Consolidation in June – pause before another all‑time high or start of major reversal | Luminor

Consolidation in June – pause before another all‑time high or start of major reversal

Atis Krūmiņš

Head of Investment Management

- Second COVID‑19 wave potentially starting in USA and FED taking a pause with creating new liquidity put a hold on the rally in financial assets that has started in late March;

- As future economic outcomes remain highly unpredictable, volatility is likely to remain high with significant upward and downward price moves to be expected in second half of 2020;

- Starting Q2 earnings season should help understand the exact damage made from lockdown on revenues and earnings as well as to what extent those indicators improved after the reopening.

By any standards 2020 is very challenging year for making investments. Only six months have passed, but we have already seen one of the fastest and most significant market crashes in history followed by one of the most rapid recoveries in asset prices ever. Changes that usually take at least few years to realize, in 2020 happened over the course of few months. And with market environment becoming increasingly volatile, even difference of few days is capable to make what appears to be a good investment a bad one and vice versa.

What complicates things even more in 2020 is that investors have to operate somewhat in the dark. As we discussed previously, there are plenty of unknown risk factors that may play out in one or the other direction, and these factors raise many questions, which cannot be really answered right now. Nobody can tell how future situation with coronavirus will play out around the globe and in separate countries. Will there be new lockdowns leading to even more economic destruction or the worst is really over? How soon companies will be able to fully recover from COVID‑19 crisis and would bankrupted entities be replaced by new entrants? Moreover, will there be a deflation induced by oversupply and decreased aggregate demand problems, or central banks will manage to create as much liquidity as needed to actually trigger inflation around the world? This is the question of utmost importance as completely different combination of financial assets should be held depending on which scenario would play out.

Lately we see that even economists and analysts, people that are paid to make forecasts, provide estimates that miss actual numbers by a wide margin. In fact, it is hard to blame them, as relationships that used to work under normal business conditions, in post‑coronavirus world became broken and increasingly hard to model.

For now, markets, boosted by excess liquidity and massive inflow of general public that is willing to invest, provide most positive guesses as answers to all the unpleasant questions. We in its turn do not want to play a guessing game, but want to operate with facts or at least with high probabilities that certain scenarios are likely to happen. And from what we continue to observe, facts suggest that reality may turn out to be much bleaker than what markets continue to predict1.

