Rally in April – return to normality or major investor trap? | Luminor

Rally in April – return to normality or major investor trap?

Atis Krūmiņš

Head of Investment Management

- Boosted by unprecedented central bank liquidity and hopes of COVID-19 peak being already reached, equities experienced strong price rebound in April;

- Macroeconomic data continues to indicate that world might experience worst economic decline since 1930s Great Depression;

- Extra caution is warranted as risks of another significant market drop surpassing March lows remain elevated.

After extraordinary market decline, triggered by coronavirus economic shutdowns, prices of global equities and majority of other risky assets bottomed in late March and continued drifting upwards throughout April, rising from bottom by almost 30%. There were two major reasons supporting strong rally – improvement in coronavirus dynamics and monetary stimuli announced and implemented.

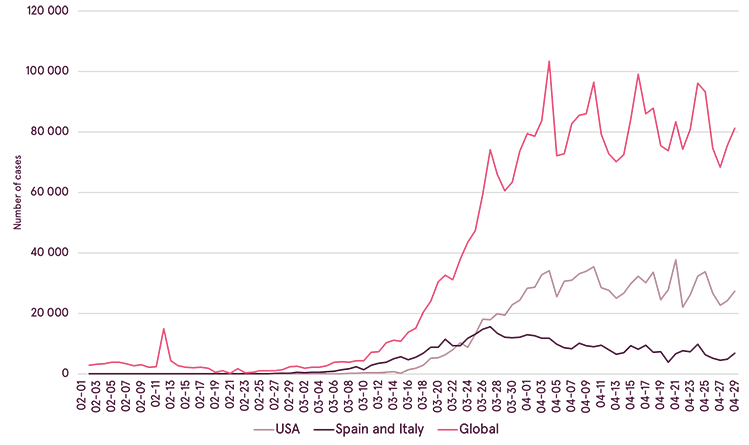

Indeed, number of new daily global and US COVID-19 cases stopped accelerating further and reached plateau at the start of the month. Moreover, in most severely hit Western European countries such as Italy and Spain spread of disease was in clear downtrend compared to March. As a result, it allowed to lift some of the quarantine measures by the end of April, and in some countries such as Germany even reopen parts of the economy. In USA, states were also allowed to decide, if to reopen their economy starting from 1st of May.

Daily increase in global, US, Spain and Italy coronavirus cases

Source: Bloomberg

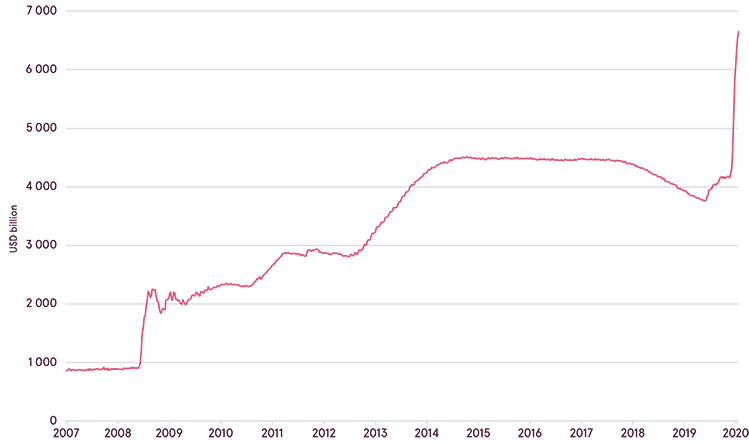

Furthermore, global central banks continued to introduce additional measures in order to ease potential economic damages, with FED this time being particularly active. Specifically, US Central bank announced that it will start buying not just government securities, but also corporate bonds and bond ETFs, with possibility to buy funds that hold riskiest high yield debt instruments. In addition, it rolled out $ 2.3 trillion programs to support small and mid-sized businesses as well as local governments. Together with previously announced measures, FED liquidity injections into financial markets are truly massive in last two months, being already much higher than what was introduced during 2008-2009 financial recession, and being equivalent in size to all quantitative easing programs undertaken since then.

FED balance sheet

Source: Bloomberg

Such developments boosted investor confidence and led many analysts to believe that bear market is already over, while equity prices being headed to new all-time highs and potentially much higher levels. However, in our view, unfortunately, this may turn out to be wishful thinking. Economic risks still remain extremely high, and possibility of another leg down to even lower levels than reached in late March still very possible. Let us discuss these risks in more detail.

