It was too calm in July, but now volatility is returning

- After successful trade negotiations in late June, conflict between USA and China escalated yet again in early August;

- Central banks deliver on investor expectations of more monetary stimulus, but the move is broadly priced in;

- As global economy still remains soft, investors are taking profits, which leads to increased volatility

- As global bond yields continue to decline, equities are still relatively more attractive than bonds

For the most part, July was quite uneventful month for the markets. After digesting news of Trump and Xi successful meeting during G20 summit, with parties agreeing to resume negotiations to resolve trade conflict between USA and China, markets were trading sideways for the most of the July. Investors were patiently waiting what will be announced during ECB and FED meetings that were held on 25th and 31st July respectively, and preferred not to engage in trading activities before that. Another reason is that historically July is one of the quietest months throughout the year as large part of market participants go on vacation. However, since the end of the July volatility is again returning to the markets.

Key reason is that once again, just as it happened in the beginning of May, despite all previous assurances of progress in trade talks and increased hopes that US and China finally will be able to find way for mutual agreement, in early August Trump tweeted that 10% tariff on $ 300 billion of additional Chinese goods would be introduced starting from September 1st. This was unexpected move and made investors quite nervous, indicating that August might turn out to be unfavorable month for performance of financial assets (so far it is indeed the case). Another reason, why investors may be willing to take profits right now is that irrespective of news related to trade war, not many catalysts are left in the market to support further rise in equity prices at least in the perspective of next few months.