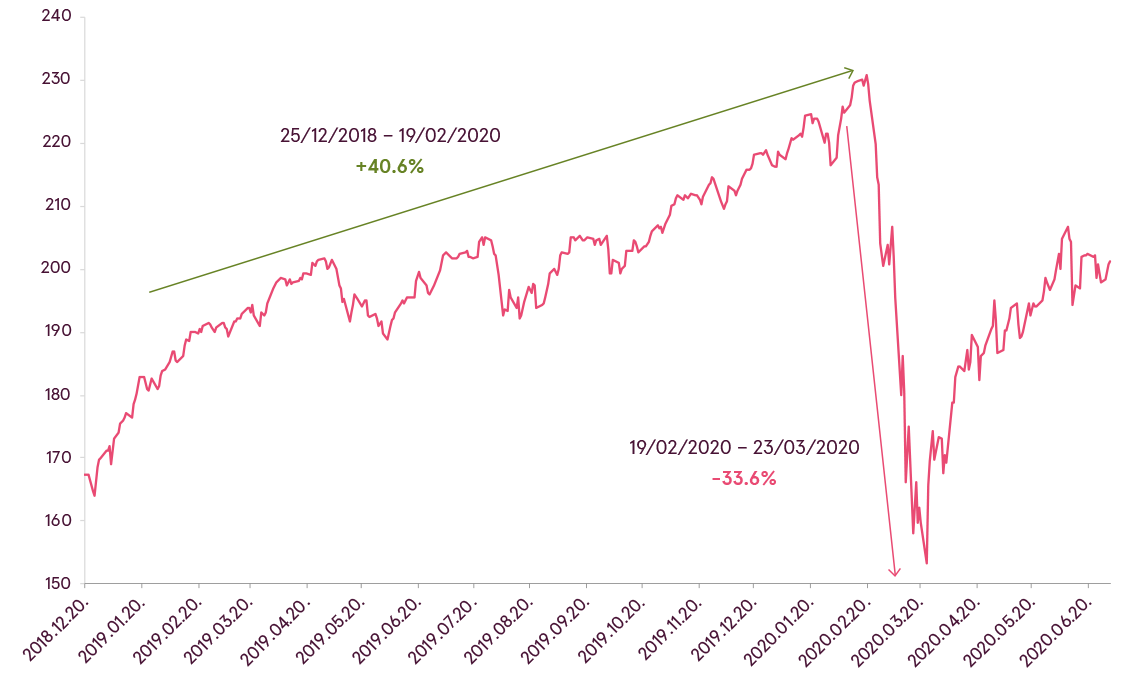

Key point here is that the harder it becomes to predict the future, more volatile, emotional and chaotic price movements in the markets become. Overall, since early 2018 when global economic slowdown has first started, speed and magnitude of price movements have been only increasing, while tops and bottoms are becoming more and more extreme. Such “roller coaster” makes financial system less stable and more fragile, and thus probability of even more severe moves either up or down than what was observed recently remains high in the upcoming months. In such environment waiting out for more clarity to appear may be the most optimal solution, even though in the end some opportunities may be missed and less potential profit earned. Remember, 2019 was an excellent year, with separate equity markets rising by more than 40%, and market trending higher almost every day. But then in March 2020 in about a month not only all those gains were wiped out, but losses generated as well.

Global equity index (MSCI ACWI in EUR)