First of all, it is true that significant progress was made in terms of COVID-19 dynamics. However, it is quite natural that if majority of population is restricted from contacting each other and predominantly stays at home, no new infectious cases would be registered. However, now, when economies starting to be reopened and inhabitants are allowed to move more freely, could there be any guarantee that acceleration of new virus cases would not return again? “Spanish flu” pandemic of 1918 developed in four waves, and actually it was not the first, but second wave which turned out to be most infectious and deadliest. Nobody knows, will there be and if it does, how severe can be the second wave in COVID-19, but we think it should be quite explanatory what is likely to happen to global economy, if another round of economic shutdowns and quarantine measures will have to be reintroduced. In this scenario, if markets realize that another wave of pandemic is coming, decline in equities may turn out to be even more rapid than what was observed in March.

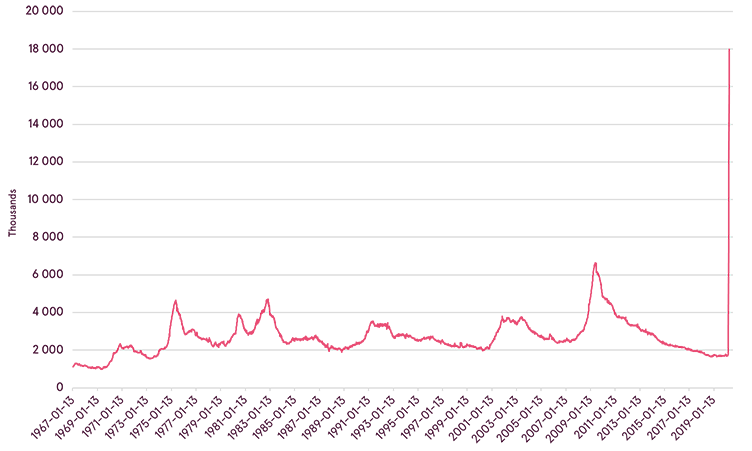

Secondly, even, if from virus perspective, the worst is over, according to IMF, global economy is still likely to be headed for worst economic downturn since the Great Depression. Different macroeconomic indicators in various countries are hitting record low numbers. For example, since end of February US continuous unemployment claims went from less than 2 million to around 20 million, indicating that unemployment rate is already above 15% in USA right now. Thus, just in around one month number of jobs being lost equaled to number of all new jobs being created since the end of last recession in mid-2009.

USA Continuous unemployment claims

Source: Bloomberg

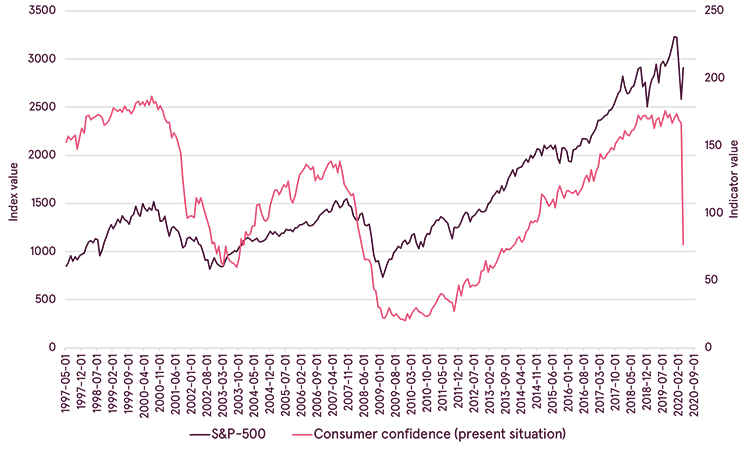

Just as in any recession, it is quite logical to assume that even despite all introduced stimulus measures, least effective and most leveraged companies would still be going out of business, while it would take considerable time to reemploy all people who lost their job. As a result, it may lead to prolonged negative impact on consumption and investment levels, which would lower aggregate economic demand, unless it is fully replaced by government spending. In addition, it is unclear, if recent events modified established spending patterns – after pandemic population and corporations may increase their propensity to save, leading to another negative impact to GDP. All these actions are likely to lower corporate earnings further in the upcoming quarters and put additional pressure on prices of financial assets. Another risk that we cannot ignore right now.