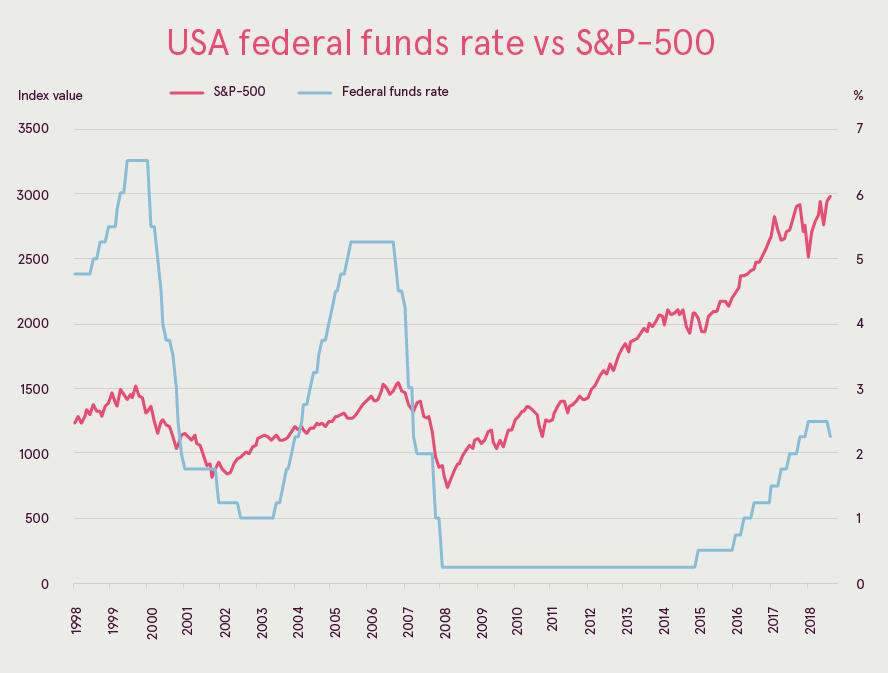

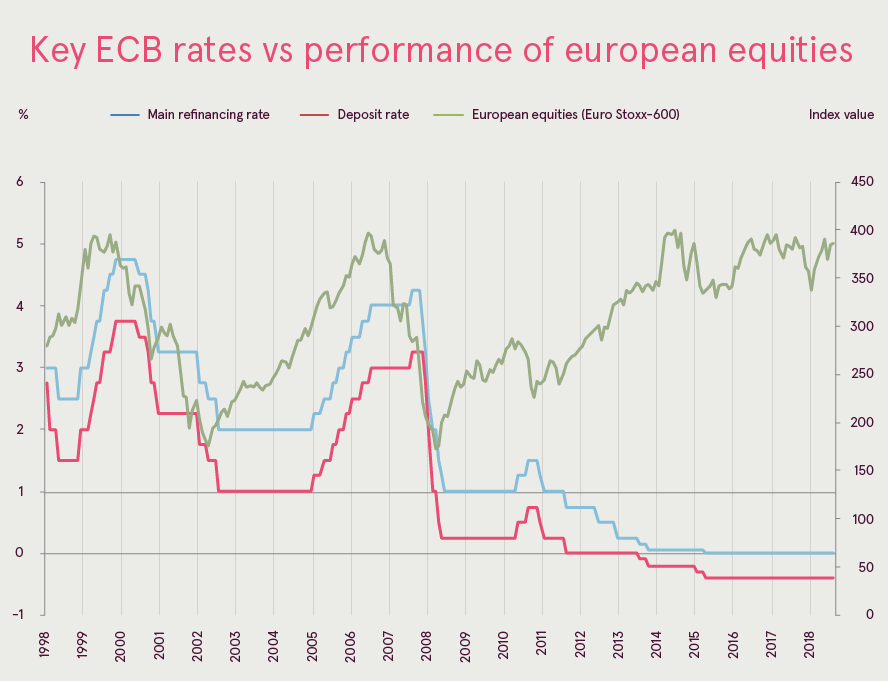

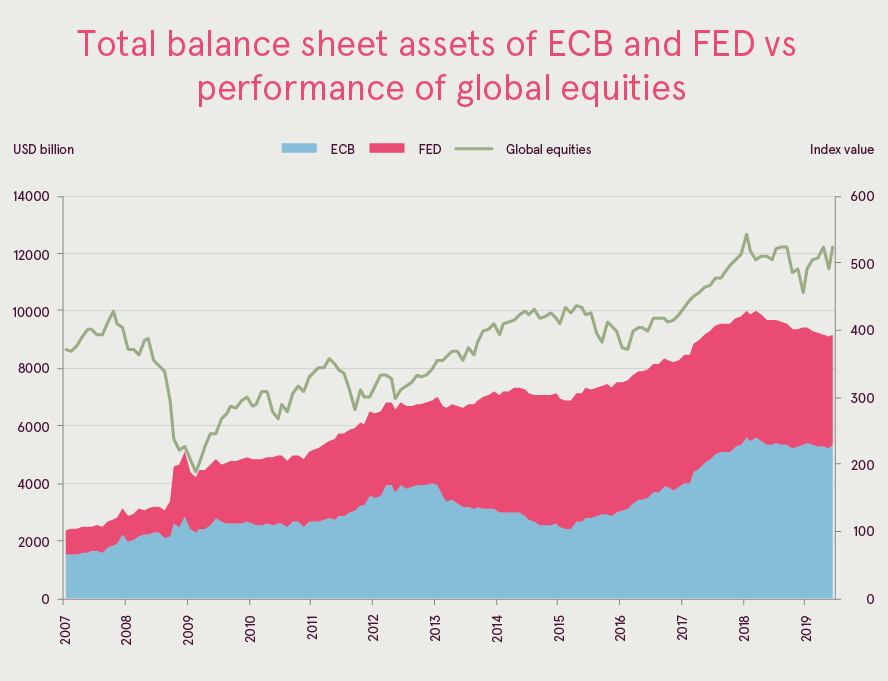

First of all, let us consider central banks, as their statements and actions are by far the major reason why performance of most financial assets was so strong this year. During July meetings, both ECB and FED delivered on what investors were expecting from them – ECB President Mario Draghi stated that given economic risks significant monetary stimulus may be introduced going forward. What it means is that in September Eurozone main refinancing interest rate is likely to be cut to negative territory for the first time ever and deposit rate would be also reduced, moreover, program of repurchasing government and corporate bonds by printing new money might be resumed later as well. At the same time, FED message did not contain just wordings, but real action, Central bank cut interest rate for the first time since 2008, and decided to halt quantitative monetary tightening already in August, two months in advance of previous plan. End of quantitative monetary tightening means that money which Central Bank is receiving at the maturity of previously purchased financial assets would again be reinvested in the market and not removed from the financial system, as it has been effectively done since 2017.

