If fears of recession do not materialize, expect euphoria to continue during 2020 as well | Luminor

If fears of recession do not materialize, expect euphoria to continue during 2020 as well

Atis Krūmiņš

Head of Investment Management

- Despite global economic slowdown, trade tensions and subpar fundamentals, global equities demonstrated best performance since 2009, rising in US dollar terms by 24%;

- In contrast to 2018, majority of financial assets yielded positive return during 2019, boosted by declining interest rates and central bank easing policies;

- 2020 is complex year for financial forecasting, as most extreme positive and negative scenarios are capable to materialize;

- A balanced and diversified approach with a long term focus should help cope with potentially increased price volatility and take advantage of potential opportunities in the market.

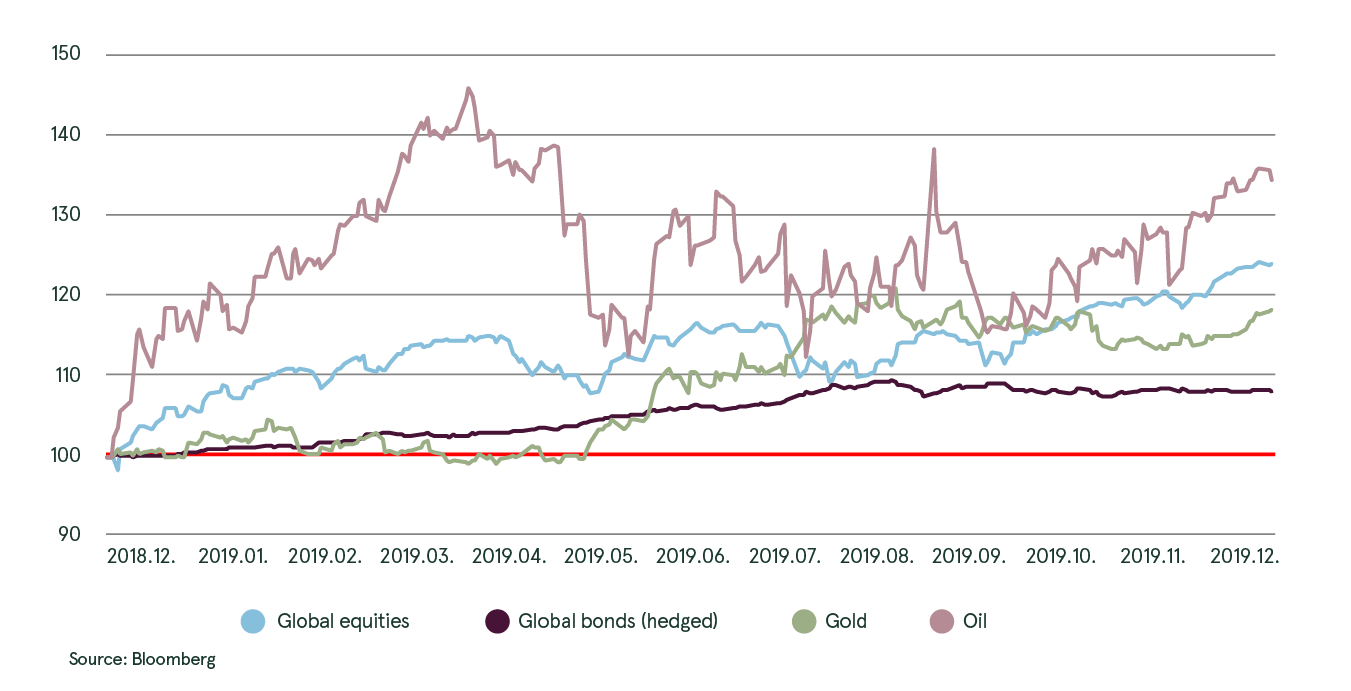

In many regards last year was rather exceptional. We witnessed worst global macroeconomic data since 2008 financial crisis, with many indicators sending clear message that risk of economic recession is high1. Equity fundamentals also did not improve, growth in global corporate earnings has stalled and future outlook by many companies was revised lower. Meanwhile global equity indexes have really prospered throughout the year, showing strongest performance since 2009, while other financial assets, such as bonds and commodities, have also increased in price.

