Second COVID‑19 wave and US political uncertainty raise questions about the future | Luminor

Second COVID‑19 wave and US political uncertainty raise questions about the future

- With probable Biden win and senate control remaining among republicans, election uncertainty has abated, but probability of new stimulus bill is still unclear;

- Second COVID‑19 wave and new lockdowns in Europe reintroduce economic uncertainty in the region, however, there is still hope that situation in other regions could remain better;

- Central bank actions and no additional economic shocks might still lead to decent post‑election rally until Christmas;

- Despite high volatility, investors still should carefully follow their long‑term investment strategy.

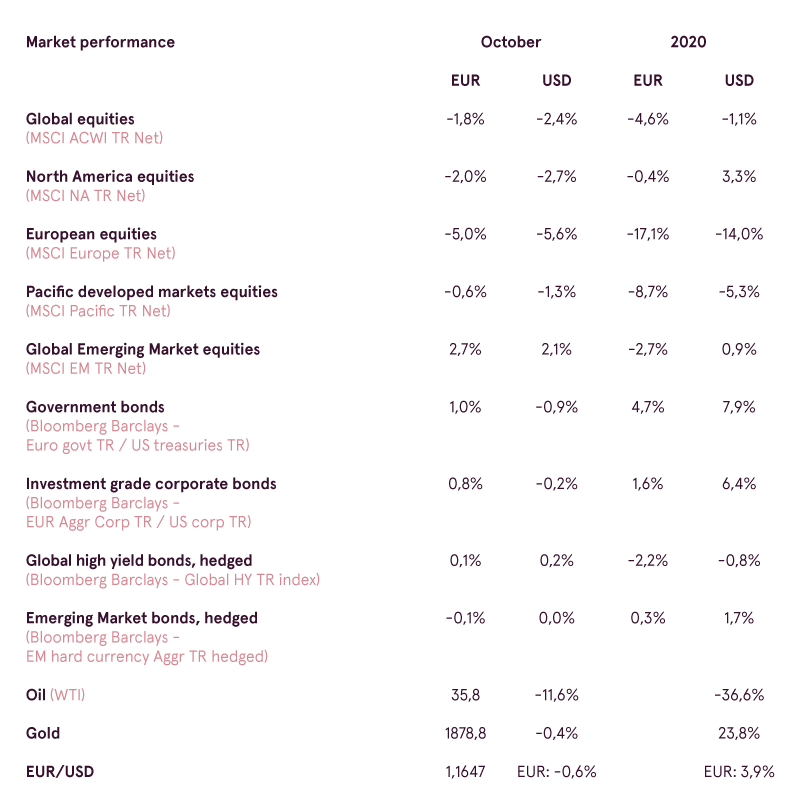

October was rather controversial month for financial markets. It started on a positive note with investors being excited about new massive fiscal stimulus bill to be potentially introduced in the USA, but ended in the negative territory due to coronavirus developments in Europe combined with US political uncertainty. As these two factors continue to drive investment performance in November and both are more important than anything else, we would discuss both of them in more detail.

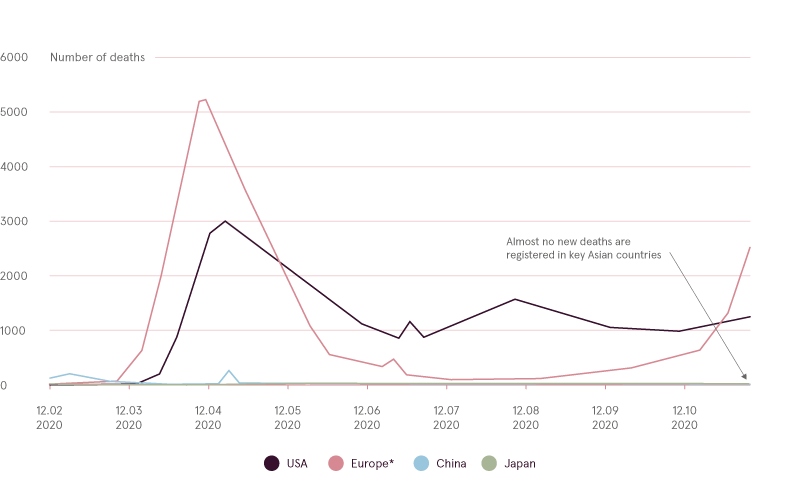

COVID‑19 situation in Europe started to get out of control already in mid‑September registering new record in number of new daily cases compared to developments in spring1. However, for the time being, European governments tried not to introduce harsh measures to fight spread of virus, as situation with hospitalizations and number of deaths was still much lower than at the beginning of the year. But with weather becoming colder and spread of disease intensifying by late October, disturbing trends both in number of seriously ill patients and deaths has also reemerged. As a result, one by one, countries like France, Germany, UK and others had no choice, but to announce new strict lockdown measures, what in essence means – new major economic hit and trouble for local financial markets, if no countermeasures are introduced.