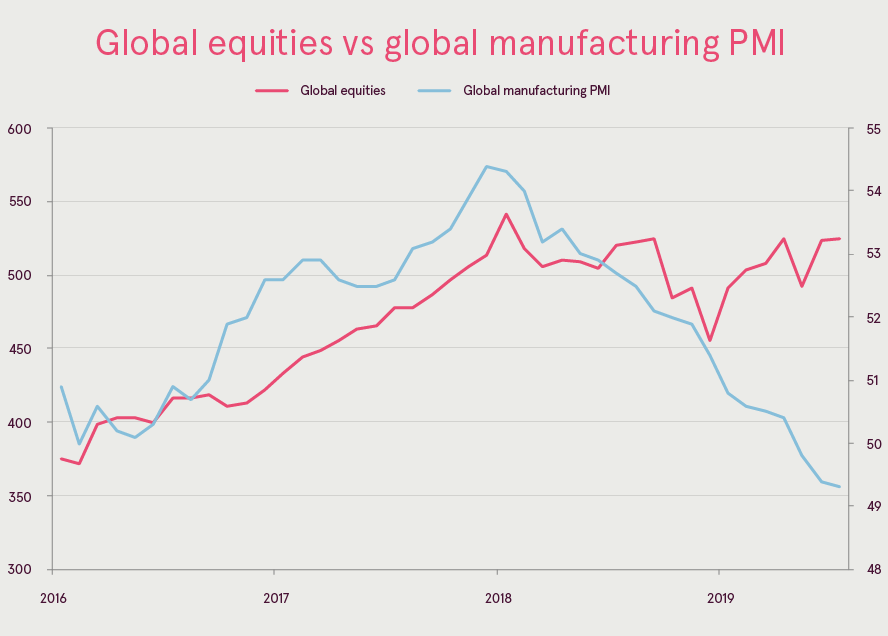

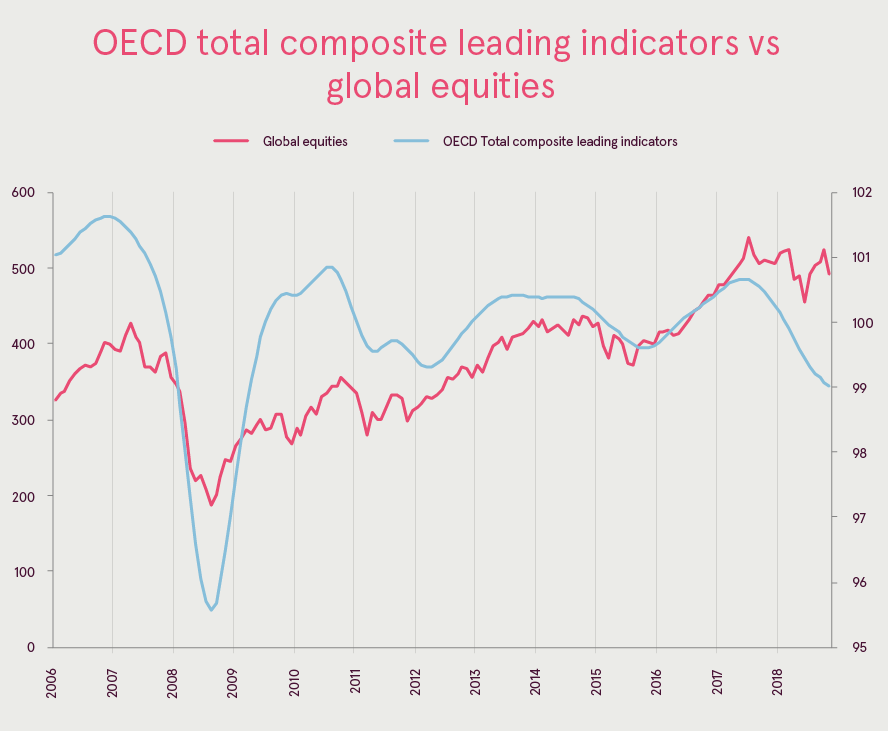

Unfortunately, such bullish news coming from monetary authorities are already in large part priced in, so even more aggressive statements by central bank heads are needed going forward this year to boost equities higher. Alternatively, global economy finally needs to start accelerating higher, and unfortunately month after month we need to acknowledge that such development is not happening. On contrary, despite several improvements here and there for some regions, in general, macroeconomic indicators worldwide continue to deteriorate. And again we need to repeat ourselves and say that risks are quite high right now and additional caution in making investments is required, especially after confirmation that trade war is still likely to continue influencing global economic growth in a negative way in the perspective of next months.