Performance of selected assets in 2019 (in USD)

Reason why we observed such controversial behavior in the market, with asset prices not fully reflecting what was predicted by economic theory and similar historic precedents is straightforward. Investors believed that by pouring additional liquidity into financial system, central banks would be able to prevent economic recession, and even revive healthy economic growth. Investors also believed that trade tensions between USA and China would end in finding mutual compromise, reducing uncertainty and reestablishing favorable conditions for growth in global trade. Therefore, all growth in equity prices throughout 2019 was based on very favorable expectations of what will happen to global economy throughout 2020-2021.

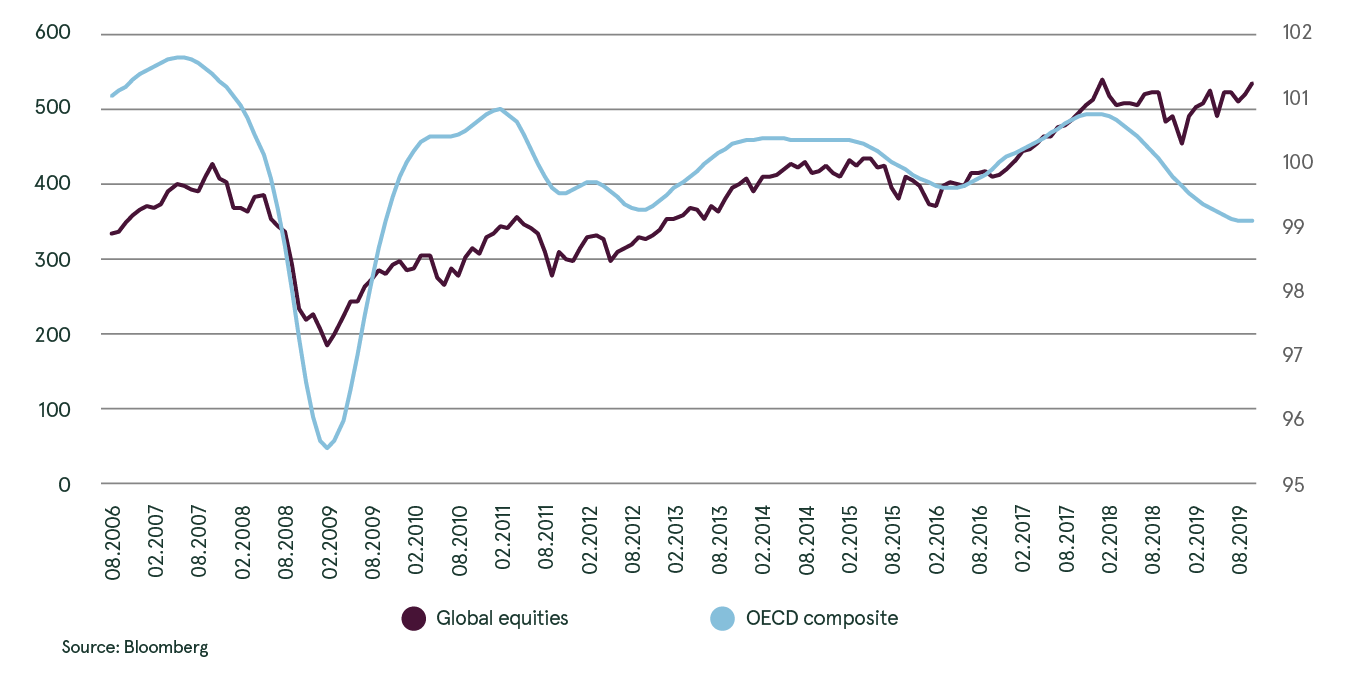

Global liquidity and performance of global equities in 2019

However, we have chosen to maintain a cautious stance during all 2019, as large share of economic indicators continued to deteriorate and similarities to 2008 were too high to ignore them.

OECD total composite leading indicators vs global equities

But going into 2020, situation is becoming more complicated for the analysis. From one perspective, majority of risk factors that were present throughout 2019 still remain, and thus economic recession and crash in the financial markets cannot be ruled out. From another perspective, thanks to continuous central bank liquidity injections, together with resolution in politic tensions (trade dispute, Brexit), there are good odds that global recession might be postponed for couple more years. In this scenario, investor euphoria that has started in 2019 might reach rather extreme levels, and equities will be capable to experience parabolic rise, even if rationally there are no sound logic for such development.