US consumer confidence vs S&P-500

Source: Bloomberg

US personal saving as % of disposable income

Source: Bloomberg

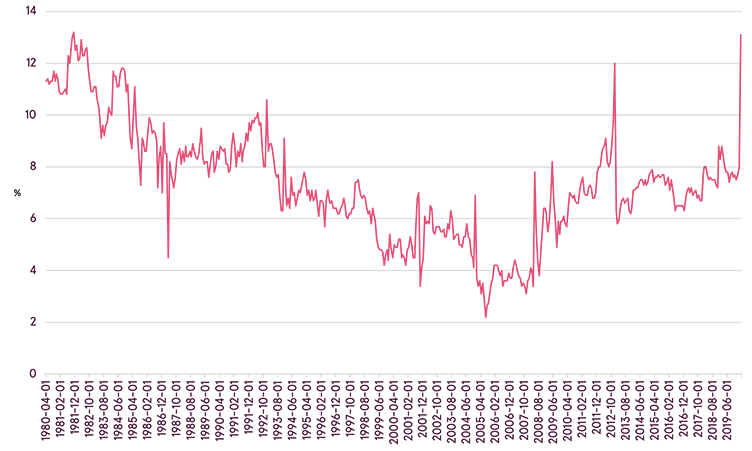

Third, even if all optimistic scenarios will play out, and corporate earnings are not reduced more than is already expected, equities are not being cheap right now. According to forward price to earnings multiples; valuation of global equities as measured by MSCI ACWI is highest since at least 2003. Given extraordinary uncertainty about the future that we are witnessing at the moment, and the fact that majority of corporations are refusing to give any forward looking guidance, because even to management executives it is highly unclear what would be their upcoming financial results, such valuations may be way too optimistic.

Forward P/E multiple of MSCI ACWI (global equity index)

Source: Bloomberg

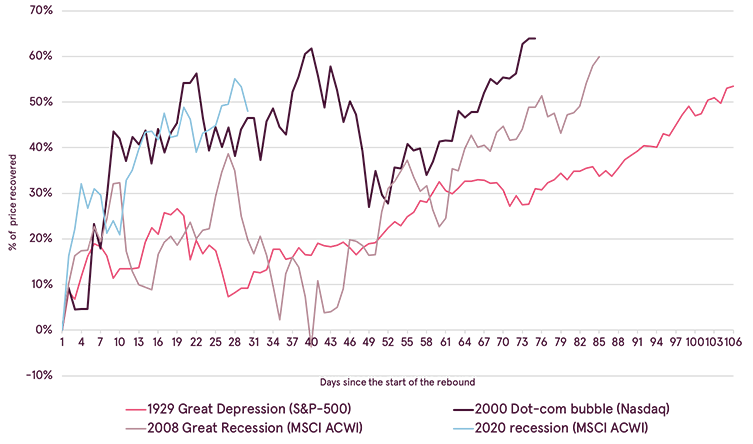

Also, we may say that despite April rally being extremely strong, it is not abnormal given magnitude of initial decline from late February. Often during recessions, after first initial shock lower, investors still believe that large declines in asset prices may be prevented, as economy will be fast enough to recover. As a result, prices experience strong rebound, until more bleak reality resurfaces. It happened in 2008, when housing crisis was already common knowledge and multiple banks including Bear Sterns were already bailed out. It happened in 2000, when dot-com bubble has already burst and multiple internet companies were facing financial trouble. It also happened after1929 Wall Street Crash to which we compared 2020 decline in terms of magnitude in our previous overview. After initial crash lower at that time, US indices rebounded by around 50% higher before continuing significant decline. Please note that we are not saying something similar should happen this time, but we cannot ignore the risk of further market decline.

Percentage of price recovered in rebound after initial move down during recessions

Source: Bloomberg

Summing up, despite some positive encouraging news and good rebound in financial markets, significant risks described above remain. However, there is also some balancing effect from all the monetary and fiscal stimulus implemented and announced. For example, although earnings yield (earnings divided by price) is fairly low right now, compared to close to 0% bond yields, equities do still offer some risk premium. Nevertheless, uncertainty remains high as there are still many unknowns. Therefore, it makes sense to stay cautious and stick to your long-term plan avoiding impulsive investment decisions based on market price actions.

Warnings

- This Marketing Communication is not considered investment research and has not been prepared in accordance with standards applicable to independent investment research.

- This Marketing Communication does not limit or prohibit the bank or any of its employees from dealing prior to its dissemination.

