A new downtrend or just a correction?

- Second correction in 2018 brings global equity investors back to start of year

- Current correction in equity prices drives ACWI below 200-day moving average. Uptrend broken?

- Increased economic policy uncertainty predicts increase in equity volatility

- 77% of US companies report better than expected earnings and more than 60% beat revenue expectations

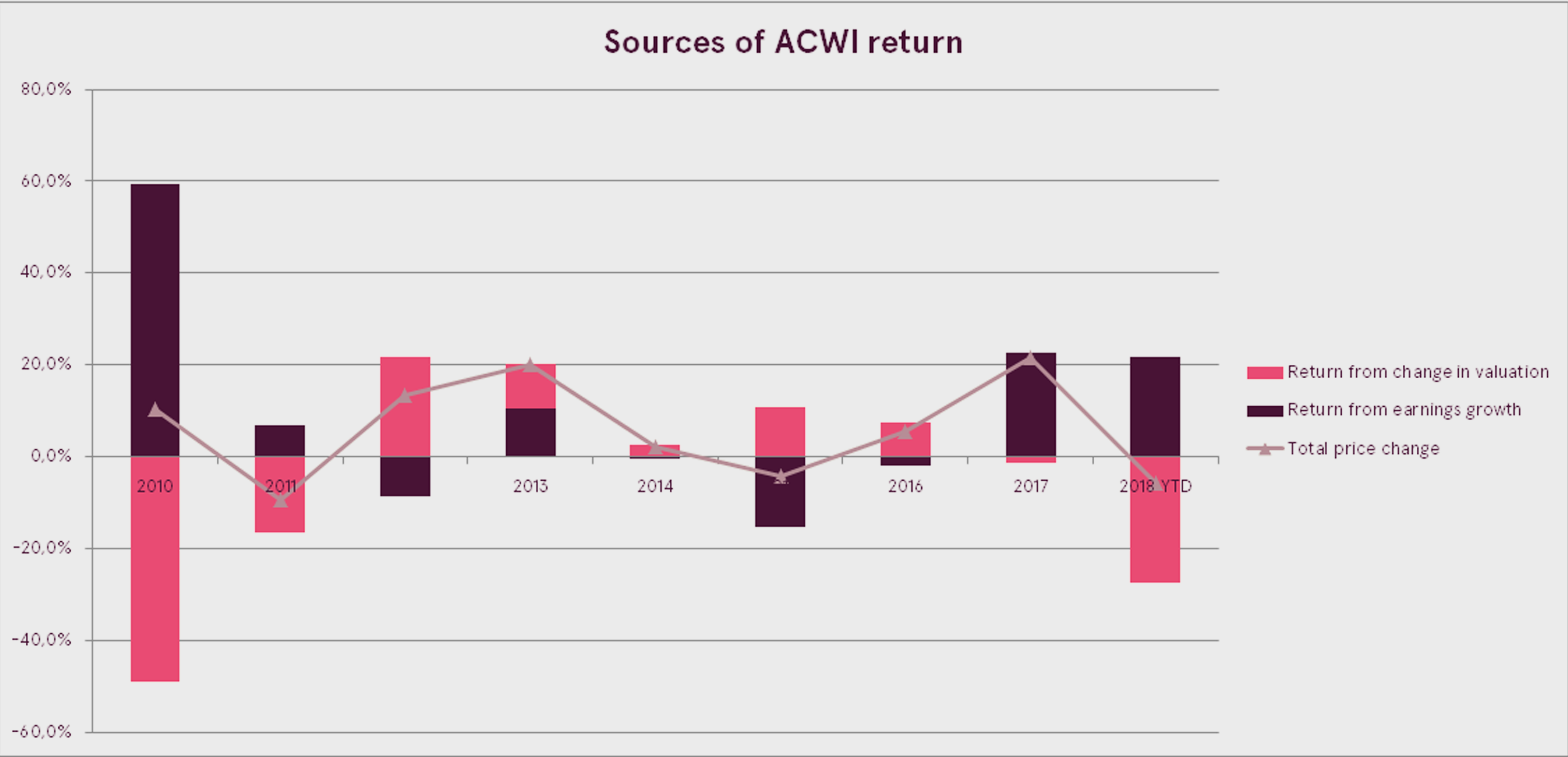

- All price gains in ACWI since start of 2017 fuelled by earnings growth

Second correction in 2018 brings global equity investors back to the start of the year

The global financial markets were marked by volatility in October as world equities began to correct after reaching new all-time highs the month before. Selling pressure, which started in the second week of October, accelerated towards the end of the month and the market was unable to rebound until the last two days of the month.