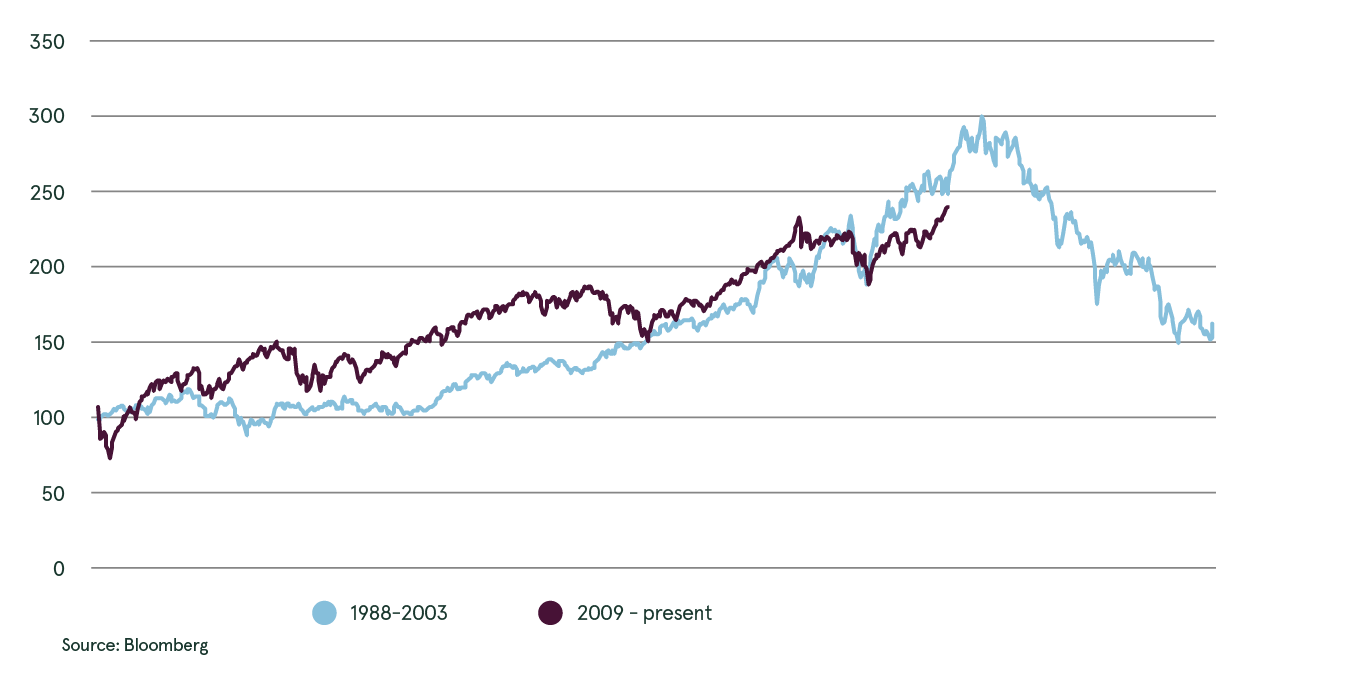

If we analyze latter scenario from historic perspective, current situation is very similar to what was happening in the markets 20 years ago. At that time, Asian financial crisis and Russian debt default in August 1998 triggered fear of global economic recession among the investors, with global equities dropping by around 20% in 3 months (similar to how markets moved in Q4 2018). Global central banks reacted immediately by implementing expansionary monetary actions, and just like in 2019 FED cut interest rate 3 times during that time. As a result, late economic cycle was prolonged for few more years, while cheaper liquidity stimulated extreme investor optimism. It led to formation of “dot-com bubble”, with IT stocks and Nasdaq rising by more than 200% in less than two years, and global equities increasing by around 55% during that time. Drawing parallel to 1998-2000, 2020 thus may become another very strong year, especially if global economy stops slowing down (similar to what happened in 1999).

Performance of global equities in selected timeframes

However, it is very important to understand that even if monetary stimuli would work, and global growth rebounds, it is unlikely to be strong and last for prolonged period of time. Key reason is that in many countries production capacity is becoming rather limited. For example, in USA unemployment rate is already lowest in 50 years, so finding additional workers is becoming real challenge right now. At the same time, thanks to central bank actions financing is becoming cheaper and more available. As a result, in such environment, we might see economic “overheating”, when supply is unable to fully satisfy demand, leading to rise in inflation. Central banks would have to start fighting inflation by raising interest rates, and in such conditions, almost certainly recession would start. If we again return to our historic example, this is exactly what happened in 2000.

