Possibility of higher inflation – risk for certain assets, but opportunity for the other

Expected fiscal stimulus and encouraging COVID trends continued boosting equity prices higher in February; but by the end of the month rising treasury yields put such rally on hold;

Rising Inflation expectations were largely responsible for correction in bond markets, but also for very diverse performance in equity space

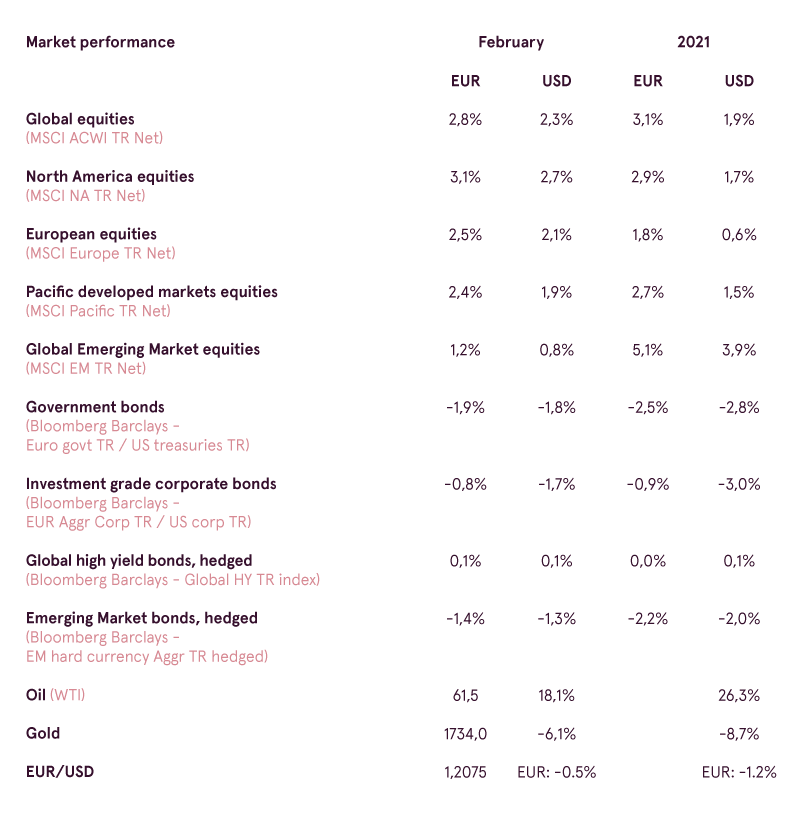

To a large extent global equity performance in February resembled January developments. During most of the month indices rallied higher to new all-time highs for similar reasons as in January – upcoming 1.9 trillion stimulus bill and COVID trend improvements. However, by March large part of these gains did not hold. And if key reason for late month sell-off in January was related to financial risks associated with Gamestop ‘’short squeeze” saga, this time negative impact was mainly linked to developments observed in bond markets.

Performance of global equities (MSCI ACWI EUR index

Source: Bloomberg

In last report we already mentioned how rising bond yields may negatively impact “growth” equities through revaluation of their fair value, and unfortunately this risk materialized during second half of last month. As previously discussed, new fiscal stimulus bill should significantly increase supply of treasuries in USA, and if it is not balanced by the same increase in demand, it is natural for treasury yields to rise. Moreover, negative impact on price of bonds and not just in USA, but globally may come from rising inflation expectations.

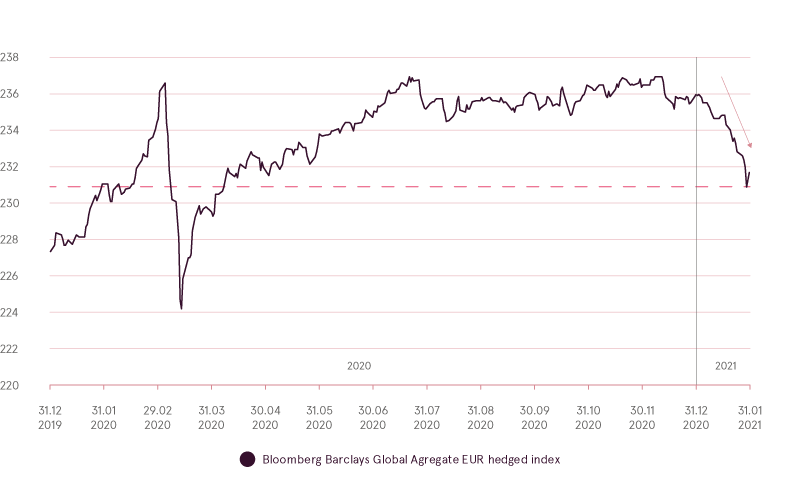

Performance of global bonds

Source: Bloomberg

Worry about rising inflation comes from already observed supply shortages for certain goods like semiconductor chips or various commodities. Such shortages are mainly explained by the fact that due to government fiscal support, which did not reduce personal income and capacity to spend during pandemic despite recession, demand for certain goods continues to be strong. Meanwhile, lockdowns put some limitations on available supply and manufacturing capacity.