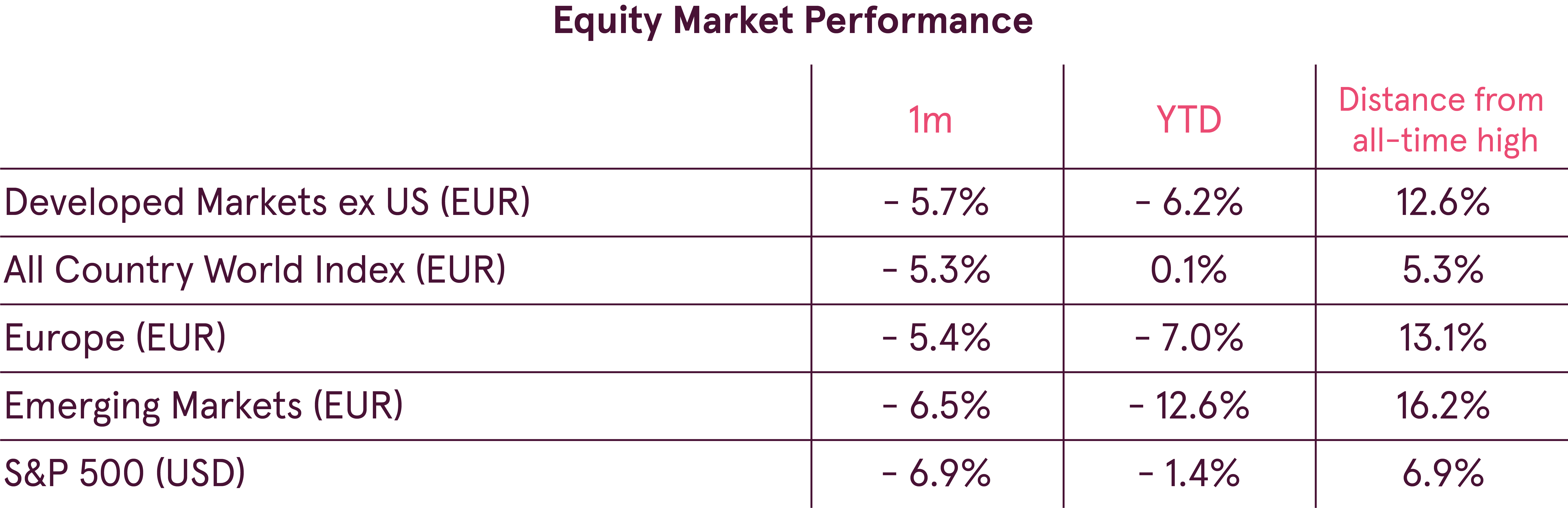

The ongoing correction is already the second this year and has pushed global equity prices to the levels seen at the start of the year. After a 5.3% slide in October, the All County World index has managed to maintain a tiny gain of 0.1% so far in 2018. If the price decline continues, 2018 may become the first year since 2011 in which world equities show negative performance. It is worth noting, however, that the ACWI is just over 5% below its record level.

The rise in interest rates in the middle of the month and the stronger USD have further damaged investor sentiment towards emerging-market equities. As a result, the emerging market equity index plunged 6.5% in October and is down over 12% this year.

US equities also suffered a significant decline, but the drop was slightly balanced by the appreciation of the USD. Nevertheless, the S&P 500 index was up 1.4% for the year at the end of October.

Did the correction break the up-trend?

As global equity prices continued their correction, investors wondered whether the longer-term uptrend had been broken. A widely used and followed indicator of the-long term trend is the 200-day moving average of the index price. If the current price is above the 200-day moving average, the index is considered to be uptrending, and if below then downtrending. The crossing of the current price above or below the moving average is considered to be an indication of the change in the trend.

Current correction in equity prices drove the ACWI below its 200-day moving average. However, this is not enough for us to conclude that the trend has changed. Looking at historical data for the ACWI, since 2000 the index has crossed its 200-day moving average 121 times. However, 81 of those times (67%) the signal turned out to be false and the trend did not reverse. Consequently, although crossing the 200-day moving average may help identify a change in the trend, the high percentage of false signals renders it an unreliable indicator.

Economic policy uncertainty causes equity market volatility

Financial markets do not like uncertainty of any kind, as it makes investors anxious and future projections harder to make. As a result, it becomes hard for investors to make rational decisions and the markets start to overreact to news and events, increasing volatility. And it is obvious that investors should be most sensitive to uncertainty in economic policy.