Source: Bloomberg

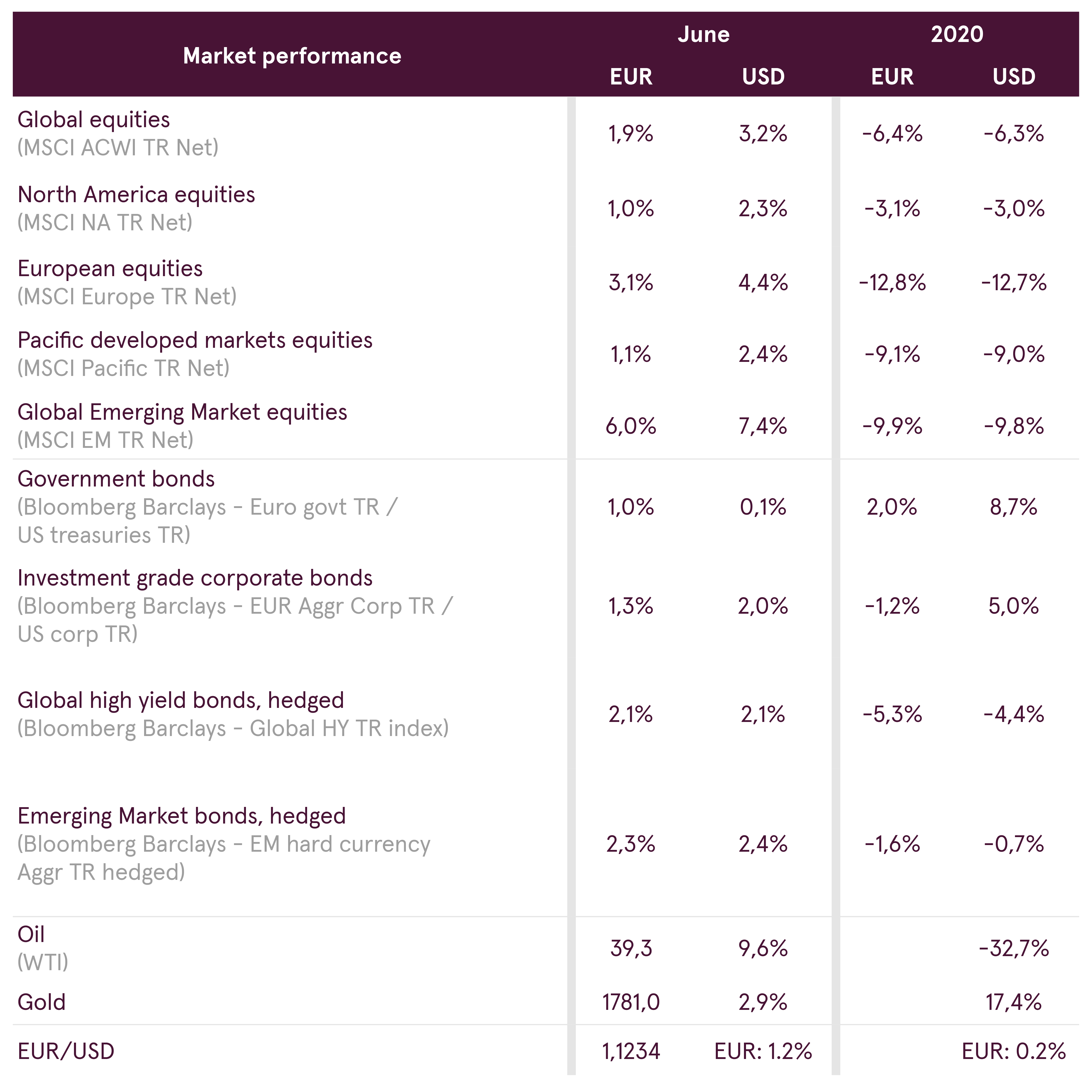

With that in mind, let us return to developments which happened in June. Rally that was observed in majority of financial assets since late March has slowed down in early June, with equity indexes consolidating since then in a gradual drift lower.