So as paradoxically as it may sound, there are good reasons for 2020 to turn out as either extremely good or extremely bad year for investments. Therefore a balanced and diversified approach with a long term focus should help cope with potentially increased price volatility and take advantage of potential opportunities in the market. Moreover, after a great year for almost all asset classes it is reasonable to expect that not all of them will perform as well this year. However, there are still areas with good potential for relative outperformance worth mentioning: precious metals and cheap “value” stocks. For example, gold mining stocks may generate positive results both during times of recession and times of high inflation due to exposure to precious metals. In times of market instability and rising global risks, investors seek protection by moving into “safe assets”, therefore, demand for gold tends to increase, and price of metal tends to move higher. At the same time, when markets are stable, but there is pick-up in inflation, gold should act for investors as hedge against decline in currency’s purchasing power, therefore metal is also likely to rise in price.

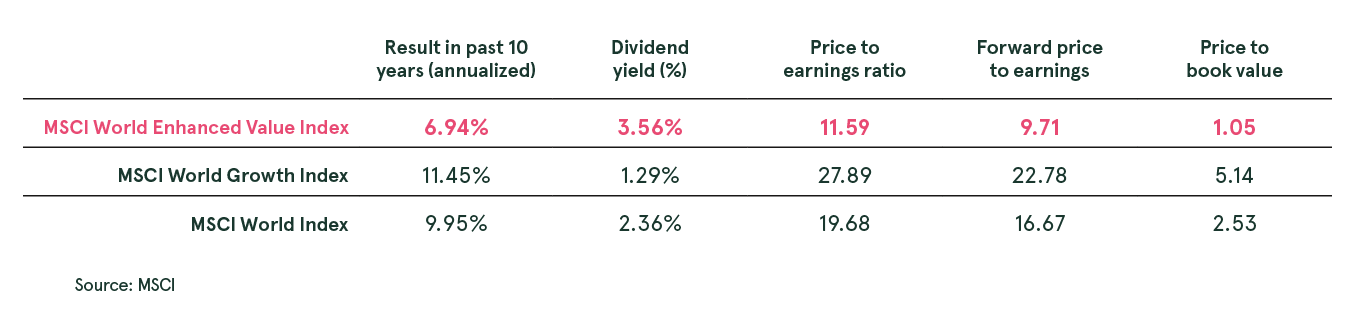

Although overall equity valuations have gone up last year there are still pockets of reasonably priced stocks within global equity markets. For example the whole Emerging Market region is trading at a CAPE (cyclically adjusted price per earnings) of 13.1, which is significantly below its median level of 15.4 (according to researchaffiliates.com data). Additionally, there are also cheap stocks within other regions, which are referred to as “Value” stocks. These stocks tend to have lower valuation multiples, higher dividend yield and higher share of tangible assets on their balance sheet. Since 2007, “value” ideas tended to underperform the market, but right now their relative valuation is becoming too cheap to ignore, and since august 2019 these stocks finally started to see significant fund inflows and stronger relative performance. Overall, if global economy would rebound, these stocks have good odds to rise more than the rest of the market, to close the ‘’valuation gap”. But even if there is recession and market corrects, investment in these equities should provide solid margin of safety compared to rest of the market, as intrinsic value of these companies is likely to be revised less severely down compared to other stocks.

Value vs growth vs market

Market performance

1We discussed some of these indicators in more detail throughout our monthly reports in 2019

Warnings

- This Marketing Communication is not considered investment research and has not been prepared in accordance with standards applicable to independent investment research.

- This Marketing Communication does not limit or prohibit the bank or any of its employees from dealing prior to its dissemination.

Origin of the Marketing Communication

This Marketing Communication originates from the Portfolio Management unit (hereinafter referred to as PMU) – a division of Luminor Bank AS (reg. No 11315936, with registered address at Liivalaia 45, 10145, Tallinn, Republic of Estonia, represented within the Republic of Latvia by Luminor Bank AS Latvian branch, reg. No 40203154352, address: Skanstes iela 12, LV-1013, Riga, hereinafter - Luminor). PMU is involved in the provision of discretionary portfolio management services to Luminor clients.