To measure the level of uncertainty in global economic policy, a Global Economic Policy Uncertainty index was launched (Davis, Steven J., 2016. “An Index of Global Economic Policy Uncertainty,” Macroeconomic Review, October). The index evaluates media articles on economic policy topics. The higher the value, the greater the uncertainty.

Looking at the graph above it is evident that the Global Economic Uncertainty index historically moved quite closely with the level of US equity market volatility.

As such, looking for explanations for the current market decline, increased economic policy uncertainty seems a good match. Trade war issues between the US and China, the US mid-term elections, a possible interest rate spike, the Italian debt crisis and the looming Brexit deadline have all contributed to increased uncertainty. Higher volatility did not follow immediately, but the building pressure had to dissipate sooner or later, which it did in October.

Strong earnings should help restore investor sentiment

Investor sentiment suffered severely in October in the aftermath of the turmoil on the markets. Flows to bearish bets have increased significantly and have reached extreme levels. Such an extreme level of negative sentiment is usually a contrarian indicator and would suggest that prices may rebound in the short term.

The ongoing Q3 earnings reporting season may be the catalyst that is needed to restore investor sentiment. In the US over 77% of companies are reporting better than expected earnings and over 60% are beating revenue expectations. US corporate earnings are expected to grow by an astonishing 27.1% compared to last year.

In Europe the picture is more modest, with around 50% of companies reporting better than expected earnings. Nevertheless, European corporate earnings are expected to grow by 15.8% compared to last year.

Globally, one-year earnings growth for ACWI is currently at 18.7%. More importantly, for next year the estimated earnings growth is over 10%.

Since the start of 2017 all price gains in the ACWI have been fuelled purely by earnings growth

There are two sources of the equity price change: earnings growth and change in valuation (or how much investors are willing to pay per unit of earnings). When the equity uptrend is mostly caused by an increase in the P/E multiple, equities become more expensive. Such a trend is not sustainable. Since 2017, however, all price increases in the ACWI have been driven by growth in corporate earnings. Moreover, the P/E multiple has decreased by over 20%, making global equities cheaper.

As a result, global equities are now cheaper than they were in 2016, at the same as earnings are expected to show double-digit growth next year.

Outlook

Uncertainty and risks have increased of late, hurting investor sentiment. Nevertheless, the overall picture continues to be strong. Some expected moderation in global economic growth should actually provide relief, as inflation should thus remain contained and central banks less inclined to raise rates.

Therefore, October’s turmoil looks like a normal correction, while the longer-term uptrend remains intact. Moreover, the risks are fairly balanced by potential positive developments. Should there be meaningful progress in the trade negotiations between the USA and China, the market may react very positively to the news.

Considering the positive fundamentals, but also taking into account mounting risks, we are keeping our equity allocation at neutral. At the same time, in anticipation of a gradual rate increase and due to mediocre risk/reward, we are reducing the bond allocation to underweight and increasing cash to overweight.

From the regional perspective, we are moving European equities back to neutral from overweight. At the same time, we are also increasing the Pacific equity region position to neutral. In the aftermath of the Brazilian elections and in expectation of economic reforms from the new president we are increasing Latin American equities to overweight. In addition to potentially positive economic development, Latin American equities are supported by cheap valuation.

On the fixed income side, we prefer emerging market bonds as they are still offering reasonable yield and are less sensitive to general interest rate level increases.

Disclosures and disclaimer

Origin of the publication

This publication originates from Luminor’s Investment Advice Development Department (hereinafter referred to as IAD). Luminor is supervised by the Estonian Financial Supervisory Authority (Finantsinspektsioon).

Content of the publication

This publication has been prepared solely by Anton Skvortsov, Investment Advice Development Manager.

Opinions or suggestions from the IAD unit may deviate from recommendations or opinions presented by Luminor Markets. The reason may typically be the result of differing time horizons, methodologies, contexts, risk assessments, portfolio considerations or other factors. Opinions, price targets and calculations are based on one or more methods of valuation, for instance cash flow analysis, use of multiples, behavioural technical analyses of underlying market movements in combination with considerations of the market situation, interest rate forecasts, currency forecasts and the time horizon. Key assumptions of forecasts, price targets and projections in research cited or reproduced appear in the research material from the named sources.

The date of publication appears from the research material cited or reproduced.

Opinions and estimates may be updated in subsequent versions of the publication, provided that the relevant company/issuer is treated anew in any later versions of the publication.

This publication has not been reviewed by the issuers of the relevant financial instruments mentioned in the publication prior to its publication.