New daily deaths of COVID-19 (weekly average)

*European data includes Germany, France, UK, Spain, Italy, Netherlands and Belgium

Source: Bloomberg

New daily deaths of COVID-19 (weekly average)

Source: Bloomberg

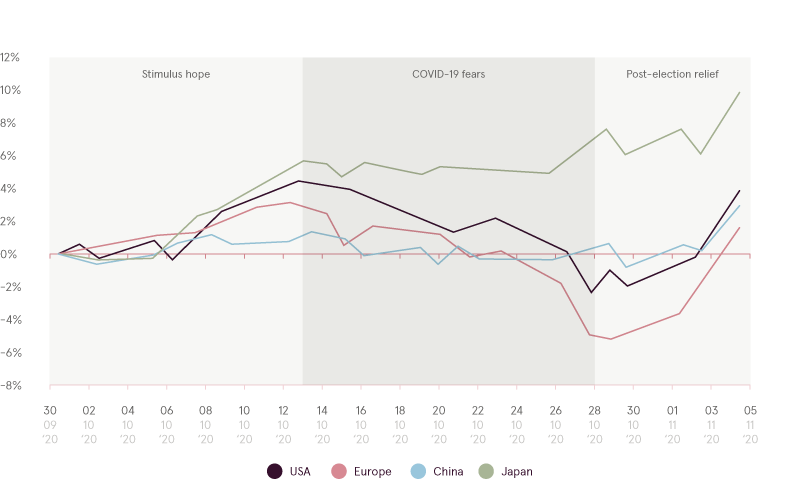

Thankfully, for financial markets in global context, COVID‑19 risks are materializing only in Europe right now, while situation in USA still remains much better, and there is almost non‑existent risk of second wave in majority of Asian countries at the moment as well. This is also the reason, why local Asian indices in countries like China or Japan have barely declined and even increased in EUR terms throughout the month.

Performance of selected regions in EUR since 2020 09 30

Source: Bloomberg

In November, coronavirus impact on financial markets would largely depend on whether European leaders would try to introduce new fiscal aid in the region to help mitigate damage to businesses and job market created by new lockdown. In addition, ECB already hinted on new monetary measures in December, but question is, will buying of financial assets be enough to prevent enterprises from potential bankruptcies, unless those companies would receive actual funds to survive.

Another potentially even bigger problem is what will happen in USA, which is much more important region than Europe, in terms of its impact on the markets. Cases continue to spike there, but number of deaths is still much lower than in spring and summer. Many experts fear that as flu season would intensify in Northern America, hospitalization trends would also become similar to what is experienced in Europe, just with a lag. And if it is indeed the case, new lockdown in USA without solid fiscal stimulus in place might become a very troubling development indeed.

With that in mind, let us shift focus to US politics and what election results will probably mean for the future. Probable victory of democrat Joe Biden2 and republicans maintaining control of the senate indicates potential stalemate for consensus on future policies. Whatever decision Biden and democrats would try to introduce, be it massive fiscal stimulus bill, new infrastructure spending, change in tax policies or other matters, republican senate would be able to block any of such initiatives. As a result of such potential confrontations, needed policies - mainly fiscal spending to provide additional income for millions of unemployed and to grant funds to negatively affected companies will probably not be introduced in a timely manner. That is why if COVID‑19 dynamics would worsen in USA, but no stimulus bill is there yet, economic damage might be even more severe than expected.

Another issue that might complicate matters even more is possibility of Trump initially not accepting the elections result. As current race for presidency was extremely tight, and key battleground states were won by Biden with a narrow margin, Trump may appeal to US Supreme Court in order to initiate recount procedure in these important states. In 2000 presidential elections similar situation has happened, when Al Gore was identified as a winner at first, but through recount, it became clear that Florida3 votes were counted incorrectly and actual winner should be George Bush Jr. That is why until inauguration process in January, there is still risk that Trump will not be ready to announce himself as a losing side, and it would be extremely hard to pass any bills or initiatives while this uncertainty is still present. From this perspective any stimulus bill may come not earlier than only February.