Supervisory authority

As a credit institution Luminor is subject to supervision by the Latvian Financial Supervisory Authority (Finanšu un kapitāla tirgus komisija). Additionally, Luminor is subject to supervision by the European Central Bank (ECB), which undertakes such supervision within the Single Supervisory Mechanism (SSM), which consists of the ECB and the national responsible authorities (Council Regulation (EU) No 1024/2013 - SSM Regulation). Unless set out herein explicitly otherwise, references to legal norms refer to norms enacted by the Republic of Latvia.

Content and source of the publication

This Marketing Communication has been prepared by PMU for information purposes. Luminor will not consider recipients of this Communication as its clients and accepts no liability for use by them of the contents, which may not be suitable for their personal use.

Opinions of PMU may deviate from recommendations or opinions presented by the Luminor Markets unit. The reason may typically be the result of differing investment horizons, using specific methodologies, taking into consideration personal circumstances, applying a specific risk assessment, portfolio considerations or other factors. Opinions, price targets and calculations are based on one or more methods of valuation, for instance cash flow analysis, use of multiples, behavioural technical analyses of underlying market movements in combination with considerations of the market situation, interest rate forecasts, currency forecasts and investment horizon.

Luminor uses public sources that it believes to be reliable. However, Luminor has not performed independent verification. Luminor makes no guarantee, representation or warranty as to their accuracy or completeness. All investments entail a risk and may result in both profits and losses.

This Marketing Communication constitutes neither a solicitation of an offer nor a prospectus in the sense of applicable laws. An investment decision in respect of a financial instrument, a financial product or an investment (all hereinafter “product”) must be made on the basis of an approved, published prospectus or the complete documentation for such a product in question, and not on the basis of this document. Neither this document nor any of its components shall form the basis for any kind of contract or commitment whatsoever. This document is not a substitute for the necessary advice on the purchase or sale of a financial instrument, a financial product.

No Advice

This Marketing Communication has been prepared by Luminor PMU as general information and shall not be construed as the sole basis for an investment decision. It is not intended as a personal recommendation of particular financial instruments or strategies. Luminor accepts no liability for the use of the Marketing Communication content by its recipients.

If this Marketing Communication contains recommendations, those recommendations shall not be considered as an objective or independent explanation of the matters discussed herein. This document does not constitute personal investment advice or take into account the individual financial circumstances or objectives of the persons who receive it. The securities or other financial instruments discussed herein may not be suitable for all investors. The investor bears all risk of loss in connection with an investment. Luminor recommends that investors independently evaluate each issuer, security or instrument discussed herein and consult any independent advisors if they believe it necessary.

The information contained in this document also does not constitute advice on the tax consequences of making any particular investment decision. The estimates of costs and charges related to specific investment products are not provided therein. Each investor shall make his/her own appraisal of the tax and other financial advantages and disadvantages of his/her investment.

Risk information

The risk of investing in certain financial instruments including those mentioned in this document, is generally high, as their market value is exposed to many different factors. The value of and income from any investment may fluctuate from day to day as a result of changes in relevant economic markets (including changes in market liquidity). The information herein is not intended to predict actual results, which may differ substantially from those reflected. Past performance is not necessarily indicative of future results. When investing in individual financial instruments the investor may lose all or part of their investments.

Important disclosures of risks regarding investment products and investment services are available here.

Conflicts of interest

To avoid occurrence of potential conflicts of interest as well as to manage personal account dealing and / or insider trading, the employees of Luminor are subject to internal rules on sound ethical conduct, management of inside information, handling of unpublished research material and personal account dealing. The internal rules have been prepared in accordance with applicable legislation and relevant industry standards. Luminor’s Remuneration Policy establishes no link between revenues from capital markets activity and remuneration of individual employees.

The availability of this Marketing Communication is not associated with the amount of executed transactions or volume thereof.

This material has been prepared following the Luminor Conflict of Interest Policy, which may be viewed here.

Distribution

This Marketing Communication may not be transmitted to, or distributed within, the United States of America or Canada or their respective territories or possessions, nor may it be distributed to any U.S. person or any person resident in Canada. The document may not be duplicated, reproduced and(or) distributed without Luminor’s prior written consent.