Validity of the publication

All opinions and estimates in this publication are, regardless of source, given in good faith, may only be valid as of the stated date of this publication and are subject to change without notice.

No individual investment or tax advice

The publication is intended only to provide general and preliminary information to investors and shall not be construed as the sole basis for an investment decision.

This publication has been prepared by Luminor as general information for private use of investors to whom the publication has been distributed, but is not intended as a personal recommendation of particular financial instruments or strategies and thus it does not provide individually tailored investment advice, and does not take into account your particular financial situation, existing holdings or liabilities, investment knowledge and experience, investment objective and horizon or risk profile and preferences. The investor must particularly ensure the suitability of his/her investment as regards his/her financial and fiscal situation and investment objectives.

The investor bears all risks of losses in connection with an investment. Before acting on any information in this publication, it is recommended to examine the specific terms and conditions of investment products or services and consult one’s financial advisor.

The information contained in this publication does not constitute advice on tax consequences of making any particular investment decision. Each investor shall make his/her own appraisal of the tax and other financial advantages and disadvantages of his/her investment.

Sources

This publication may be based on and contain information, such as opinions, recommendations, estimates, price targets and valuations which emanate from: IAD, publicly available information, information from other units of Luminor or other named sources. Luminor has deemed the Other Sources to be reliable but does not guarantee the accuracy, adequacy or completeness of the External Information.

The stated prices are the closing prices at the stock exchange unless expressly stated otherwise. The perception of opinions or recommendations such as Buy/Sell or similar comparable expressions may vary depending on, for example, the source and the type of financial instrument in focus, and the definition is therefore where appropriate shown in the research material or on the website of each named source.

Limitation of liability

The liability of Luminor may not be engaged as regards any investment, divestment or retention decision taken by the investor on the basis of this publication. Luminor shall not be liable for direct, indirect or incidental, special or consequential damages resulting from the information in this publication regardless of whether such damages were foreseeable or unforeseeable.

Risk information

The risk of investing in certain financial instruments, including those mentioned in this document, is generally high, as their market value is exposed to many different factors such as the operational and financial conditions of the relevant company/issuer, growth prospects, change in interest rates, the economic and political environment, foreign exchange rates, changes in credit rating, liquidity in the market, shifts in market sentiments, etc. In case of a company´s/issuer’s insolvency or similar circumstance there may be periods when the financial instrument issued by the company/ issuer cannot be traded. Where an investment or security is denominated in a different currency than the investor’s currency of reference, changes in rates of exchange may have a positive or negative effect on the value, price or income of or from that investment to the investor. Important disclosures of risks regarding investment products and investment services are available here.

Past performance is not a guide to future performance. Estimates of future performance are based on assumptions that may not be realized. When investing in individual financial instruments the investor may lose all or part of his investments.

Conflicts of interest

Luminor may perform services for, solicit business from, hold long or short positions in, or otherwise be interested in the investments (including derivatives) of any company mentioned in the publication.

To limit possible conflicts of interests and counter the abuse of insider knowledge, the advisors and strategists in Luminor are subject to internal rules on sound ethical conduct, the management of inside information, handling of unpublished research material, contact with other units and personal account dealing. The internal rules have been prepared in accordance with applicable legislation and relevant industry standards. The object of the internal rules is, for example, to ensure that (i) no advisor or strategist will abuse or cause others to abuse confidential information, (ii) a physical separation exists between advisors and strategists involved in the production of this publication and other relevant persons whose responsibilities or business interests may conflict with the interests of the persons to whom the investment research is disseminated, (iii) advisors and strategists involved in the production of this publication act in good faith, etc.

It is the policy of Luminor that no link exists between revenues from capital markets activity and individual advisor or strategist remuneration. Luminor does not promise issuers favourable research coverage. The availability of this publication is not associated with the amount of executed transactions or volume thereof.

This material has been prepared following the Luminor Conflict of Interest Policy, which may be viewed here.

Information about personal shareholdings of Luminor advisers and strategists will be disclosed at Luminor’s web page if this issue becomes relevant.

Distribution

This publication does not constitute an offer of services in any jurisdiction where Luminor does not have the necessary license. The securities referred to in this publication may not be eligible for sale in some jurisdictions. This publication is generally public but is intended only for distribution in Estonia, Latvia and Lithuania.

This publication may be distributed by Luminor Estonia, Latvia and Lithuania.

This publication may not be mechanically duplicated, photocopied or otherwise reproduced, in full or in part, under applicable copyright laws.