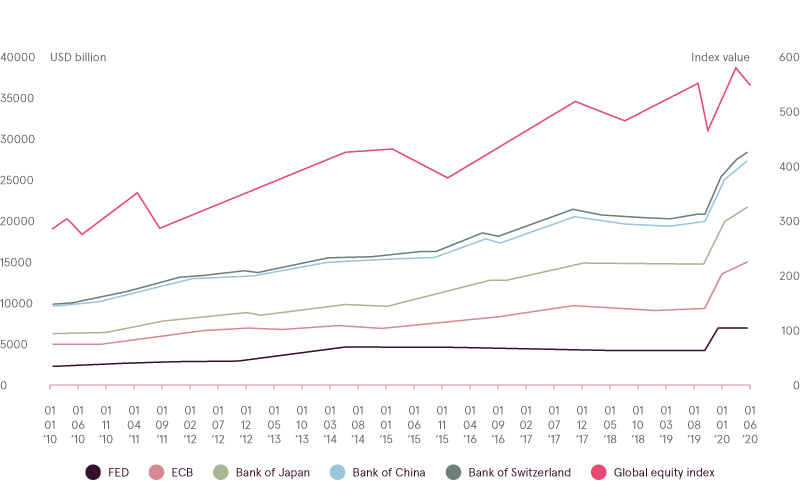

However, despite these risks market initial post‑election reaction turned out to be very positive. Similar to what happened in summer main winners turned out to be FANMAG and other popular large‑cap stocks. Hard to say, whether investor mania, which we mentioned in some of our previous reports, is ready to continue for another several months irrespective of any news or risks out there. But what can definitely contribute to another wave of investor euphoria are new monetary actions that may be introduced by Central Banks in order to stabilize financial system in times of COVID‑19 and political uncertainty.

Major central bank total assets (USD'bln) and performance of global equities

Source: Bloomberg

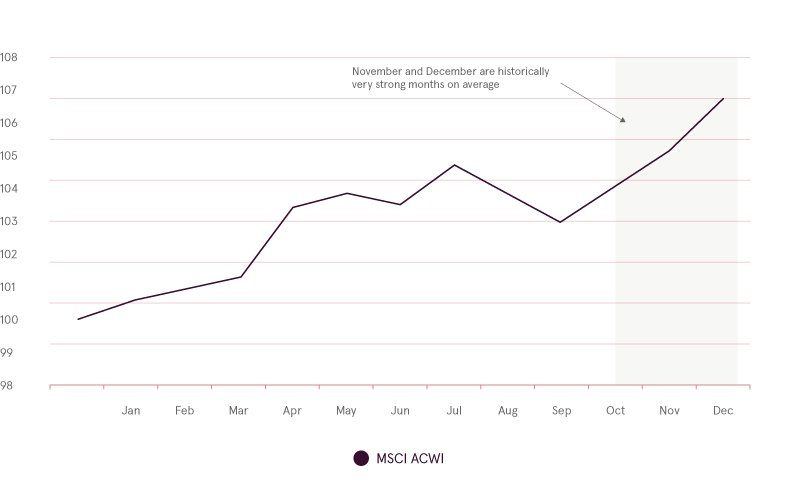

In addition, post‑election November and December are historically very strong months, as investors become relieved with political results and start planning their Christmas purchases. Current year is, of course, not a typical year at all, but if no new economic shocks would happen, pre‑holiday optimism might return this year as well, calming markets and contributing to positive performance for the rest of the year. Hopefully, we would get more clarity in terms of further market movements in the nearest future.

Monthly average performance of global equities (since 1995)

Source: Ned Davis Research

Given absolute uncertainty in relation to how severe COVID‑19 situation would be across the world and how efficiently governments would be able to respond and provide timely economic support, volatility in the markets most likely would remain high. Higher volatility may not only lead to strong and fast moves to the downside, but also to strong and fast moves to the upside. Therefore, it is prudent to remain conservative, patiently executing investment decisions according to the predetermined plan, and keeping the long‑term view in focus.

1Most likely actual number of cases was still higher in spring, but capacity to register all ill persons was limited at that time

2At the moment of writing results were still not officially announced, but Trump victory became highly improbable

3Key battleground state which determined final elections result

Warnings

- This Marketing Communication is not considered investment research and has not been prepared in accordance with standards applicable to independent investment research.

- This Marketing Communication does not limit or prohibit the bank or any of its employees from dealing prior to its dissemination.