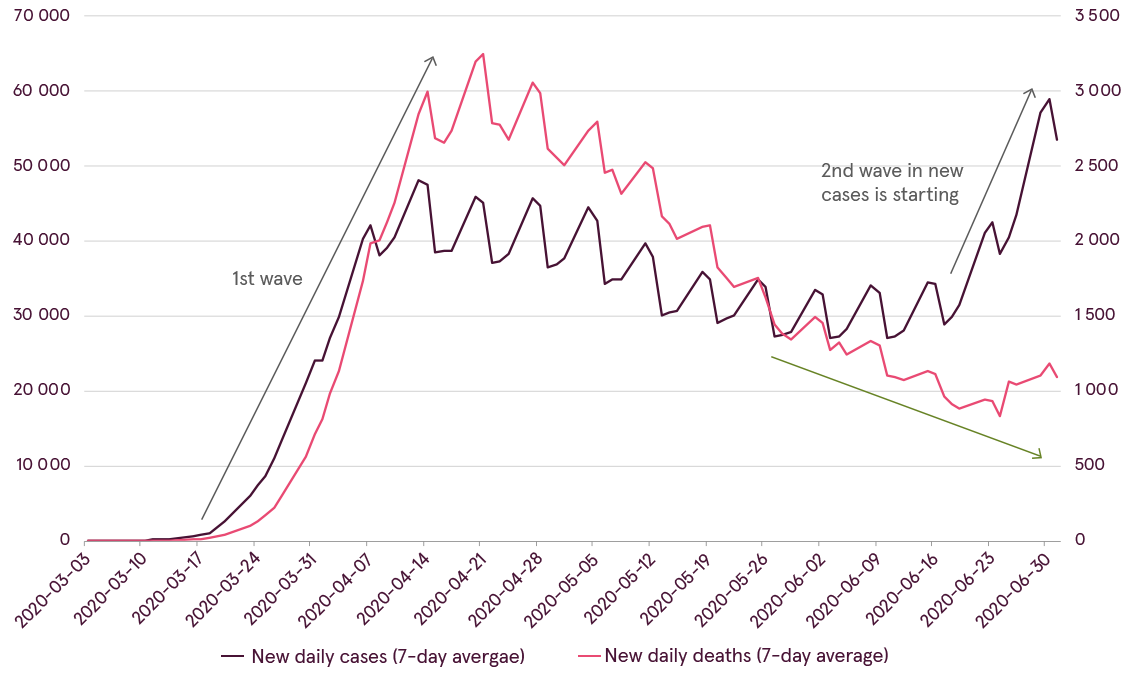

Two key catalysts why equity markets at least temporarily stopped their ascent are related to spike in new COVID ‑19 cases being registered in USA and FED making pause in creating new liquidity.

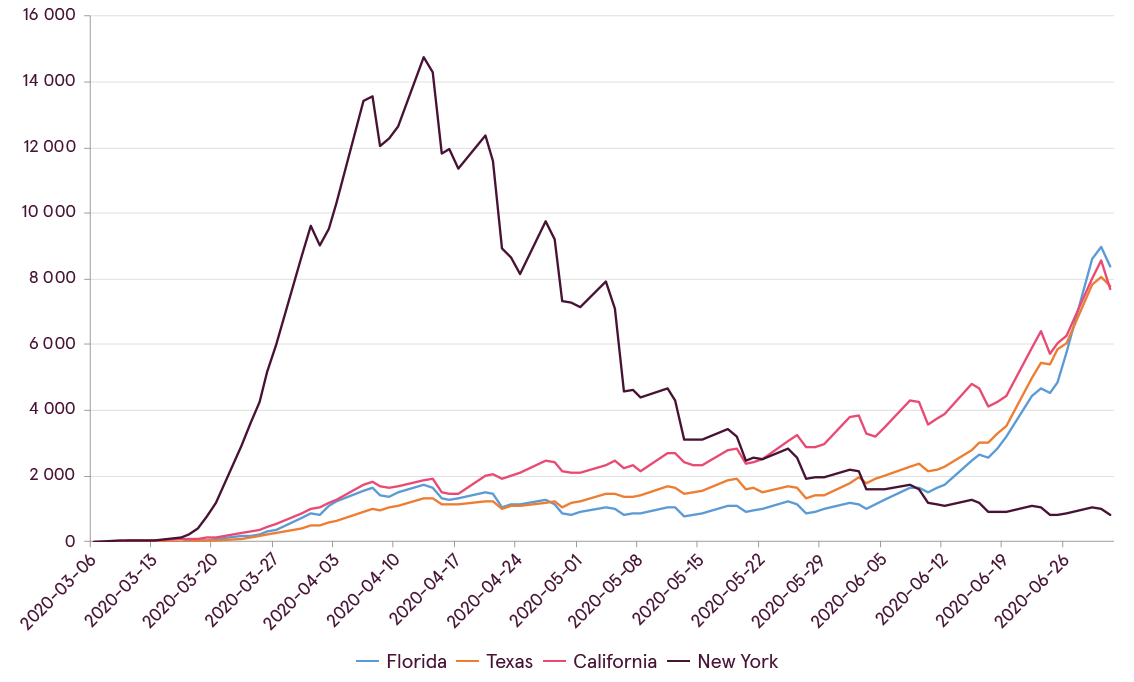

Either due to mass gatherings, not wearing masks, widespread use of air conditioning or other less known reasons, but significant acceleration in new cases was observed in large southern US states likes Texas, Florida and California, resulting in what appears to be second coronavirus wave starting in USA. This is incredibly worrisome, especially if these states have to be put on lockdown once again.

But just as it happened in February, when many hints suggested that COVID‑19 epidemic is likely to spread from China to the rest of the world, while equity markets were updating new all‑time highs, similarly today, market participants for now believe that it is temporary solvable problem. Two factors which contribute to their optimism is the fact that overall trend for number of new deaths still continues trending down and that situation in New York, state with largest amount of cases during first wave, is fully under control right now.