But in addition to existing inflation pressures, there is maybe even bigger fear that when economies would reopen, demand for yet unavailable in lockdown goods and services would be so significant that their prices would immediately and drastically jump. For example, when borders would be reopened and air travelling fully allowed, desire to have vacation abroad may be so strong and widespread among population that there would be both not enough plane tickets available for everyone, as well as larger indifference as to what amount of money to pay. And this is just one of many examples how spike in inflation may be realized.

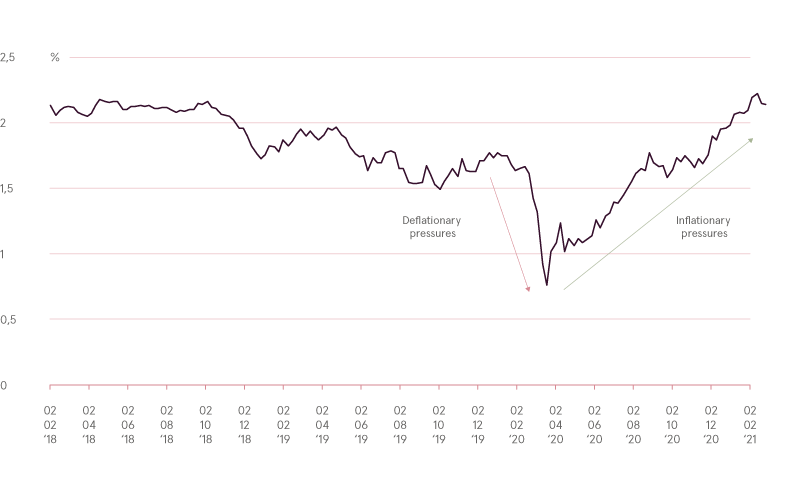

US 10-year expected inflation rate

Source: Bloomberg

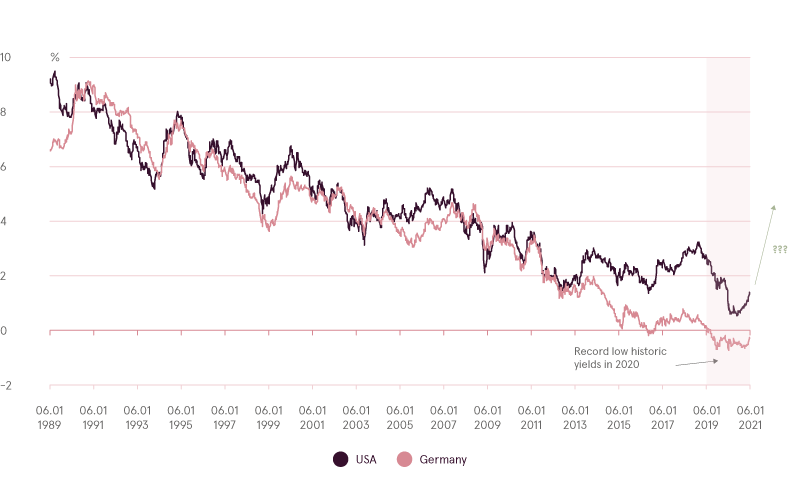

So with each month bond investors are becoming more and more concerned that rising inflation expectations may actually cause FED and other central banks start thinking about shifting their monetary policy from easing to tightening much sooner than it was previously expected. From historic perspective global bond yields still remain close to record low “zero” levels (or even negative as for European treasuries), and if with time inflation concerns indeed would cause central banks to raise rates, negative impact on bond prices (especially, those with higher duration) can be very prolonged and significant.

Long term trend in 10-year treasury yields

Source: Bloomberg

But let us return to equity markets. Indeed, since mid-February on revaluation concerns “growth” stocks, predominantly found in IT and consumer discretionary sectors, had one of the worst short-term performances since last March. From this perspective, not surprising that absolutely worst performance in S&P-500 index was shown by one of the main 2020 and “growth story” leaders – Tesla, which declined by 23.5% throughout the month. And another one of the worst performances was shown by even more stable 2020 leader – Apple, which declined by 15.3%. So the question you are probably asking, if performance of leading 2020 names was so poor throughout February, why on balance global indices still managed to show positive month?

