust 14.9%, and for the year 2018 the European earnings growth is projected to reach 12.5% in 2018.

Growing sales and revenues together with fairly stable margins due to subdued wage pressure and low inflation should also translate into strong earnings for emerging market companies. Currently analysts are estimating earnings growth in the range of 10-15% for the region.

Equities are not cheap but earnings growth supports further upside

From the valuation perspective, looking at the trailing P/E (price divided by earnings for last year) global equities are starting to move into slightly overvalued territory compared to the longer term average. The valuation is the most stretched in the US with a P/E of 26.8, while developed markets in general also start to look expensive at 21.5 P/E. Emerging market equities are still quite fairly valued with a P/E of 16.2.

Such valuation shouldn’t scare investors, however, as it is far from extreme and there is still room for expansion. Moreover, thanks to double-digit expected earnings growth equities can grow over 10% without a change in valuation. However, a higher valuation may cause more volatility, so investors should be prepared for wider price fluctuations.

Main factors suggest continued positive development in global financial markets

Market volatility has already been very subdued for an extended time, which has been worrying some investors, as the fear of a short-term correction grows. Up until the last week of January the MSCI World index hasn’t experienced a larger than 1.5% drawdown for almost half a year (since August, 2017). However, a slew of positive economic data ignited investors’ speculations of faster than expected monetary tightening driving yields higher and causing the start of a correction in stocks. Big positions betting on lower volatility amassed during last year amplified the downside move as they got unwound.

Nevertheless, considering the very supportive environment and positive outlook for the economy and corporate profits, the correction shouldn’t be too long or deep. A longer-term uptrend is still in force and investors who were waiting to enter the market at cheaper levels may be using the price decline as a buying opportunity.

Sources: MSCI, Bloomberg, Thompson Reuters, IMF.

The present marketing material (Overview) was prepared by Luminor Bank AS (Luminor) analysts based on publicly available information at the time of preparation and relying on their professional evaluation.

Subject to changes in circumstances, the opinions given in the Overview may differ from current ones, which is why Luminor bears no responsibility for the timeliness of the opinions presented in the Overview.

This Overview should not be deemed an investment consultation or an offer to invest in financial instruments, make financial transactions or act in any other way. The Overview may not be interpreted as Luminor’s confirmation or promise of occurrence of the events reported in the Overview. The data presented is not connected to any potential information receiver’s specific investment goal, financial situation nor any specific needs.

The historical yield of securities described in this Overview is for reference only. The historical yield may not be considered as a guarantee for future investment results, as the real yield may differ considerably from the one referred to herein.

Luminor shall not be held liable for any loss that the customer might incur due to relying on information contained herein. Before making any investment or credit decision it is recommended to use the help of a respected professional and evaluate the suitability of the investment product or service to the customer’s risk profile and goals.

The terms and conditions of financial instruments and investment fund prospectuses can be found on the Luminor homepage www.luminor.lv. This material may not be copied, distributed or published in any form without Luminor’s prior written consent.