COVID‑19 trends in USA

Source: Bloomberg

New daily cases in selected USA states (7‑day average)

Source: Bloomberg

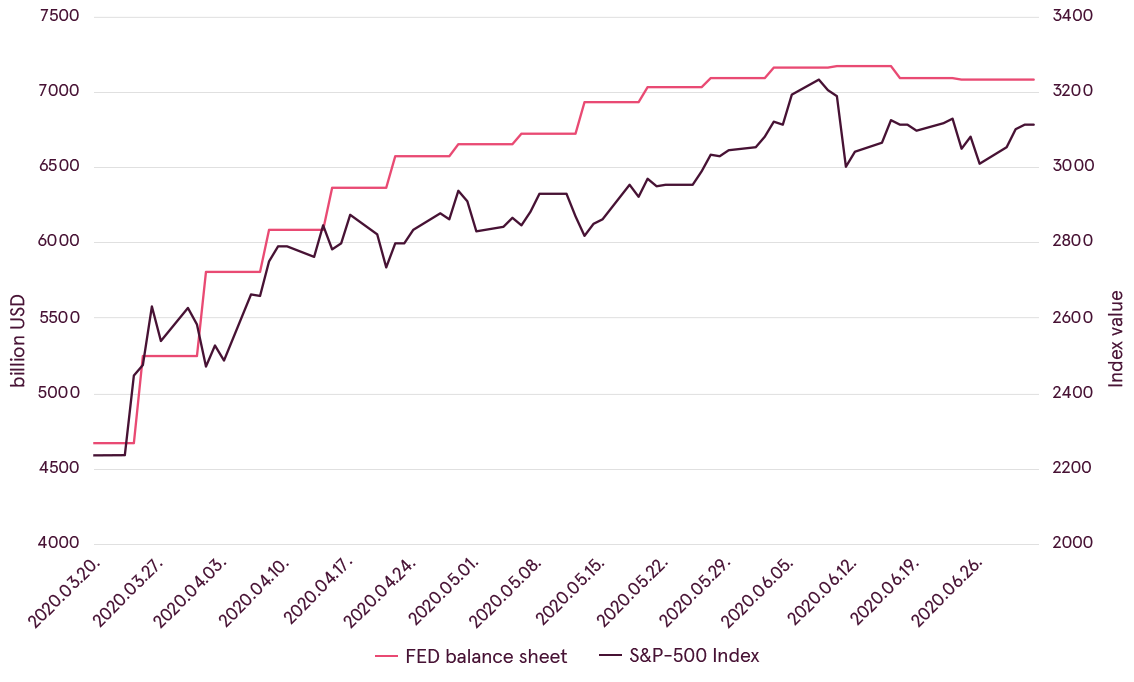

Additionally, with stabilization of financial system, return of investor optimism and increase in asset prices FED reduced usage of their emergency facilities and interventions in the market. Liquidity created by central banks was the main driver of asset price increases in spring, so not surprisingly that without newly created money, demand for assets in June also was not as strong as before.