Origin of the Marketing Communication

This Marketing Communication originates from the Portfolio Management unit (hereinafter referred to as PMU) – a division of Luminor Bank AS (reg. No 11315936, with registered address at Liivalaia 45, 10145, Tallinn, Republic of Estonia, represented within the Republic of Latvia by Luminor Bank AS Latvian branch, reg. No 40203154352, address: Skanstes iela 12, LV-1013, Riga, hereinafter - Luminor). PMU is involved in the provision of discretionary portfolio management services to Luminor clients.

Supervisory authority

As a credit institution Luminor is subject to supervision by the Latvian Financial Supervisory Authority (Finanšu un kapitāla tirgus komisija). Additionally, Luminor is subject to supervision by the European Central Bank (ECB), which undertakes such supervision within the Single Supervisory Mechanism (SSM), which consists of the ECB and the national responsible authorities (Council Regulation (EU) No 1024/2013 - SSM Regulation). Unless set out herein explicitly otherwise, references to legal norms refer to norms enacted by the Republic of Latvia.

Content and source of the publication

This Marketing Communication has been prepared by PMU for information purposes. Luminor will not consider recipients of this Communication as its clients and accepts no liability for use by them of the contents, which may not be suitable for their personal use.

Opinions of PMU may deviate from recommendations or opinions presented by the Luminor Markets unit. The reason may typically be the result of differing investment horizons, using specific methodologies, taking into consideration personal circumstances, applying a specific risk assessment, portfolio considerations or other factors. Opinions, price targets and calculations are based on one or more methods of valuation, for instance cash flow analysis, use of multiples, behavioural technical analyses of underlying market movements in combination with considerations of the market situation, interest rate forecasts, currency forecasts and investment horizon.

Luminor uses public sources that it believes to be reliable. However, Luminor has not performed independent verification. Luminor makes no guarantee, representation or warranty as to their accuracy or completeness. All investments entail a risk and may result in both profits and losses.

This Marketing Communication constitutes neither a solicitation of an offer nor a prospectus in the sense of applicable laws. An investment decision in respect of a financial instrument, a financial product or an investment (all hereinafter “product”) must be made on the basis of an approved, published prospectus or the complete documentation for such a product in question, and not on the basis of this document. Neither this document nor any of its components shall form the basis for any kind of contract or commitment whatsoever. This document is not a substitute for the necessary advice on the purchase or sale of a financial instrument, a financial product.

No Advice

This Marketing Communication has been prepared by Luminor PMU as general information and shall not be construed as the sole basis for an investment decision. It is not intended as a personal recommendation of particular financial instruments or strategies. Luminor accepts no liability for the use of the Marketing Communication content by its recipients.

If this Marketing Communication contains recommendations, those recommendations shall not be considered as an objective or independent explanation of the matters discussed herein. This document does not constitute personal investment advice or take into account the individual financial circumstances or objectives of the persons who receive it. The securities or other financial instruments discussed herein may not be suitable for all investors. The investor bears all risk of loss in connection with an investment. Luminor recommends that investors independently evaluate each issuer, security or instrument discussed herein and consult any independent advisors if they believe it necessary.

The information contained in this document also does not constitute advice on the tax consequences of making any particular investment decision. The estimates of costs and charges related to specific investment products are not provided therein. Each investor shall make his/her own appraisal of the tax and other financial advantages and disadvantages of his/her investment.

Risk information

The risk of investing in certain financial instruments including those mentioned in this document, is generally high, as their market value is exposed to many different factors. The value of and income from any investment may fluctuate from day to day as a result of changes in relevant economic markets (including changes in market liquidity). The information herein is not intended to predict actual results, which may differ substantially from those reflected. Past performance is not necessarily indicative of future results. When investing in individual financial instruments the investor may lose all or part of their investments.

Important disclosures of risks regarding investment products and investment services are available here.

Conflicts of interest

To avoid occurrence of potential conflicts of interest as well as to manage personal account dealing and / or insider trading, the employees of Luminor are subject to internal rules on sound ethical conduct, management of inside information, handling of unpublished research material and personal account dealing. The internal rules have been prepared in accordance with applicable legislation and relevant industry standards. Luminor’s Remuneration Policy establishes no link between revenues from capital markets activity and remuneration of individual employees.

The availability of this Marketing Communication is not associated with the amount of executed transactions or volume thereof.

This material has been prepared following the Luminor Conflict of Interest Policy, which may be viewed here.

Distribution

This Marketing Communication may not be transmitted to, or distributed within, the United States of America or Canada or their respective territories or possessions, nor may it be distributed to any U.S. person or any person resident in Canada. The document may not be duplicated, reproduced and(or) distributed without Luminor’s prior written consent.