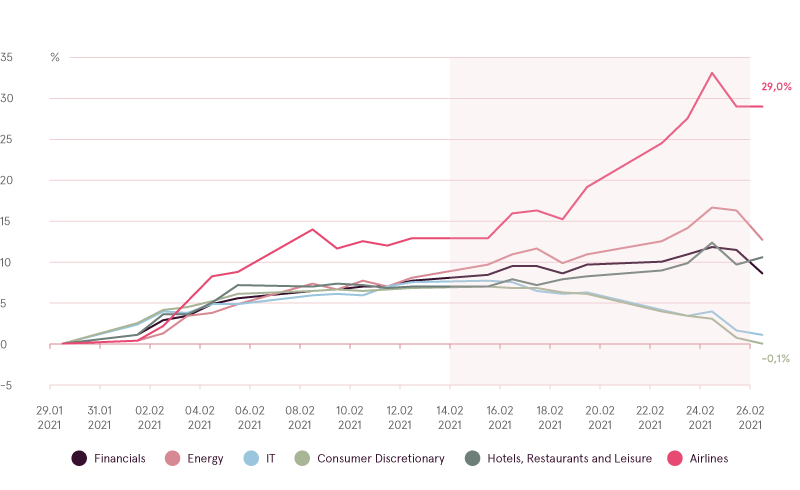

The explanation comes from the fact that though rising bond yields negatively impact “growth” companies, it usually positively impact cheaper “value” companies, which often are cyclical in nature and can benefit from higher inflation and return of more stable economic growth (which is expected to happen when countries finally remove all lockdown measures). Indeed, February was very positive month for these “inflation protection” ideas, as sectors such as energy and financials increased by 13% and 9%, and one of the best performances was shown, for example, by airlines and cruise ship stocks. And that plane ticket analog we mentioned earlier should help to understand why.

Performance of selected sectors in February

Source: Bloomberg

However, as global equity index composition is still tilted towards “growth” sectors like IT and communications, global equity indices may on balance still decline in price, if yields would continue to rise. On the contrary, if central banks will be able to stabilize bond markets in March, we might see once again outperformance of high growth equity stories.

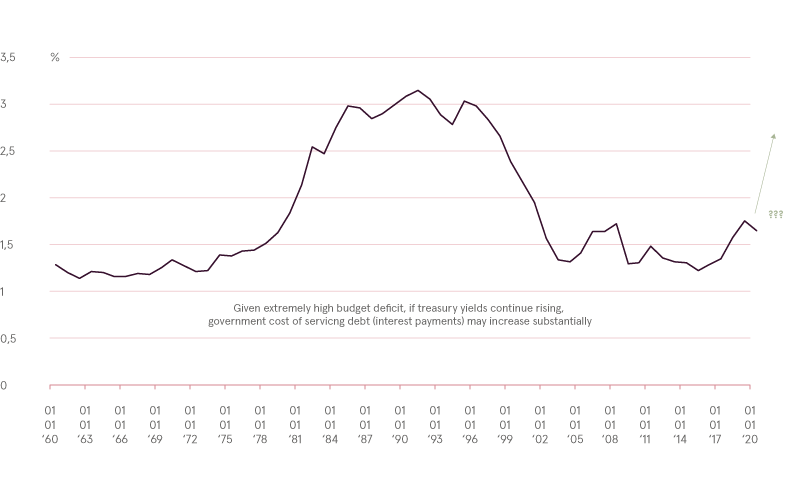

Therefore, despite late February sell-off and mentioned risks, for March we remain relatively optimistic. Markets still are likely to be dominated by passing of new $1.9 trillion US fiscal bill, which should stimulate both spending and savings, latter also partially going to financial markets, creating extra demand for risky assets. Meanwhile, if developments in bond markets would start to get out of control FED would probably act to stabilize and put a cap on further increase in treasury yields. Reason is that, given massive budget deficit, unlikely that US authorities would allow budget debt servicing costs to increase significantly, at least for a while and at least until actual inflation indeed becomes exceedingly high. Finally COVID-19 vaccination process is on track and existing decline in spread of virus is very encouraging. Therefore, it may be hoped that lifting of lockdown restrictions might be just around the corner.

US federal outlays interest as % o GDP

Source: Bloomberg

Warnings

- This Marketing Communication is not considered investment research and has not been prepared in accordance with standards applicable to independent investment research.

- This Marketing Communication does not limit or prohibit the bank or any of its employees from dealing prior to its dissemination.