Change in FED balance sheet and S&P‑500

Source: Bloomberg

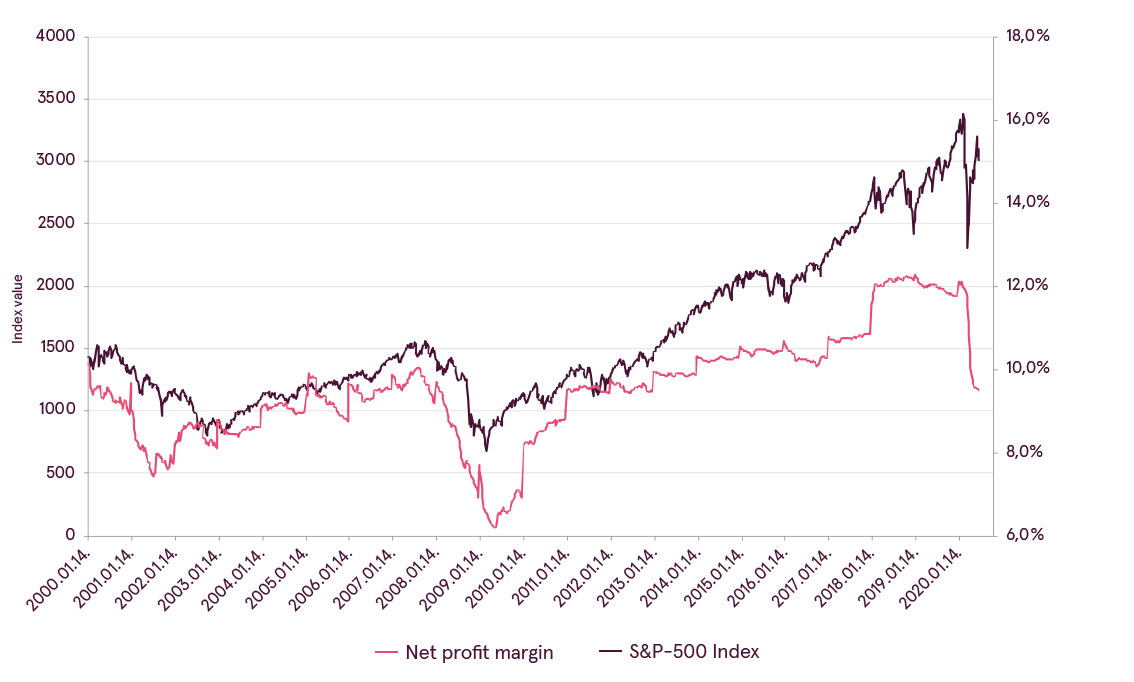

In July we expect that volatility in the markets is likely to continue. Apart from either positive or negative COVID‑19 developments, central bank stimuli and macroeconomic releases, another very important factor in July would be linked to corporate earnings. Companies will finally release their financial results for second quarter 2020, helping to understand the exact damage made from lockdown on revenues and earnings as well as to what extent those indicators improved after the reopening. Hopefully, guidance about second half of 2020 would also be provided.

S&P‑500 vs profit margin

Source: Bloomberg

Summing up, there are currently two contradictory trends, where from one side there is a new increase in COVID‑19 cases, while on the other hand we are seeing an improvement of global economic indicators. However, we must bear in mind that economic indicators are improving from extremely bad levels and in absolute terms are still far from normal. At the same time increase in COVID‑19 cases brings more uncertainty on whether there will be a new lock‑down and how fast full reopening will be achieved. In such environment it extremely hard even for companies themselves to provide any more or less reliable future guidance. This may result in big swings in analysts’ estimates of forward corporate earnings. And with equities already not cheap, this may cause big swings in prices. Therefore, investors should be prepared to embrace volatility while sticking to their long term investment plan.

1Please see June 2020 Overview for more detailed discussion on economic reasons for our cautious view

Warnings

- This Marketing Communication is not considered investment research and has not been prepared in accordance with standards applicable to independent investment research.

- This Marketing Communication does not limit or prohibit the bank or any of its employees from dealing prior to its dissemination.

Origin of the Marketing Communication

This Marketing Communication originates from the Portfolio Management unit (hereinafter referred to as PMU) – a division of Luminor Bank AS (reg. No 11315936, with registered address at Liivalaia 45, 10145, Tallinn, Republic of Estonia, represented within the Republic of Latvia by Luminor Bank AS Latvian branch, reg. No 40203154352, address: Skanstes iela 12, LV-1013, Riga, hereinafter - Luminor). PMU is involved in the provision of discretionary portfolio management services to Luminor clients.

Supervisory authority

As a credit institution Luminor is subject to supervision by the Latvian Financial Supervisory Authority (Finanšu un kapitāla tirgus komisija). Additionally, Luminor is subject to supervision by the European Central Bank (ECB), which undertakes such supervision within the Single Supervisory Mechanism (SSM), which consists of the ECB and the national responsible authorities (Council Regulation (EU) No 1024/2013 - SSM Regulation). Unless set out herein explicitly otherwise, references to legal norms refer to norms enacted by the Republic of Latvia.