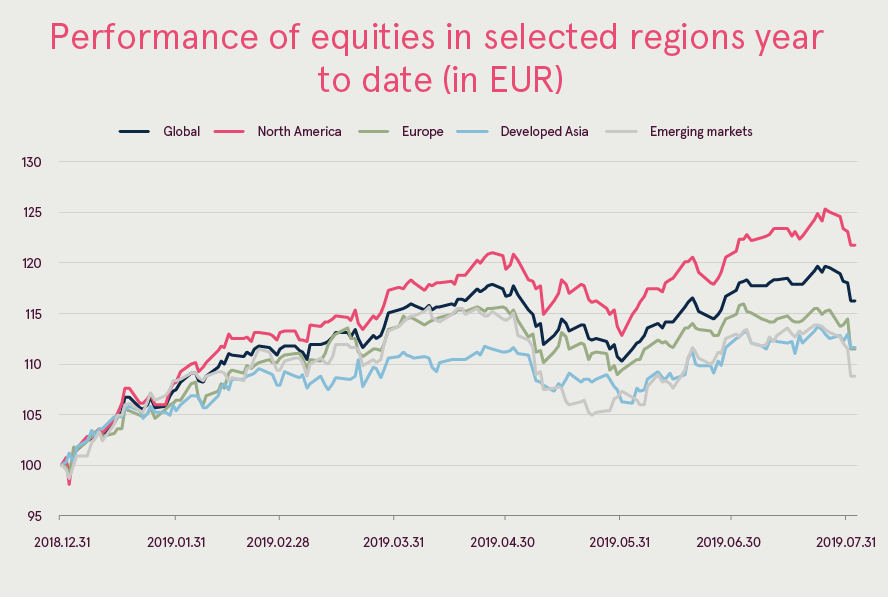

In addition, we are actually starting to observe same pattern that prevailed in the markets last year, namely USA outperforming all other major regions. Key reason is that while macroeconomic indicators both in Europe, Asia and Emerging markets are sending straightforward message that economic activity is slowing down and risk of recession is rising, in USA data continues to hold relatively well (signs of weakness are also present, but threat of negative GDP growth is not so high so far). Usually when performance of regional equity markets is becoming out of sync, it may lead to more weakness ahead, as it, for example, happened in 2018.

Another reason why US equities are experiencing better performance is linked to earnings. Number of companies beating analyst estimates in second quarter 2019 is higher in USA. If elsewhere around 50% of enterprises positively surprised analysts, in USA this percentage is close to 75%. In addition USA is basically only region, where companies are still capable to show positive growth in earnings on average. Yes, it is rather unimpressive and is equal to approximately 2%, but at least it still not negative as can be found elsewhere.

Outlook

Considering the uncertainty caused by the unresolved trade dispute and slowing global economy, global financial markets are facing some significant risks in the near term. Therefore investors should be prepared to higher volatility as the markets reacts viciously to each new piece of information regarding the trade issues, so that each new Twit by president Trump can significantly impact the markets.

| Forward P/E* | |

| Current | |

| Developed Markets ex US | 13,0 |

| All Country World Index | 14,7 |

| Europe | 12,6 |

| Emerging Markets | 11,5 |

| USA | 16,8 |

| * - price divided by the 12-m forward earnings estimate | |

| Source: Yardeni Research, Inc. | |

On the other hand looking at valuations, only the US equities are on the expensive side, while overall global equity market is only somewhat above average historical valuation, based on forward P/E. Moreover, emerging market equities are still fairly cheap compared to the historical average. Furthermore, with such low global bond yields equities continue to be relatively more attractive than bonds. However, the valuations are based on the forward earnings estimates where analysts are expecting the rebound in earnings growth by the end of this year. Such estimates are based on the assumption that the global economy will start gaining pace by the end of the year. As a result, there is a risk that earnings estimates will need to be adjusted lower, if the economy continues to slow.

All in all, the very accommodative central banks and low interest rates should support earnings growth and thus also global equities in the longer term perspective. The risks present in the short term, however, may cause significant asset price fluctuations, so investors should be prepared for that.

| Market performance | July | 2019 YTD | ||

| EUR | USD | EUR | USD | |

| Global equities (MSCI ACWI TR Net) |

2,4% | 0,3% | 20,0% | 16,6% |

| North America equities (MSCI NA TR Net) |

3,5% | 1,4% | 23,7% | 20,2% |

| European equities (MSCI Europe TR Net) |

0,3% | -1,7% | 16,6% | 13,3% |

| Pacific developed markets equities (MSCI Pacific TR Net) |

1,9% | -0,2% | 14,2% | 11,0% |

| Global Emerging Market equities (MSCI EM TR Net) |

0,8% | -1,2% | 12,4% | 9,2% |

| Government bonds (Bloomberg Barclays - Euro govt TR / US treasuries TR) |

1,7% | -0,1% | 7,8% | 5,1% |

| Investment grade corporate bonds (Bloomberg Barclays - EUR Aggr Corp TR / US corp TR) |

1,4% | 0,6% | 6,9% | 10,5% |

| Global high yield bonds, hedged (Bloomberg Barclays - Global HY TR index) |

0,6% | 0,9% | 8,8% | 10,8% |

| Emerging Market bonds, hedged (Bloomberg Barclays - EM hard currency Aggr TR hedged) |

0,8% | 1,1% | 8,3% | 10,3% |

| Oil (WTI) |

58,6 | 0,1% | 22,4% | |

| Gold | 1413,9 | 0,3% | 10,2% | |

| EUR/USD | 1,1373 | EUR: -2.6% | EUR: -3.4% | |