Origin of the Marketing Communication

This Marketing Communication originates from the Portfolio Management unit (hereinafter referred to as PMU) – a division of Luminor Bank AS (reg. No 11315936, with registered address at Liivalaia 45, 10145, Tallinn, Republic of Estonia, represented within the Republic of Latvia by Luminor Bank AS Latvian branch, reg. No 40203154352, address: Skanstes iela 12, LV-1013, Riga, hereinafter - Luminor). PMU is involved in the provision of discretionary portfolio management services to Luminor clients.

Supervisory authority

As a credit institution Luminor is subject to supervision by the Latvian Financial Supervisory Authority (Finanšu un kapitāla tirgus komisija). Additionally, Luminor is subject to supervision by the European Central Bank (ECB), which undertakes such supervision within the Single Supervisory Mechanism (SSM), which consists of the ECB and the national responsible authorities (Council Regulation (EU) No 1024/2013 - SSM Regulation). Unless set out herein explicitly otherwise, references to legal norms refer to norms enacted by the Republic of Latvia.

Content and source of the publication

This Marketing Communication has been prepared by PMU for information purposes. Luminor will not consider recipients of this Communication as its clients and accepts no liability for use by them of the contents, which may not be suitable for their personal use.

Opinions of PMU may deviate from recommendations or opinions presented by the Luminor Markets unit. The reason may typically be the result of differing investment horizons, using specific methodologies, taking into consideration personal circumstances, applying a specific risk assessment, portfolio considerations or other factors. Opinions, price targets and calculations are based on one or more methods of valuation, for instance cash flow analysis, use of multiples, behavioural technical analyses of underlying market movements in combination with considerations of the market situation, interest rate forecasts, currency forecasts and investment horizon.

Luminor uses public sources that it believes to be reliable. However, Luminor has not performed independent verification. Luminor makes no guarantee, representation or warranty as to their accuracy or completeness. All investments entail a risk and may result in both profits and losses.

This Marketing Communication constitutes neither a solicitation of an offer nor a prospectus in the sense of applicable laws. An investment decision in respect of a financial instrument, a financial product or an investment (all hereinafter “product”) must be made on the basis of an approved, published prospectus or the complete documentation for such a product in question, and not on the basis of this document. Neither this document nor any of its components shall form the basis for any kind of contract or commitment whatsoever. This document is not a substitute for the necessary advice on the purchase or sale of a financial instrument, a financial product.

No Advice

This Marketing Communication has been prepared by Luminor PMU as general information and shall not be construed as the sole basis for an investment decision. It is not intended as a personal recommendation of particular financial instruments or strategies. Luminor accepts no liability for the use of the Marketing Communication content by its recipients.

If this Marketing Communication contains recommendations, those recommendations shall not be considered as an objective or independent explanation of the matters discussed herein. This document does not constitute personal investment advice or take into account the individual financial circumstances or objectives of the persons who receive it. The securities or other financial instruments discussed herein may not be suitable for all investors. The investor bears all risk of loss in connection with an investment. Luminor recommends that investors independently evaluate each issuer, security or instrument discussed herein and consult any independent advisors if they believe it necessary.

The information contained in this document also does not constitute advice on the tax consequences of making any particular investment decision. The estimates of costs and charges related to specific investment products are not provided therein. Each investor shall make his/her own appraisal of the tax and other financial advantages and disadvantages of his/her investment.

Risk information

The risk of investing in certain financial instruments including those mentioned in this document, is generally high, as their market value is exposed to many different factors. The value of and income from any investment may fluctuate from day to day as a result of changes in relevant economic markets (including changes in market liquidity). The information herein is not intended to predict actual results, which may differ substantially from those reflected. Past performance is not necessarily indicative of future results. When investing in individual financial instruments the investor may lose all or part of their investments.

Important disclosures of risks regarding investment products and investment services are available here.

Conflicts of interest

To avoid occurrence of potential conflicts of interest as well as to manage personal account dealing and / or insider trading, the employees of Luminor are subject to internal rules on sound ethical conduct, management of inside information, handling of unpublished research material and personal account dealing. The internal rules have been prepared in accordance with applicable legislation and relevant industry standards. Luminor’s Remuneration Policy establishes no link between revenues from capital markets activity and remuneration of individual employees.

The availability of this Marketing Communication is not associated with the amount of executed transactions or volume thereof.

This material has been prepared following the Luminor Conflict of Interest Policy, which may be viewed here.

Distribution

This Marketing Communication may not be transmitted to, or distributed within, the United States of America or Canada or their respective territories or possessions, nor may it be distributed to any U.S. person or any person resident in Canada. The document may not be duplicated, reproduced and(or) distributed without Luminor’s prior written consent.