Content and source of the publication

This Marketing Communication has been prepared by PMU for information purposes. Luminor will not consider recipients of this Communication as its clients and accepts no liability for use by them of the contents, which may not be suitable for their personal use.

Opinions of PMU may deviate from recommendations or opinions presented by the Luminor Markets unit. The reason may typically be the result of differing investment horizons, using specific methodologies, taking into consideration personal circumstances, applying a specific risk assessment, portfolio considerations or other factors. Opinions, price targets and calculations are based on one or more methods of valuation, for instance cash flow analysis, use of multiples, behavioural technical analyses of underlying market movements in combination with considerations of the market situation, interest rate forecasts, currency forecasts and investment horizon.

Luminor uses public sources that it believes to be reliable. However, Luminor has not performed independent verification. Luminor makes no guarantee, representation or warranty as to their accuracy or completeness. All investments entail a risk and may result in both profits and losses.

This Marketing Communication constitutes neither a solicitation of an offer nor a prospectus in the sense of applicable laws. An investment decision in respect of a financial instrument, a financial product or an investment (all hereinafter “product”) must be made on the basis of an approved, published prospectus or the complete documentation for such a product in question, and not on the basis of this document. Neither this document nor any of its components shall form the basis for any kind of contract or commitment whatsoever. This document is not a substitute for the necessary advice on the purchase or sale of a financial instrument, a financial product.

No Advice

This Marketing Communication has been prepared by Luminor PMU as general information and shall not be construed as the sole basis for an investment decision. It is not intended as a personal recommendation of particular financial instruments or strategies. Luminor accepts no liability for the use of the Marketing Communication content by its recipients.

If this Marketing Communication contains recommendations, those recommendations shall not be considered as an objective or independent explanation of the matters discussed herein. This document does not constitute personal investment advice or take into account the individual financial circumstances or objectives of the persons who receive it. The securities or other financial instruments discussed herein may not be suitable for all investors. The investor bears all risk of loss in connection with an investment. Luminor recommends that investors independently evaluate each issuer, security or instrument discussed herein and consult any independent advisors if they believe it necessary.

The information contained in this document also does not constitute advice on the tax consequences of making any particular investment decision. The estimates of costs and charges related to specific investment products are not provided therein. Each investor shall make his/her own appraisal of the tax and other financial advantages and disadvantages of his/her investment.

Risk information

The risk of investing in certain financial instruments including those mentioned in this document, is generally high, as their market value is exposed to many different factors. The value of and income from any investment may fluctuate from day to day as a result of changes in relevant economic markets (including changes in market liquidity). The information herein is not intended to predict actual results, which may differ substantially from those reflected. Past performance is not necessarily indicative of future results. When investing in individual financial instruments the investor may lose all or part of their investments.

Important disclosures of risks regarding investment products and investment services are available here.

Conflicts of interest

To avoid occurrence of potential conflicts of interest as well as to manage personal account dealing and / or insider trading, the employees of Luminor are subject to internal rules on sound ethical conduct, management of inside information, handling of unpublished research material and personal account dealing. The internal rules have been prepared in accordance with applicable legislation and relevant industry standards. Luminor’s Remuneration Policy establishes no link between revenues from capital markets activity and remuneration of individual employees.

The availability of this Marketing Communication is not associated with the amount of executed transactions or volume thereof.

This material has been prepared following the Luminor Conflict of Interest Policy, which may be viewed here.

Distribution

This Marketing Communication may not be transmitted to, or distributed within, the United States of America or Canada or their respective territories or possessions, nor may it be distributed to any U.S. person or any person resident in Canada. The document may not be duplicated, reproduced and(or) distributed without Luminor’s prior written consent.