Origin of the Marketing Communication

This Marketing Communication originates from the Portfolio Management unit (hereinafter referred to as PMU) – a division of Luminor Bank AS (reg. No 11315936, with registered address at Liivalaia 45, 10145, Tallinn, Republic of Estonia, represented within the Republic of Latvia by Luminor Bank AS Latvian branch, reg. No 40203154352, address: Skanstes iela 12, LV-1013, Riga, hereinafter - Luminor). PMU is involved in the provision of discretionary portfolio management services to Luminor clients.

Supervisory authority

As a credit institution Luminor is subject to supervision by the Latvian Financial Supervisory Authority (Finanšu un kapitāla tirgus komisija). Additionally, Luminor is subject to supervision by the European Central Bank (ECB), which undertakes such supervision within the Single Supervisory Mechanism (SSM), which consists of the ECB and the national responsible authorities (Council Regulation (EU) No 1024/2013 - SSM Regulation). Unless set out herein explicitly otherwise, references to legal norms refer to norms enacted by the Republic of Latvia.

Content and source of the publication

This Marketing Communication has been prepared by PMU for information purposes. Luminor will not consider recipients of this Communication as its clients and accepts no liability for use by them of the contents, which may not be suitable for their personal use.

Opinions of PMU may deviate from recommendations or opinions presented by the Luminor Markets unit. The reason may typically be the result of differing investment horizons, using specific methodologies, taking into consideration personal circumstances, applying a specific risk assessment, portfolio considerations or other factors. Opinions, price targets and calculations are based on one or more methods of valuation, for instance cash flow analysis, use of multiples, behavioural technical analyses of underlying market movements in combination with considerations of the market situation, interest rate forecasts, currency forecasts and investment horizon.

Luminor uses public sources that it believes to be reliable. However, Luminor has not performed independent verification. Luminor makes no guarantee, representation or warranty as to their accuracy or completeness. All investments entail a risk and may result in both profits and losses.

This Marketing Communication constitutes neither a solicitation of an offer nor a prospectus in the sense of applicable laws. An investment decision in respect of a financial instrument, a financial product or an investment (all hereinafter “product”) must be made on the basis of an approved, published prospectus or the complete documentation for such a product in question, and not on the basis of this document. Neither this document nor any of its components shall form the basis for any kind of contract or commitment whatsoever. This document is not a substitute for the necessary advice on the purchase or sale of a financial instrument, a financial product.

No Advice

This Marketing Communication has been prepared by Luminor PMU as general information and shall not be construed as the sole basis for an investment decision. It is not intended as a personal recommendation of particular financial instruments or strategies. Luminor accepts no liability for the use of the Marketing Communication content by its recipients.

If this Marketing Communication contains recommendations, those recommendations shall not be considered as an objective or independent explanation of the matters discussed herein. This document does not constitute personal investment advice or take into account the individual financial circumstances or objectives of the persons who receive it. The securities or other financial instruments discussed herein may not be suitable for all investors. The investor bears all risk of loss in connection with an investment. Luminor recommends that investors independently evaluate each issuer, security or instrument discussed herein and consult any independent advisors if they believe it necessary.

The information contained in this document also does not constitute advice on the tax consequences of making any particular investment decision. The estimates of costs and charges related to specific investment products are not provided therein. Each investor shall make his/her own appraisal of the tax and other financial advantages and disadvantages of his/her investment.

Risk information

The risk of investing in certain financial instruments including those mentioned in this document, is generally high, as their market value is exposed to many different factors. The value of and income from any investment may fluctuate from day to day as a result of changes in relevant economic markets (including changes in market liquidity). The information herein is not intended to predict actual results, which may differ substantially from those reflected. Past performance is not necessarily indicative of future results. When investing in individual financial instruments the investor may lose all or part of their investments.

Important disclosures of risks regarding investment products and investment services are available here.

Conflicts of interest

To avoid occurrence of potential conflicts of interest as well as to manage personal account dealing and / or insider trading, the employees of Luminor are subject to internal rules on sound ethical conduct, management of inside information, handling of unpublished research material and personal account dealing. The internal rules have been prepared in accordance with applicable legislation and relevant industry standards. Luminor’s Remuneration Policy establishes no link between revenues from capital markets activity and remuneration of individual employees.

The availability of this Marketing Communication is not associated with the amount of executed transactions or volume thereof.

This material has been prepared following the Luminor Conflict of Interest Policy, which may be viewed here.

Distribution

This Marketing Communication may not be transmitted to, or distributed within, the United States of America or Canada or their respective territories or possessions, nor may it be distributed to any U.S. person or any person resident in Canada. The document may not be duplicated, reproduced and(or) distributed without Luminor’s prior written consent.