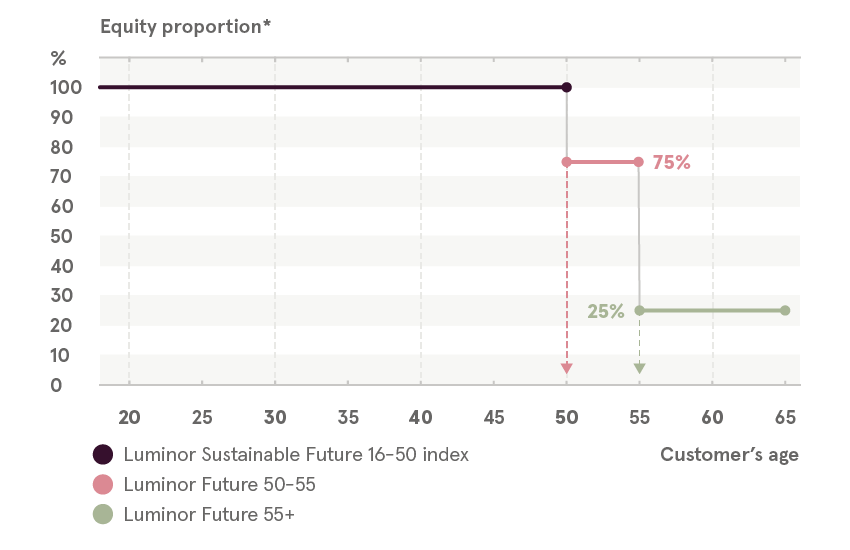

Luminor 3rd pension pillar plans:

- Luminor Sustainable Future 16-50 index

- Luminor Future 50-55

- Luminor Future 55+

Pension plan names reflects the recommended age group for which each pension plan is most suitable. The names of the pension plans have been adjusted assuming that supplementary pension capital will be accumulated until the age of 65.

We use life-cycle approach in Luminor 3rd pillar pension plans, to make it simple and understandable for customers choose the most suitable option and take full advantage of financial market opportunities to grow their personal retirement savings.

You always have the option to adjust your pension plan based on your preferences, your planned retirement age, and your willingness to take on investment-related risks.